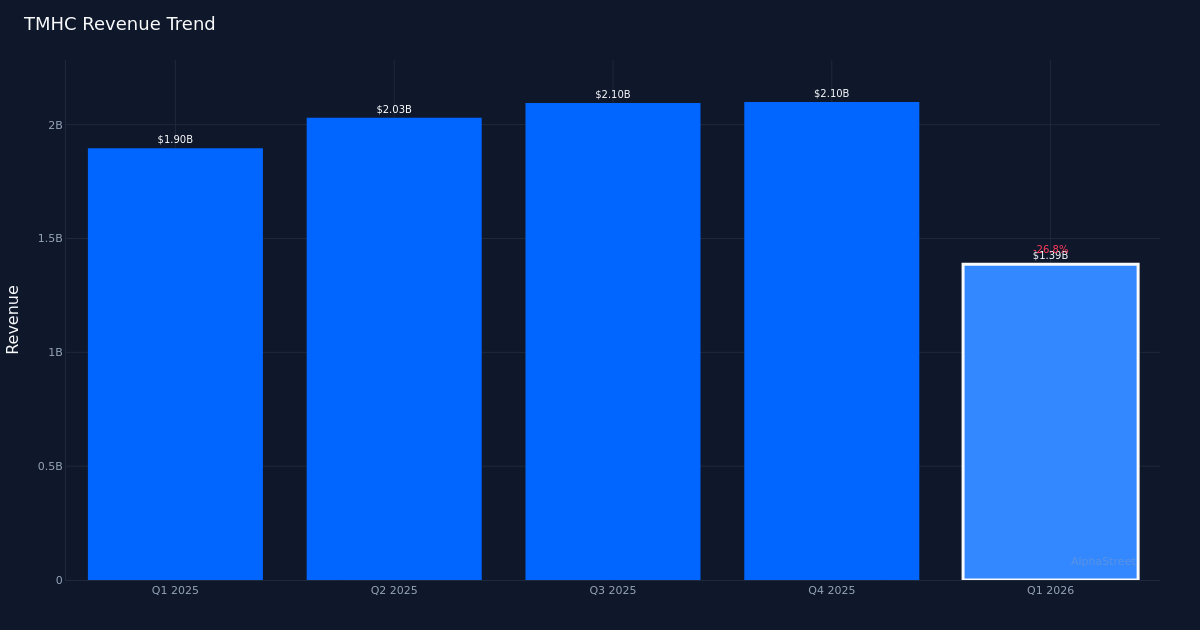

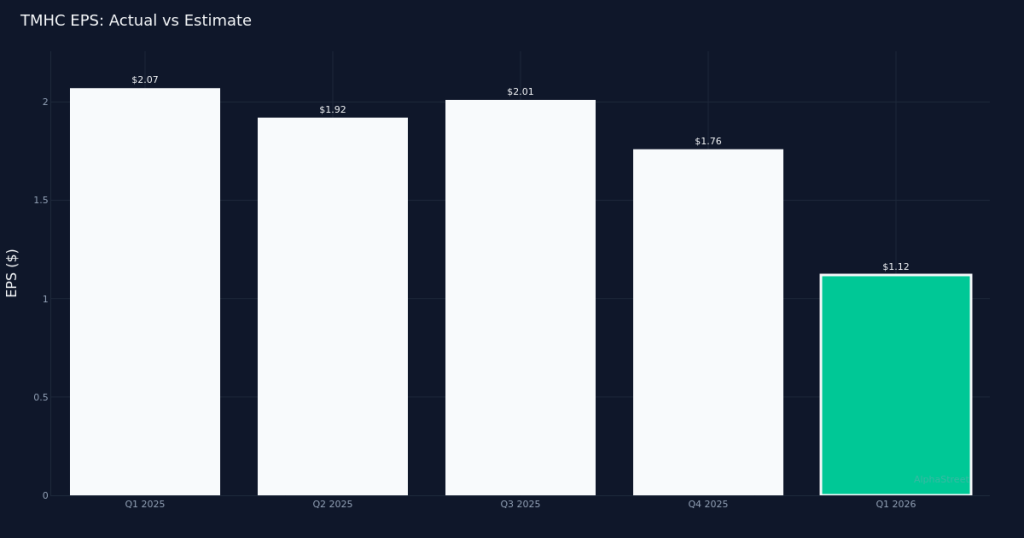

TMHC|EAdj. EPS $1.12 vs $0.87 est (+28.7%)|Rev $1.39B|Net Income $98.6M

TMHC|EAdj. EPS $1.12 vs $0.87 est (+28.7%)|Rev $1.39B|Net Income $98.6MSolid earnings beat. Taylor Morrison Home Corporation (NYSE: TMHC) delivered Q1 2026 adjusted earnings of $1.12 per share, surpassing analysts’ $0.87 forecast by 28.7%, demonstrating strong profitability despite a challenging top-line environment. Revenue totaled $1.39B for the quarter, down 26.8% from $1.90B in Q1 2025, reflecting continued headwinds in the residential construction sector as elevated mortgage rates and affordability constraints weighed on homebuyer demand.

Margin quality shines. The impressive earnings outperformance against a backdrop of declining revenues suggests the company has effectively managed costs and maintained pricing discipline in a softer market. Net income reached $98.6M for the quarter, pointing to operational efficiency gains that more than offset volume pressures. This type of beat—driven by margin management rather than pure revenue acceleration—demonstrates management’s ability to navigate difficult market conditions, though sustainability of these margins warrants close monitoring as the company balances profitability with market share considerations.

Volume metrics stabilizing. Taylor Morrison closed 2,268 homes during the quarter, while net sales orders totaled 2,914 units. The order activity provides insight into demand momentum and suggests the company continues to generate interest despite broader housing market volatility. The progression of orders relative to closings will be critical for investors assessing whether the company can maintain production levels and margin strength through the remainder of 2026.

Wall Street remains constructive. Analyst sentiment reflects moderate optimism, with consensus standing at 11 buy ratings, 2 hold ratings, and 1 sell rating. This distribution suggests most analysts believe Taylor Morrison’s operational execution and financial positioning can weather current industry headwinds, though the presence of some caution signals that the path forward may not be without challenges as the company manages through this transitional period for residential construction.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.