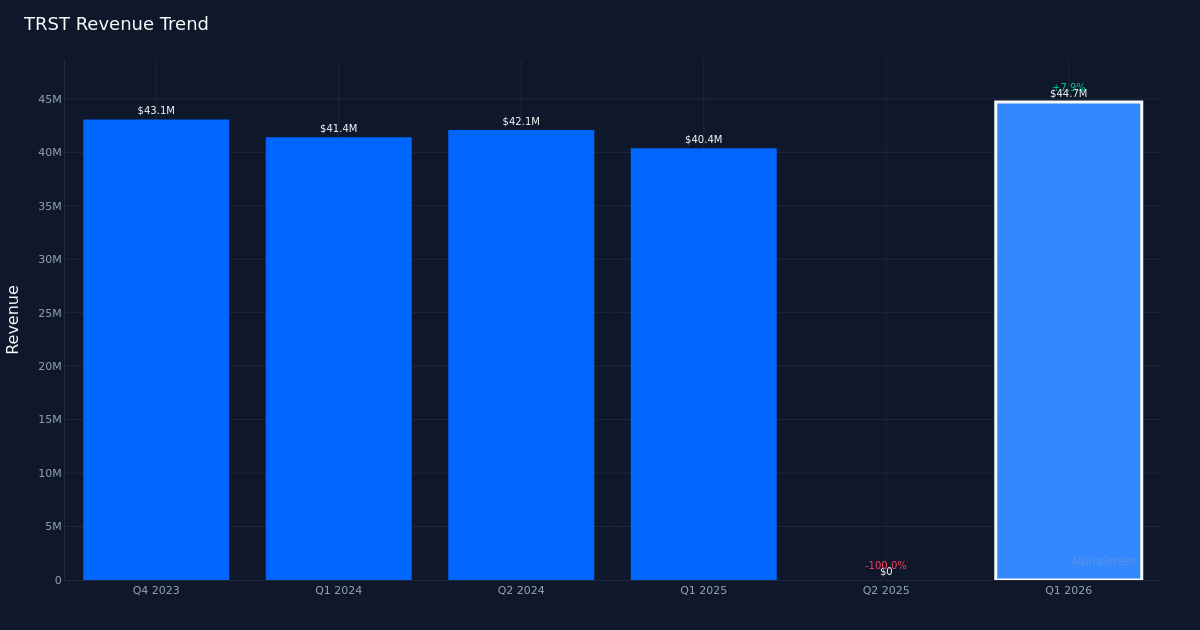

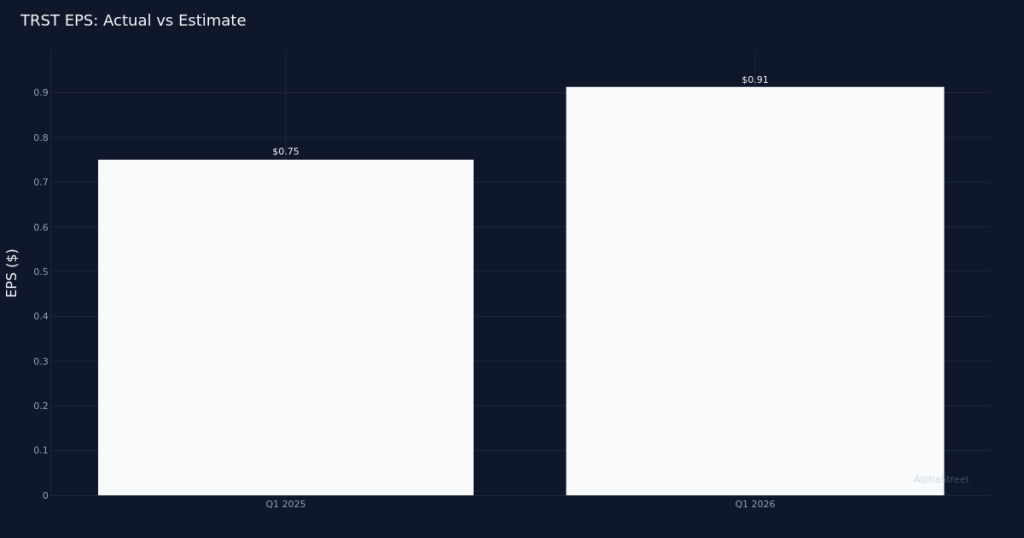

In-line performance. TrustCo Bank Corp NY (NASDAQ:TRST) reported Q1 2026 diluted earnings of $0.91 per share, delivering the top line of $44.7M that matched the $0 consensus. Net income reached $16.3M for the quarter, as the regional bank demonstrated continued momentum in its core operations. The stock traded largely unchanged following the report, suggesting investors had largely anticipated these results.

Year-over-year acceleration. The quarter reflected meaningful growth versus the prior year period, with EPS up 21.3% from $0.75 in Q1 2025. Revenue expanded at a slower but still healthy clip, representing a 10.7% increase from the $40.4M recorded in Q1 2025. The divergence between earnings growth and revenue growth indicates improved operating leverage within the business, a favorable trend for a regional banking franchise navigating the current rate environment.

Core banking strength. Net interest income was $45 for the quarter, reflecting the bank’s ability to manage its lending and deposit portfolios effectively. The company operated 133 full service banking offices at quarter end, maintaining its brick-and-mortar presence across its footprint. For a regional bank of this scale, physical branch presence remains an important customer acquisition and relationship management tool, particularly in markets where TrustCo has established community ties.

Muted market reception. Despite the solid year-over-year growth metrics, shares remained largely unchanged following the announcement. This tepid reaction likely reflects the inline nature of the print relative to expectations, offering no meaningful surprise to either side. With Wall Street consensus standing at 0 buy, 2 hold, and 2 sell recommendations, the analyst community appears cautious on the name, potentially viewing the growth trajectory as already reflected in current valuations or harboring concerns about the sustainability of margin expansion in future quarters.

Profitability trajectory. The 21.3% earnings growth substantially outpacing the 10.7% revenue increase points to margin expansion during the quarter. For regional banks, this dynamic typically stems from improved net interest margins, lower credit costs, or operating expense discipline. The quality of this earnings beat hinges on whether margin gains prove durable or represent a cyclical peak as competitive dynamics in deposit pricing continue to evolve.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.