AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects modest growth when Verizon Communications Inc. reports first-quarter results on April 27. The consensus among 19 analysts calls for earnings of $1.21 per share on revenue of $34.86B. Estimates span a fairly narrow range, with EPS projections between $1.12 and $1.33, while revenue estimates range from $34.03B to $35.56B, suggesting relatively uniform expectations for the nation’s largest wireless carrier.

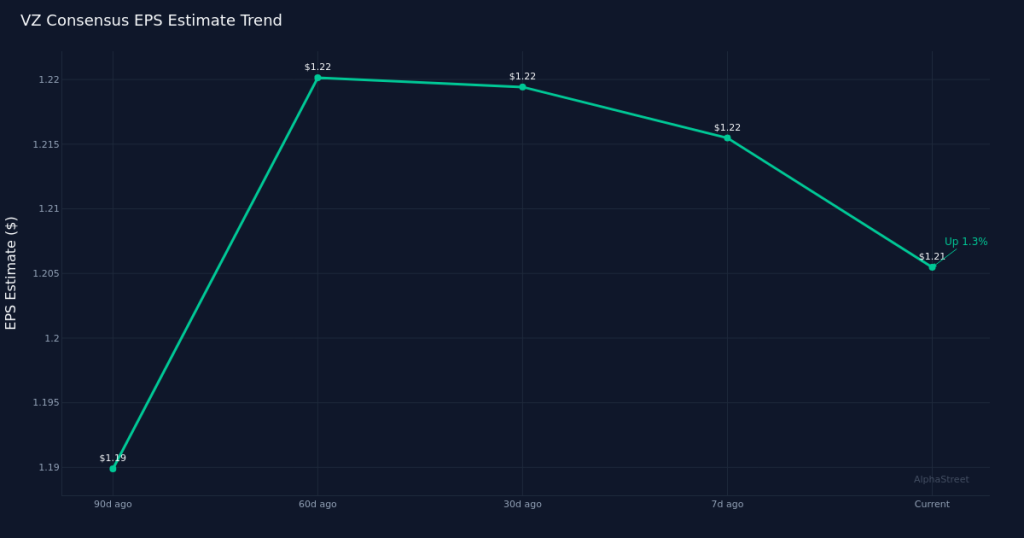

Recent estimate revisions paint a mixed picture of analyst confidence heading into the print. Over the past 30 days, the EPS consensus has drifted down 0.8% from $1.22, indicating some near-term caution among analysts as the quarter drew to a close. However, the 90-day view tells a different story, with estimates climbing 1.7% from $1.19, suggesting the longer-term trajectory remains constructive. This divergence between short-term pessimism and medium-term optimism often reflects analyst adjustments to quarterly timing issues rather than fundamental concern about the business.

The year-over-year comparison shows Verizon targeting steady but unspectacular expansion. Consensus revenue of $34.86B represents a 4.1% increase from the $33.48B reported in the first quarter of 2025, reflecting the incremental growth characteristic of mature telecom operators in a saturated domestic market. On the bottom line, the $1.21 EPS estimate implies 1.7% growth from the year-ago figure of $1.19, a slower pace than the top-line expansion. The year-ago quarter delivered $5.02B in net income on a 15.0% net margin, providing a profitability baseline against which to measure current performance. The modest EPS growth relative to revenue expansion suggests investors should monitor whether margin pressures from network investments or competitive dynamics are weighing on profitability.

Investor focus will center on several operational metrics that drive Verizon’s trajectory. Wireless subscriber trends remain the primary value driver, with postpaid phone net additions serving as the gold standard for measuring competitive positioning against AT&T and T-Mobile. Average revenue per user metrics will reveal whether promotional intensity has stabilized or intensified, while churn rates indicate customer satisfaction and network quality perception. On the infrastructure side, progress on C-band deployment and fixed wireless access subscriber growth will demonstrate Verizon’s ability to monetize its 5G investments. The fiber business continues to represent a growth vector, with broadband net additions providing diversification beyond traditional wireless. Free cash flow generation remains critical for supporting the dividend that attracts income-focused investors to the stock.

The stock’s positioning heading into the report reflects investor sentiment accumulated over recent months. Where shares trade relative to the 52-week range often signals whether expectations are elevated or subdued, though this context requires price data not provided in the verified dataset. The telecom sector’s defensive characteristics typically mean Verizon trades more on yield and stability than growth expectations, making the dividend coverage ratio and management’s capital allocation commentary particularly relevant during the earnings call.

Verizon’s track record on estimate accuracy will influence how the market interprets any variance from consensus. Companies that consistently beat or miss estimates train investors to position accordingly, though the specific beat/miss history for this company is not included in the available data. The narrow estimate ranges suggest analysts feel they have reasonable visibility into the quarter, which could amplify market reaction to any significant surprise.

Management guidance will carry substantial weight given the modest organic growth profile. Any updates to full-year wireless service revenue growth targets, adjusted EBITDA expectations, or free cash flow projections will move the stock more than the quarterly results themselves. Commentary on competitive dynamics, particularly pricing discipline across the industry, will signal whether the rational behavior that has supported margins can persist. Capital expenditure plans and network deployment timelines will clarify how much investment remains necessary to maintain competitive parity.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.