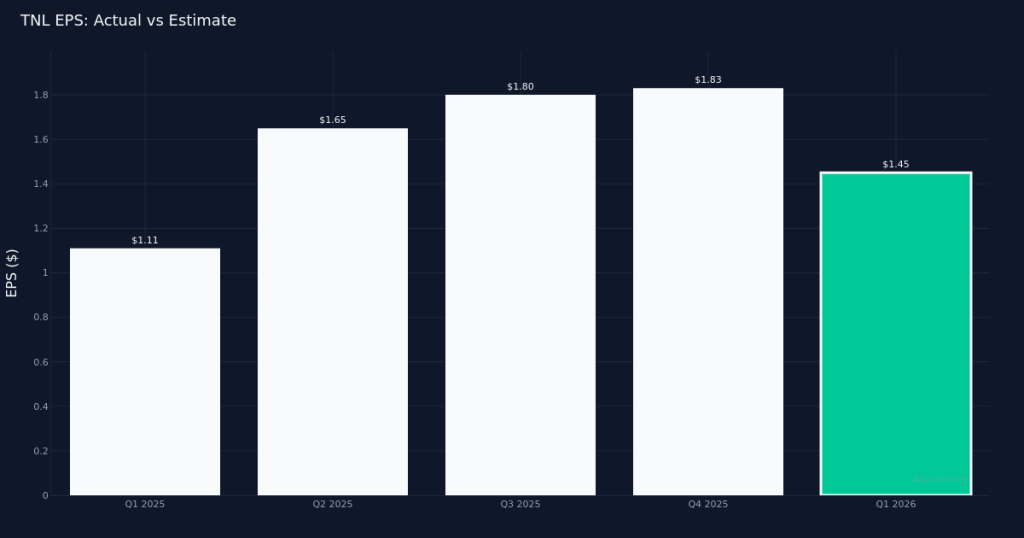

TNL|EPS $1.45 vs $1.32 est (+9.8%)|Rev $961M|Net Income $79.0M

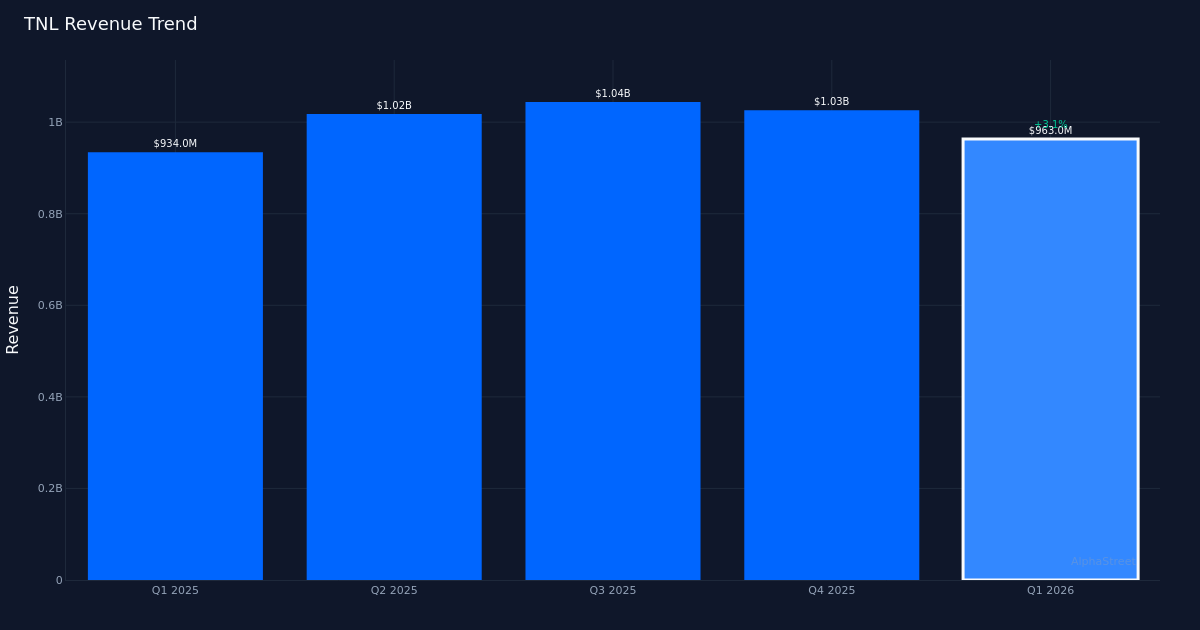

TNL|EPS $1.45 vs $1.32 est (+9.8%)|Rev $961M|Net Income $79.0MSolid Beat. Travel + Leisure Co. (NYSE:TNL) delivered Q1 2026 adjusted diluted earnings per share of $1.45, surpassing analysts’ $1.32 forecast by 9.8%, marking a strong start to the year for the vacation ownership and travel services provider. Revenue totaled $961M for the quarter, up 2.8% from $934M in Q1 2025, demonstrating the company’s ability to capitalize on sustained consumer demand for leisure travel experiences. Bottom-line profit came in at $93M on an adjusted basis as the company balanced growth investments with operational efficiency.

