Shares of Constellation Brands Inc. (NYSE: STZ) were up 2% on Friday, a day after the company delivered mixed results for the third quarter of 2023. The brewer also cut its earnings outlook for the full year. Here’s a look at the good and the bad from the Q3 earnings report:

Mixed results

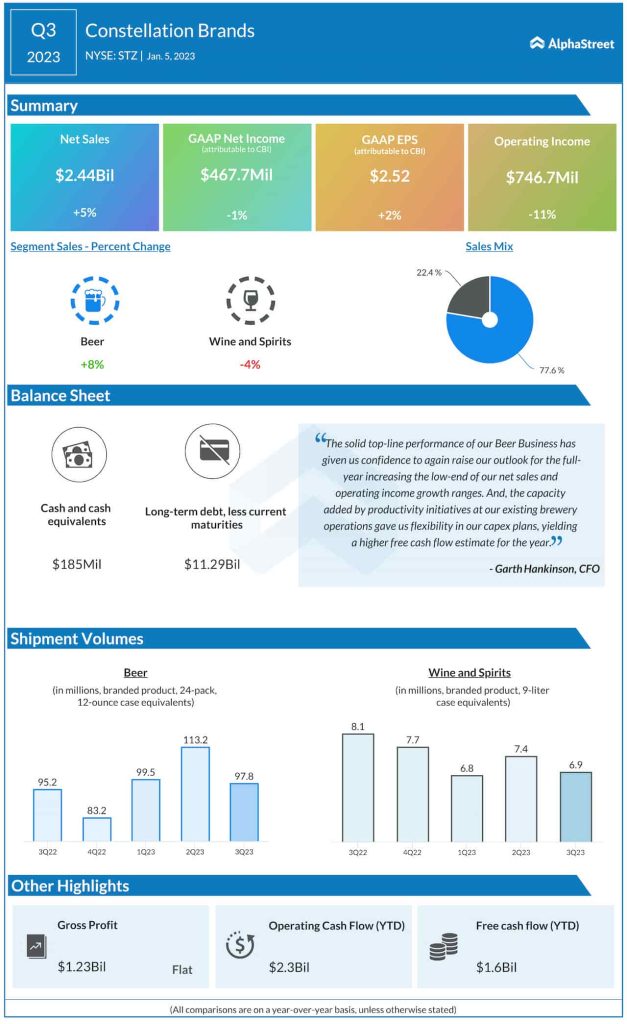

For the third quarter of 2023, Constellation posted net sales of $2.44 billion, which was up 5% compared to the same period a year ago and ahead of the consensus target of $2.40 billion. Adjusted EPS was $2.83, down 9% from the year-ago quarter and below the estimate of $2.90. On a reported basis, EPS grew 2% to $2.52. Comparable EPS, excluding Canopy, was $3.01, down 12% year-over-year.

Strength in beer

In Q3, net sales in Constellation’s beer business grew 8% YoY to $1.89 billion, driven by strong demand and higher average price increases. Shipment volumes rose 3% in the quarter. Depletions growth was around 6%, driven by strong performances by the Modelo Especial, Modelo Chelada and Pacifico brands.

Although depletions decelerated in Q3 from Q2 due to incremental fall pricing and lower distribution growth, the company expects the impact of incremental pricing to settle over the coming months even as distribution growth appears to be normalizing.

Modelo Especial delivered depletion growth of 4.4% in Q3. The brand continues to strengthen its position in its primary markets with significant opportunity for additional expansion. Depletions for Pacifico and Modelo Chelada grew over 40% in the third quarter. A large part of Modelo Chelada’s gains were driven by the launch of new products and the company anticipates significant growth from this brand going forward.

Constellation raised its sales guidance for the beer business and now expects 9-10% growth for FY2023 compared to the previous range of 8-10%. Operating income is now expected to grow 4-5% versus the prior range of 3-5%.

Decline in wine and spirits

Net sales in the wine and spirits segment declined 4% to $544.6 million in Q3 due to decreases in shipments and depletions. Shipments were down nearly 15% while depletions fell approx. 6% during the quarter. On an organic basis, sales were down 1% and shipments fell nearly 13%.

Constellation continues to expect organic net sales for its wine and spirits business to decline 0-2% in FY2023. Operating income is expected to grow 3-5%.

Guidance cut

Constellation cut its earnings outlook for fiscal year 2023 which the Street did not take well. The company lowered its range for comparable EPS, excluding Canopy, to $11.00-11.20 from the previous range of $11.20-11.60. In addition, reported EPS is now expected to range between $0.15-0.35 versus the prior range of $0.75-1.15.