Shares of Ulta Beauty, Inc. (NASDAQ: ULTA) stayed red on Wednesday. The stock has dropped over 4% in the past three months. The company has been facing certain headwinds which took a toll on its most recent quarterly earnings results. Based on the trends seen during the first half, Ulta decided to take a more cautious view for the year and lowered its full-year guidance.

Q2 performance and challenges

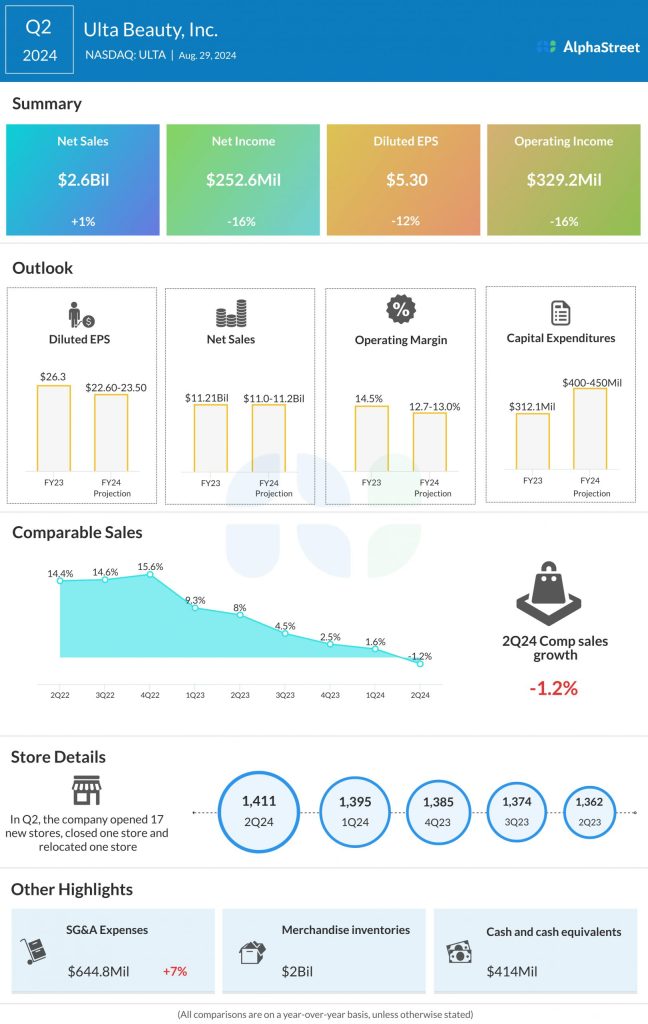

In the second quarter of 2024, Ulta Beauty’s net sales inched up 0.9% to $2.6 billion compared to the same period last year. The growth was driven by strong performance from new stores and a 12% increase in other revenue. Comparable sales decreased 1.2%, driven by a 1.8% decline in transactions, partly offset by a 0.6% growth in average ticket.

The beauty retailer believes its store transaction growth was impacted by a number of factors. Firstly, the beauty category is seeing growth normalize after three years of gains. In addition, consumers have become both budget-conscious and value-conscious. As mentioned on the company’s quarterly conference call, based on data from Circana, US beauty growth slowed to approx. 3% through the first half of 2024.

The second factor is heavy competition in the beauty category, which continues to pressure Ulta’s market share, especially in prestige beauty. On its call, the company stated that during the second quarter, it maintained its share in mass beauty but lost share in prestige beauty, particularly driven by hair and makeup categories.

Ulta also said that more than 80% of its stores have been impacted by one or more competitive openings in recent years, with more than half impacted by multiple competitive openings. These competitive headwinds continue to impact the top line of these stores.

Another factor that impacted the company’s results was the effect of incremental promotions, which did not drive sales growth as expected. Ulta rolled out incremental promotions to drive revenue growth after it started seeing weakness in late June and July. Although these offers drove sales and traffic across digital platforms, they did not deliver the expected benefit in stores.

Ulta’s gross margin fell by 100 basis points to 38.3% in Q2, driven mainly by lower merchandise margin and deleverage of store fixed costs. The decline in merchandise margin was caused by higher promotional activity, adverse impact from brand mix, and the lapping of benefits from price increases last year. The company delivered EPS of $5.30 for the quarter, which was down 12% from last year.

Full-year outlook

Ulta lowered its guidance for the full year of 2024 as it anticipates a dynamic operating environment and continued competitive pressure on its stores. The company cut its net sales outlook to $11.0-11.2 billion from $11.5-11.6 billion. It now expects comparable sales to be down 2% to flat instead of up 2-3%. EPS is now expected to be $22.60-23.50 versus the prior expectation of $25.20-26.00.