AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects steady performance from VICI Properties. Analysts are projecting earnings per share of $0.71 on revenue of $1.02 billion when the experiential real estate investment trust reports first-quarter 2026 results on April 30th. The consensus draws from 2 analysts, with revenue estimates ranging from $994.3 million to $1.04 billion and no variance in EPS forecasts across the coverage universe.

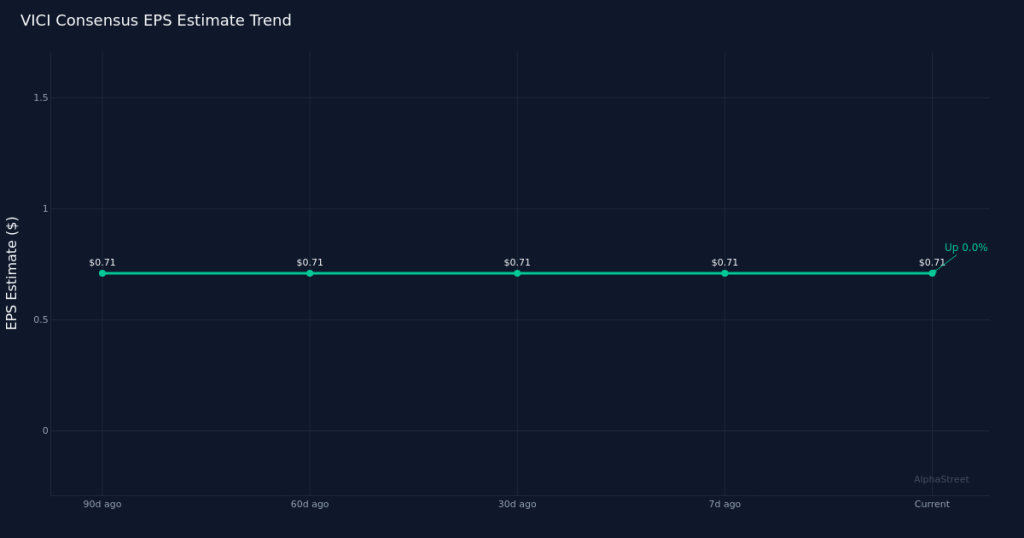

Estimates have held completely steady. Analyst projections for the quarter have remained unchanged over both the past 30 and 90 days, with EPS estimates sitting at $0.71 throughout the period. This stability in the estimate trajectory suggests analysts have maintained their conviction in VICI’s ability to deliver consistent results from its portfolio of experiential properties, with no material changes to underlying assumptions about occupancy, rent collection, or lease escalations during the winter months.

The consensus implies strong year-over-year growth. If VICI meets analyst expectations, earnings per share would rise 39.2% from the $0.51 reported in the first quarter of 2025, while revenue would advance 3.6% from the year-ago figure of $984.2 million. The substantial gap between EPS growth and revenue growth bears watching, as it suggests either improving operational leverage, lower interest expenses, or changes in the capital structure since last year. For context, VICI generated net income of $543.7 million in the year-ago quarter, representing a robust net margin of 55.2%, reflecting the high-margin nature of triple-net lease real estate income.

VICI operates as a pure-play experiential REIT. The company’s portfolio consists primarily of gaming, hospitality, and entertainment properties leased to leading operators under long-term triple-net lease agreements. This structure provides predictable cash flows with built-in rent escalators, insulating the REIT from most operating expenses while delivering steady income growth. The year-over-year comparisons reflect both organic rent growth from contractual escalations and the contribution from any acquisitions completed over the past twelve months, though specific property-level metrics from the prior quarter are not available in the current data set.

The stock’s recent positioning matters for sentiment. VICI’s share price performance heading into the print will influence how investors interpret results that meet, exceed, or fall short of the $0.71 EPS target. REITs trade on yield and growth expectations, so any divergence from consensus could trigger meaningful moves depending on whether the miss or beat affects the sustainability of the dividend or signals changes in the underlying property portfolio performance.

Investor focus will center on portfolio fundamentals. Beyond the headline EPS and revenue figures, shareholders will scrutinize lease coverage ratios from VICI’s tenants, particularly in the gaming segment where operator performance directly impacts lease sustainability. Any commentary on the acquisition pipeline, cost of capital, and leverage metrics will shape expectations for growth beyond the first quarter. Additionally, management’s updated guidance on full-year adjusted funds from operations (AFFO) and the dividend outlook will be critical, as REIT investors prioritize cash generation and distribution sustainability over traditional earnings metrics. The degree to which contractual rent escalators are flowing through to results versus being offset by higher financing costs will also be telling given the interest rate environment.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.