For UnitedHealth Group Inc. (NYSE: UNH), the early effect of coronavirus on its business was a marked reduction in costs due to deferred care, which helped it record unusually high profits in the early months of the year. The second half is the time to repay for the company, given the spike in medical cost ratios as healthcare delivery services return to normal levels and more patients seek COVID-19 treatment.

When the health insurer reports its third-quarter results on October 14, analysts will be looking for a 21% drop in earnings to $3.07 per share. That is despite an estimated 6% increase in revenues compared to the year-ago period.

Investing in UNH

UnitedHealth’s shares, which maintained a steady uptrend in recent years, bounced back quickly after losing steam during the COVID-induced selloff. After withdrawing from an all-time high in mid-August, currently, the stock is once again hovering near the peak. It closed Tuesday’s regular session at $314.45, which is down 1.2%. The consensus rating on UNH is strong buy, with experts predicting a 10% growth in the 12-month period.

The present volatility is expected to ease once the pandemic-related headwinds subside and normalcy returns to the market. While the recent moderation in price offers a buying opportunity for those looking for long-term returns, a section of analysts believes the stock is overvalued.

Weak Outlook

The company is unlikely to repeat its impressive second-quarter performance, going forward. The deferral of care in the risk-based businesses, which contributed to the bottom-line growth, will be reversed in the coming quarters. Initial estimates show that access to medical services increased significantly in the current quarter, with more and more healthcare facilities resuming operations even as the authorities lift the curbs. Inpatient care and outpatient/physician services have already bounced back from the record lows.

From the Q2 2020 earnings conference call:

“We currently expect care access patterns while somewhat more volatile than in the past to moderately exceed normal baselines in the second half as people seek previously deferred care. And the pandemic, with high testing and treatment costs per affected consumer, is expected to continue to run its course throughout 2020 and into 2021.”

Growth Plan Intact

But the management has elaborate plans to keep the momentum going. Come next year, Medicare Advantage plans will be expanded to 290 more counties in 49 states, which is up from the current 46 states. Scheduled ahead of the annual open enrolment season, the initiative is expected to help the firm grow its membership base further.

Another area of focus is home care and digital assistance, a trend that is estimated to become more prevalent in the coming months due to the inconveniences caused by the pandemic. The company is busy ramping up its digital capabilities — from telemedicine and pharmacy e-commerce to AI-assisted health records and behavioral health services. Terming the transition to the new-generation health system “durable,” the management expects the trend to support its 13-16% long-term growth target.

Cautious Pricing

When it comes to pricing, UnitedHealth executives prefer to maintain the longstanding approach. It has taken into account the future impact of coronavirus, including the testing and treatment costs, and assumes a potential increase in severity due to deferred care. As part of boosting the e-commerce capabilities, the company last week acquired online medicine start-up divvyDOSE, which competes with Amazon’s (AMZN) PillPack.

Read management/analysts’ comments on quarterly reports

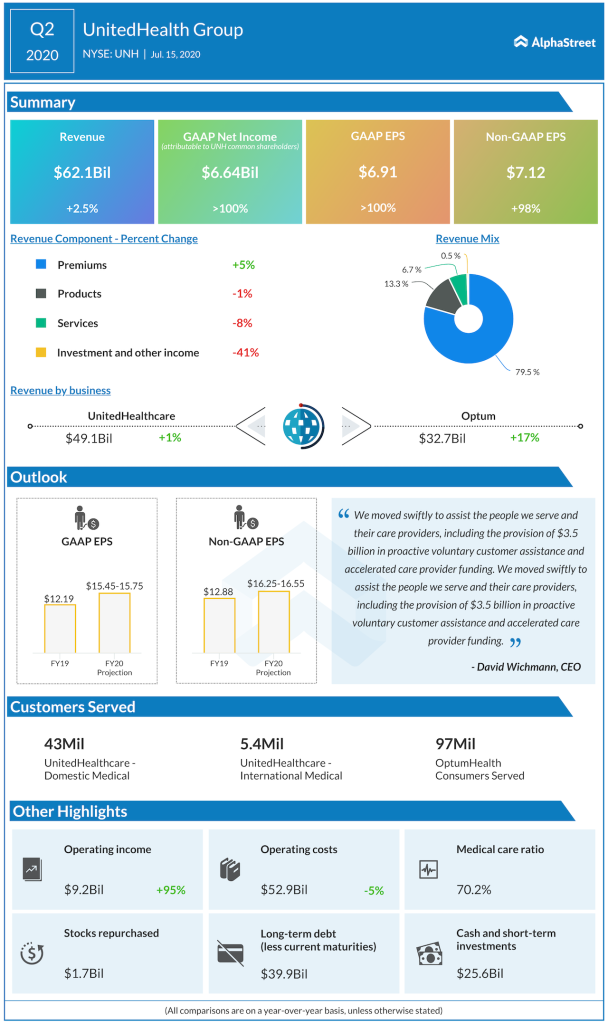

In the second quarter, a 5% growth in premiums, the main revenue driver, more than offset weakness in the other operating segments, resulting in a 2% increase in total revenues to $62 billion. Optum, the health services arm, witnessed double-digit growth. More than the top-line growth, earnings benefited from a marked decrease in operating costs and almost doubled to $7.12 per share.