Health insurer UnitedHealth Group (NYSE: UNH) stands out in the healthcare space for its unique business model covering a broad range of services within the industry. While the company dominated the health insurance market over the past several years, lately its stock has been under pressure due to uncertainties in the macroeconomic environment.

Over the years, investors have liked the Minnesota-headquartered firm for its successful business model and strong fundamentals. UNH has a history of consistently maintaining a slow but steady uptrend. However, the stock experienced weakness in the recent past, resulting in a lower valuation that looks attractive from an investment perspective. Last year, the stock mostly traded sideways and often underperformed the S&P 500, though it peaked towards the end of the year. The company hiked its dividend by 14% a year earlier and currently offers an above-average yield of 1.6%.

Q2 Report on Tap

As UnitedHealth gears up to unveil its second-quarter numbers, Wall Street analysts forecast earnings of $6.70 per share, on an adjusted basis. The estimate represents an improvement from the year-ago quarter when the company earned $6.14 per share. The consensus revenue estimate is $98.82 billion, compared to $92.9 billion in Q2 2023. The report is slated for release on Tuesday, July 16, at 5:55 am ET.

For the management, expanding the existing business and venturing into new areas is a key priority, by reinvesting in the business and through acquisitions. In 2023, the company acquired home health business LHC Group in a $5.4-billion deal. Meanwhile, UnitedHealth’s Optum division revealed plans to buy Amedisys, another home health provider, with the deal expected to close in the second half. Recent growth initiatives have positioned the company to tap into emerging opportunities in the industry.

Outlook

In the most recent quarter, the healthcare conglomerate’s bottom line was negatively impacted by the Change Healthcare cyberattack that made it pay ransom to protect patient data. However, such temporary headwinds can have only a limited impact on the business, considering the scale of operation. The company’s long-term prospects look intact since there is a steady uptick in the demand for healthcare services, mainly due to the rapidly aging population.

“Our strategy continues to focus on providing as much stability as possible in the reduced funding environment, improving outcomes and experiences for the consumers we’re privileged to serve, and delivering the performance you expect from us. We believe our long-term perspective and the deliberate multiyear approach we began last year is serving us well, putting us into a position of sustainable, competitive strength. Among a handful of notable business developments to share, UnitedHealthcare was honored to secure major Medicaid wins in Virginia, Texas, and Michigan,” UnitedHealth’s CEO Andrew Witty said in a statement a few months ago.

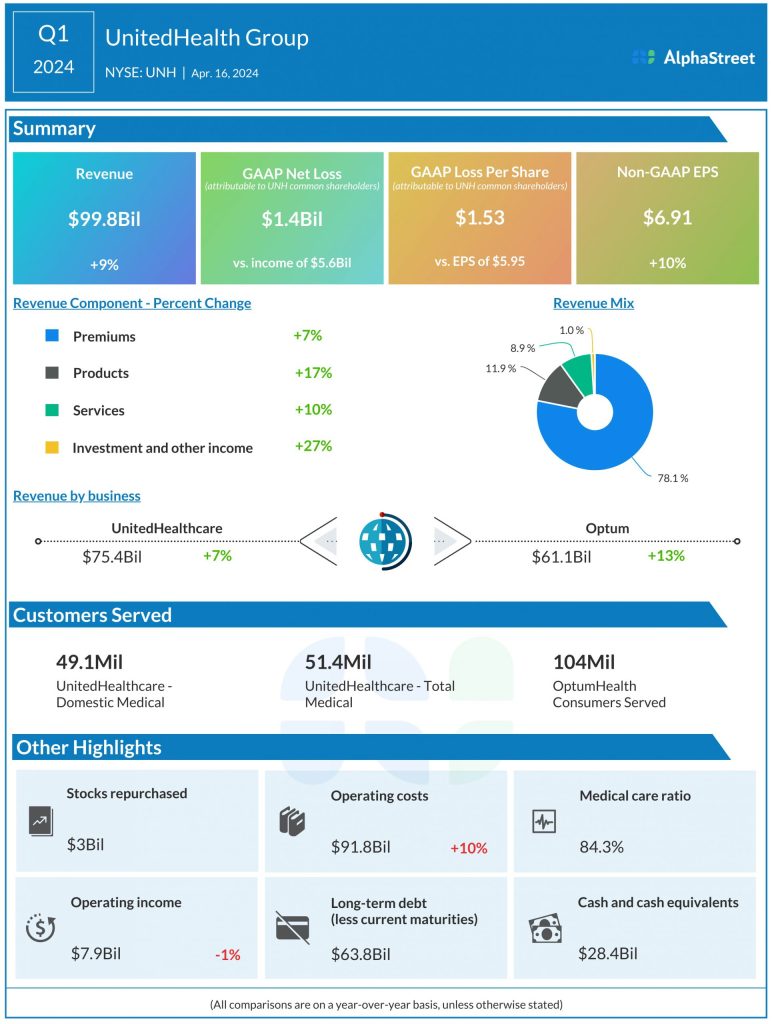

Solid Q1

The company entered fiscal 2024 on a positive note, delivering revenue growth across all four operating segments led by the core Premium business. Total revenues rose 9% year-over-year to about $100 billion, which is slightly above expectations. As a result, adjusted net income per share moved up 10% annually to $6.91. The bottom line exceeded estimates, a trend which has continued for more than a decade.

During Monday’s trading, the stock moved above $490 at one point, after closing the previous session lower. It has lost about 8% in the past six months.