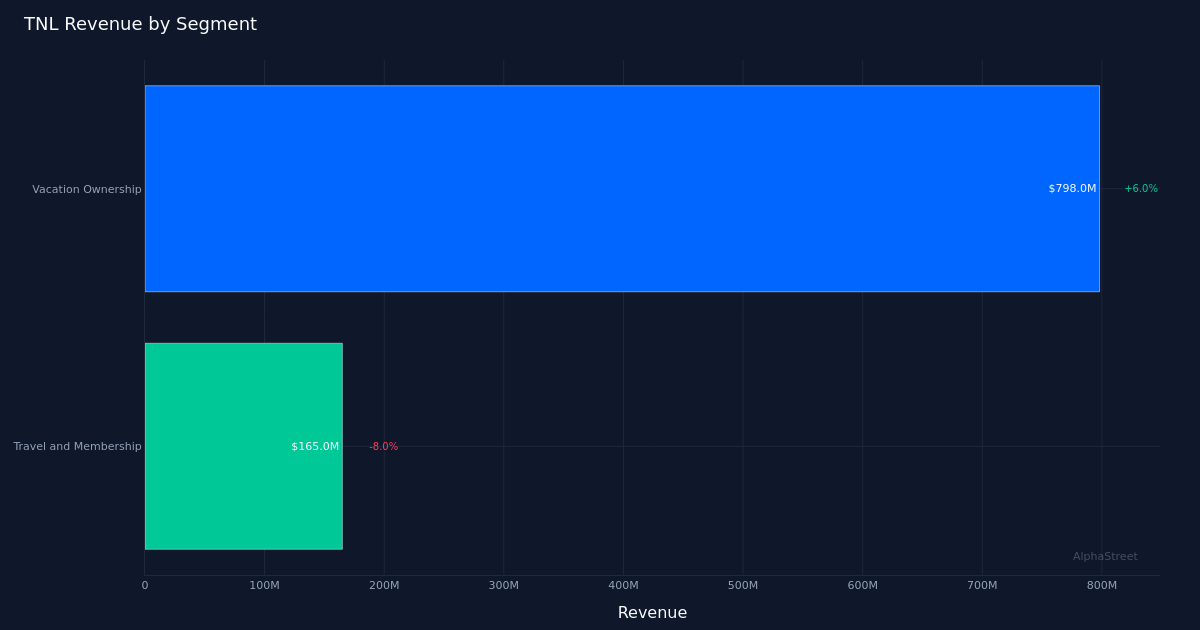

Revenue-Driven Performance. The earnings beat appears fundamentally sound, driven by topline growth rather than aggressive cost-cutting measures. The 2.8% revenue expansion reflects genuine business momentum across the company’s vacation ownership platform, with Vacation Ownership leading the way at $798.0M in revenue, up 6.0% year-over-year. This segment’s performance underscores the ongoing appeal of timeshare and vacation club products to consumers seeking predictable leisure options. Gross VOI sales reached $549.0M for the quarter, indicating healthy customer acquisition and upgrade activity within the existing owner base.

Operational Execution. The company operated 161,000 tours during the quarter, demonstrating its continued focus on converting prospective buyers through face-to-face sales presentations. This metric is particularly important for Travel + Leisure’s business model, as tours serve as the primary customer acquisition channel for vacation ownership products. The ability to maintain tour volume while driving revenue growth suggests improving conversion rates or higher transaction values, both positive indicators of pricing power and sales force productivity in the current operating environment.

Market Response. Despite the earnings beat, TNL shares fell 11.2% to $67.55 following the release, suggesting investors may be concerned about forward guidance, margin trajectory, or broader macroeconomic headwinds affecting discretionary consumer spending. The disconnect between operational results and stock performance could also reflect profit-taking after a recent run-up or sector rotation away from consumer discretionary names. Wall Street consensus stands at 8 buy, 3 hold, and 0 sell ratings, indicating analysts maintain generally positive outlooks on the company’s fundamentals despite the immediate price action.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.