Taylor Morrison Home Corporation (NYSE: TMHC) announced Q4 2025 results this week. The company reported a net income of $174 million. Also, adjusted net income totaled $188 million. Notably, Taylor Morrison’s Q4 2025 earnings delivered results across its diverse portfolio of brands and communities nationwide.

Taylor Morrison Q4 2025 Earnings: Financial Results

Q4 2025 home closings revenue reached $1.96 billion. This fell 10% from $2.17 billion in Q4 2024. Yet gross margin held at 21.8%. This shows good pricing and cost control. Also, adjusted home closings gross margin stayed at 21.8%.

Net sales orders totaled 2,499 homes. This is down 5% from last year. Still, 3,285 closings came at $596,000 each. In fact, the SG&A ratio of 9.9% shows good execution.

Full Year 2025 Taylor Morrison Q4 2025 Earnings: Annual Results

For the full year 2025, home closings revenue hit $7.76 billion. Also, net income was $783 million. The company did 12,997 closings at $597,000 each. Plus, adjusted net income was $830 million.

The full-year gross margin was 22.5% versus 24.4% last year. So margin faced pressure in 2025. Yet adjusted gross margin was 23.0%. The SG&A ratio improved to 9.5% from 9.9%.

Read the full Taylor Morrison Q4 2025 earnings press release for complete details.

Quarterly Revenue Trends: Taylor Morrison Q4 2025 Earnings Analysis

The chart shows Taylor Morrison Q4 2025 earnings revenue trends. Q1 2025 revenue was $1.83 billion. Then Q2 rose to $1.97 billion. Then Q3 reached $2.00 billion. Finally, Q4 fell to $1.96 billion.

Housing Market Focus: Taylor Morrison Q4 2025 Earnings Overview

Taylor Morrison runs in 12 states. The company serves many buyer groups. So it handles first-time buyers and move-up buyers. In fact, Esplanade resort communities have great potential.

The monthly pace held at 2.4 net orders per site in Q4. This stayed the same. Also, Q4 ended with 341 active communities. So community count rose 1% from last year. Plus, 54% of lots were off balance sheet.

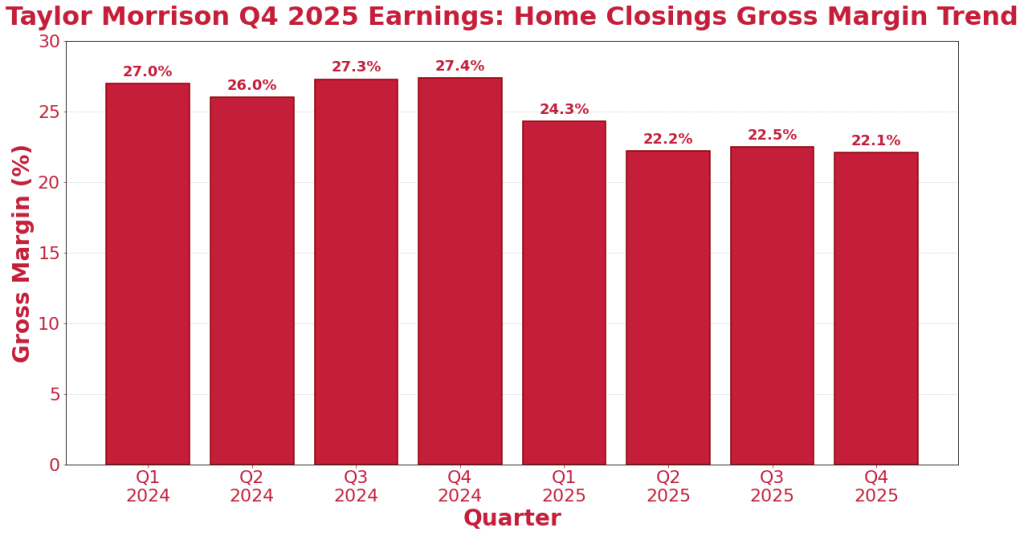

Gross Margin Performance: Taylor Morrison Q4 2025 Earnings Outlook

Taylor Morrison’s Q4 2025 earnings show margin trends. The Q1 2024 margin was 27.0%. Q4 2024 held at 27.4%. Yet 2025 fell. Q1 2025 was 24.3%. Q2 fell to 22.2%. Q3 and Q4 held at 22.5% and 22.1%.

Key Business Drivers: Taylor Morrison Q4 2025 Earnings Highlights

Land strategy stays disciplined. So Taylor Morrison spent $2.2 billion on land in 2025. Also, 6.1 years of supply exist. Plus, 54% of lots are off balance sheet. Financial services add value. So the 89% mortgage rate in Q4 2025 shows strength. Also, FICO scores hit 750. Yet online tools boost sales rates.

2026 Taylor Morrison Q4 2025 Earnings Guidance & Outlook

Management gave 2026 guidance. So full-year closings are about 11,000 units. Also, the average price is $580,000-$590,000. Plus, the SG&A ratio is in the mid-10%. For Q1 2026, closings are about 2,200 units. So community count targets about 360. Also, average price is about $580,000. Yet gross margin is about 20%.

Key Takeaways: Taylor Morrison Q4 2025 Earnings Summary

Taylor Morrison’s Q4 2025 earnings had mixed results. So revenue fell 10% year-over-year. Yet margins held. Also, cash reserves remained solid. Plus, 2026 looks positive. The diverse portfolio helps. So Esplanade growth is coming. Also, financial services help buyers. Yet margin pressure reflects the market. So watch 2026 results.

Click Here to visit the AlphaStreet website.