Shares of Ulta Beauty, Inc. (NASDAQ: ULTA) stayed red on Tuesday. The stock has gained 25% year-to-date. The specialty beauty retailer is set to report its earnings results for the third quarter of 2025 on Thursday, December 4, after markets close. Here’s a look at what to expect from the earnings report:

Revenue

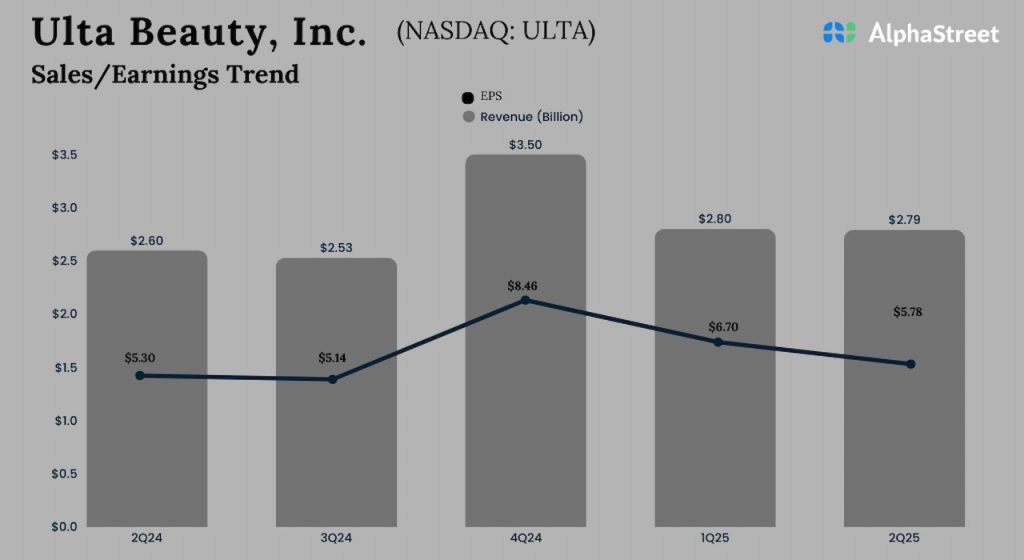

Analysts are projecting revenue of $2.70 billion for Ulta Beauty in the third quarter of 2025, which indicates a growth of over 6% from the same period a year ago. In the second quarter of 2025, net sales increased 9% year-over-year to $2.78 billion.

Earnings

The consensus estimate for earnings per share in Q3 2025 is $4.60, which implies a decline of nearly 11% from the prior-year quarter. In Q2 2025, EPS increased 9% YoY to $5.78.

Points to note

Ulta Beauty can be expected to benefit from resilience in the beauty category and healthy engagement with beauty and wellness even in an uncertain macroeconomic environment. The beauty category has seen stable growth in the US, with increases across both the mass beauty and prestige beauty segments, as budget-conscious consumers are still willing to spend on their beauty needs.

In Q2, Ulta saw comparable sales growth of 6.7%, driven by increases in transactions and average ticket. The company saw growth across both its store and digital channels, with a low double-digit increase in ecommerce sales, and also across all its major categories. It also continued to gain market share and saw a 4% increase in its loyalty members. This momentum may have continued in the third quarter.

The retailer is likely to have benefited from continued traction in fragrance, which saw robust double-digit growth last quarter. The skin care and wellness, makeup, hair care, and services categories are expected to have delivered healthy performances.

Ulta is expected to benefit from its marketing initiatives, partnerships, and new brand launches. Its efforts in building its digital capabilities and offering personalized experiences to customers are expected to yield benefits. It continues to expand into international markets which gives it further opportunity for growth.

Meanwhile, the company anticipates an increase in SG&A expenses for the second half of the year. In Q2, SG&A was up 15%. This rise in expenses may have put pressure on the bottom line in Q3.