Ulta Beauty, Inc. (NASDAQ: ULTA) has constantly increased its market value even while navigating through uncertainties like the coronavirus pandemic and more recently the economic downturn. The company outshined competitors with exceptionally strong financial performance in the holiday quarter as its affordable beauty products continue to attract shoppers.

The Bolingbrook-based beauty retailer’s stock crossed the $ 500 mark a few weeks ago and climbed to an all-time high last month. Interestingly, ULTA has defied the recent market volatilities and maintained an uptrend, outperforming the broad market quite often. Currently, it is an expensive stock — with most of the tailwinds already factored into the price, the valuation looks high. But those who have an eye on this growth stock should consider the long-term benefits of owning it, and use this opportunity.

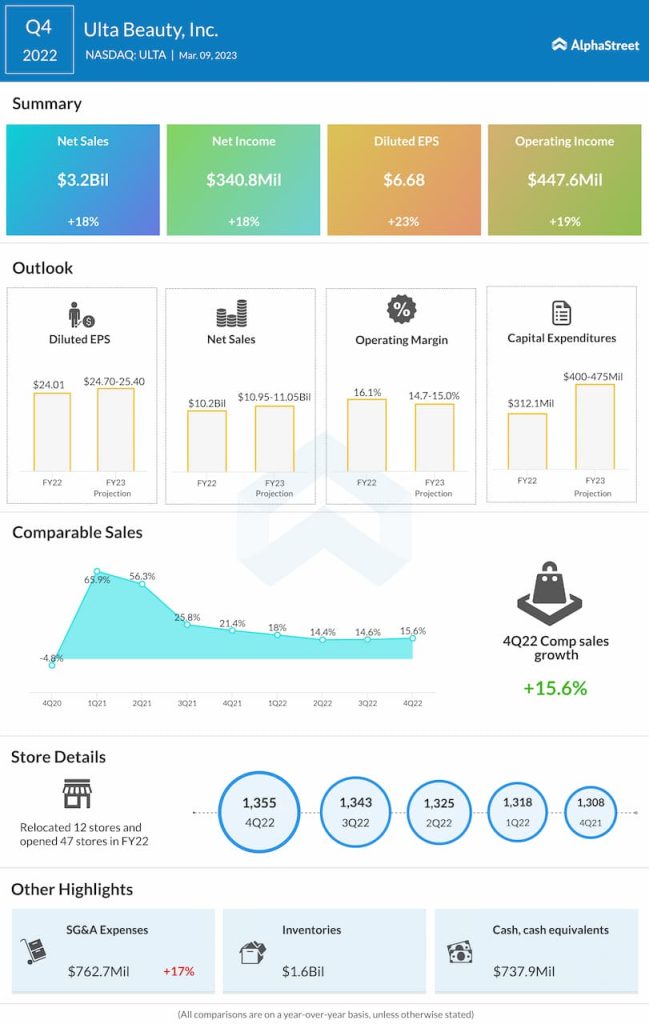

Outlook

While the outlook is bullish, it needs to be seen whether the company would maintain the momentum experienced in the holiday quarter when the demand for makeup and personal care products remained elevated. Meanwhile, if the strain on personal finances persists — due to interest rate hikes and inflation — it might force households to avoid discretionary spending, including beauty products and cosmetics.

Ulta Beauty Inc (ULTA) Q4 2022 Earnings Call Transcript

After decelerating from the COVID-driven boom, Ulta Beauty’s comparable sales growth has stabilized, reflecting the recovery in store traffic after the market reopening. Underscoring the encouraging demand scenario, the company expanded its store network every quarter over the past two years. It is preparing to add 100 more stores in the next two years.

Financials

In the fourth quarter that ended January 2023, comparable sales climbed 15.6%, which translated into an 18% growth in sales to $3.2 billion. Net profit advanced in double digits to $340.8 million or $6.68 per share. The headline numbers came in above Wall Street’s consensus forecast, continuing the long-term trend.

Ulta Beauty executives are optimistic about the current fiscal year – they see sales and profitability to be above the 2022 levels. Also, there is an increase in the Capex layout, which should enable the company to achieve its expansion goals.

Road Ahead

Going forward, a key priority would be the continued expansion of All Things Beauty, the company’s innovative model for enhancing customer experience, while adding new brands across all categories and price points. The growth initiatives also include further expansion of the ulta.com platform.

Commenting on the Q4 performance, Ulta Beauty’s CEO Dave Kimbell said, “As we move into fiscal 2023, we remain optimistic about the strength and resiliency of the beauty category and the opportunities for Ulta Beauty. Over the last two years, the U.S. Beauty category experienced unprecedented growth, reflecting various factors, such as product innovation, expanding regimens, new social media platforms, return to work and resume social activities, and the elevated connection between beauty and overall self-care.”

Procter & Gamble (PG) raises sales outlook despite significant headwinds

The stock opened Thursday’s session at $522.23 and traded lower throughout the session, extending the recent weakness. Meanwhile, it is up 10% since the beginning of 2023.