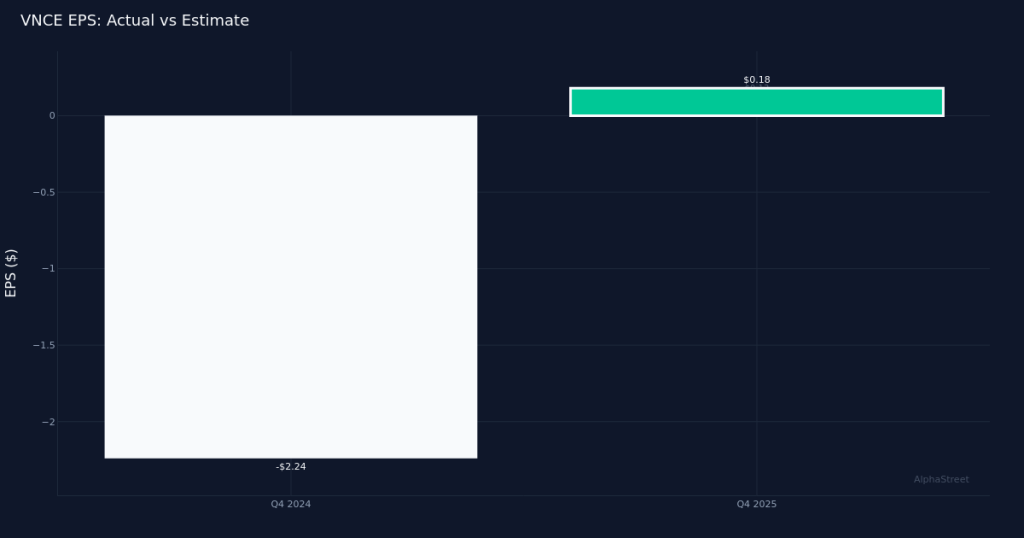

Strong beat. Vince Holding Corp. (NYSE: VNCE) reported Q4 2025 adjusted earnings of $0.18 per share, crushing the Wall Street consensus of $0.13 and delivering a 38.5% beat that sent shares surging 21% to $3.40. The apparel manufacturer generated $83.7M in revenue for the quarter, representing a 4.7% increase from the $80.0M recorded in Q4 2024, with adjusted net income reaching $2.4M. The results demonstrate that Vince’s transformation efforts are gaining traction as the company successfully navigates a challenging retail environment.

Revenue-driven performance. The quality of this earnings beat appears solid, underpinned by genuine top-line growth rather than aggressive cost management alone. The 4.7% revenue expansion year-over-year suggests improving brand momentum and customer engagement, particularly encouraging given the premium positioning of Vince’s product portfolio. This revenue-led performance provides a more sustainable foundation for profitability than margin engineering, signaling that the company’s merchandising strategies and product assortment are resonating with consumers willing to spend on elevated contemporary apparel.

Direct-to-consumer strength. The standout performance came from Vince’s direct-to-consumer segment, which led the company with $45.0M in revenue, up 10.4% year-over-year. This double-digit growth in DTC sales is particularly significant for an apparel manufacturer, as these channels typically deliver higher margins and provide greater control over brand presentation and customer experience. The +10.4% comparable metric for direct-to-consumer segment sales growth demonstrates that Vince is successfully capturing market share through its owned retail stores and e-commerce platform, reducing reliance on wholesale partners and department store distribution.

Market enthusiasm. The 21% stock price surge to $3.40 reflects investor optimism about Vince’s trajectory, with the market rewarding both the magnitude of the earnings beat and the underlying revenue momentum. This positive reaction suggests analysts and investors view the quarter as validation of the company’s strategic initiatives. Wall Street consensus currently stands at 5 buy ratings, 1 hold, and 0 sell recommendations, indicating broad analyst confidence in the company’s prospects despite the stock’s relatively modest absolute price level.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.