The popular car models of Tesla Inc. (NASDAQ: TSLA) have become more affordable after a series of price cuts this year. When the electric-vehicle maker reports earnings next week, the market’s focus will be on its margin performance and cash flows. Meanwhile, the stable performance of the stock reflects investors’ continued confidence in the company.

Tesla’s market value more than doubled in the first half of the year, as the company maintains its dominance in the US electric vehicle market with more than 60% market share. The stock hit a record high about one-and-half years ago and crossed the $400 mark, but pulled back soon and has declined by a third since then. Though the company’s unimpressive first-quarter performance weighed on investor sentiment a few months ago — amid macro uncertainties and lingering supply chain issues –TSLA quickly bounced back from the temporary dip.

Growth Target

The management is optimistic about achieving compound annual growth above the long-term rate of 50% this year, delivering around 1.8 million cars. Tesla’s strong technology backup makes it easier for the company to bring innovations like full self-driving and incorporate artificial intelligence into its products to meet long-term goals while increasing profitability.

The general outlook on the electric vehicle market is quite bullish, and Tesla has the production capacity to meet the growing demand. Recently, the company’s Texas plant came online and was ramped up, while the phase-2 expansion of the Shanghai plant is complete.

Q2 Estimates

The second-quarter report is expected on July 19, at 4:05 pm ET. Taking a cue from the company’s aggressive expansion initiatives, experts are projecting a whopping 45% year-over-year growth in sales, which would drive up June quarter revenue to $24.57 billion. Net income per share, adjusted for one-off items, is estimated to have increased to $0.82 from $0.76 last year, aided by the high demand. The cautious forecast shows that earnings growth was restricted by recent price cuts, to some extent.

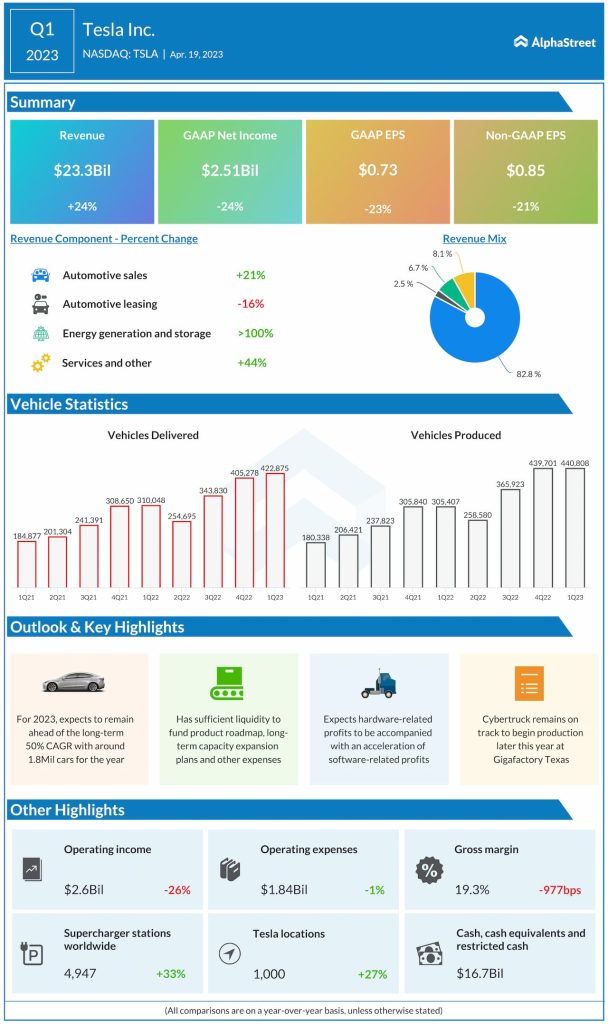

From Tesla’s Q1 2023 earnings call:

“We plan to continue to invest heavily into our future plans, which include the Cybertruck Next Generation platform, in-house cell production, energy storage business, and our autonomy and AI-enabled products. And we plan to do this while keeping the business financially healthy and industry-leading. To accomplish this we need to remain focused on cost efficiency and working capital and in particular unwinding the strategic inventory buildup leftover from the pandemic.”

Results Miss

In the first quarter, adjusted earnings missed estimates for the first time in two years as pricing pressures weighed on margins. At $0.85 per share, first-quarter profit was also 21% lower than the prior-year number. Meanwhile, revenues increased 24% to $23.3 billion but fell short of expectations, marking the third miss in a row. Automotive Sales and Services & Other expanded in double digits while energy segment revenues more than doubled, which was partially offset by a contraction in Automotive Leasing. Both production and deliveries climbed to new highs.

TSLA has been trading well about its 52-week average in recent weeks, mostly outperforming the tech and auto industries. The stock traded higher during Wednesday’s session.