Lamb Weston Holdings, Inc. (NYSE: LW), a leading supplier of frozen potato and vegetable products, is all set to publish third-quarter 2024 financial results this week, after reporting double-digit earnings and revenue growth for the previous quarter. While there are concerns about the recent dip in volume growth, the company’s higher-margin business is expected to drive growth in the second half.

Lamb Weston’s stock traded sideways so far in 2024, after making a positive start to the year. It has gained 25% since slipping to a one-year low about six months ago. Market watchers, in general, are optimistic about the prospects of the stock. The shares are likely to gather further momentum and go beyond the levels seen in mid-2023 when they hit an all-time high. At the current valuation, LW looks like a good investment option that could deliver long-term shareholder value.

Q3 Report Due

The Eagle, Idaho-headquartered food processing company’s February-quarter results are expected to come on Thursday, April 4, at 8:30 a.m. ET. On average, Wall Street predicts a profit of $1.45 per share for the third quarter, excluding special items, which represents a modest increase from the $1.43/share the company earned a year earlier. The consensus estimate for net sales is $1.65 billion, vs. $1.25 billion in the prior-year quarter.

Lamb Weston has delivered positive sales and earnings performance in recent years, despite the challenging macro environment. The business benefited from pricing actions adopted by the management in response to inflation and a better product mix. Improvements in supply chain productivity also contributed to the bottom line. There has been a solid uptick in sales lately, due to recent acquisitions in Europe and South America.

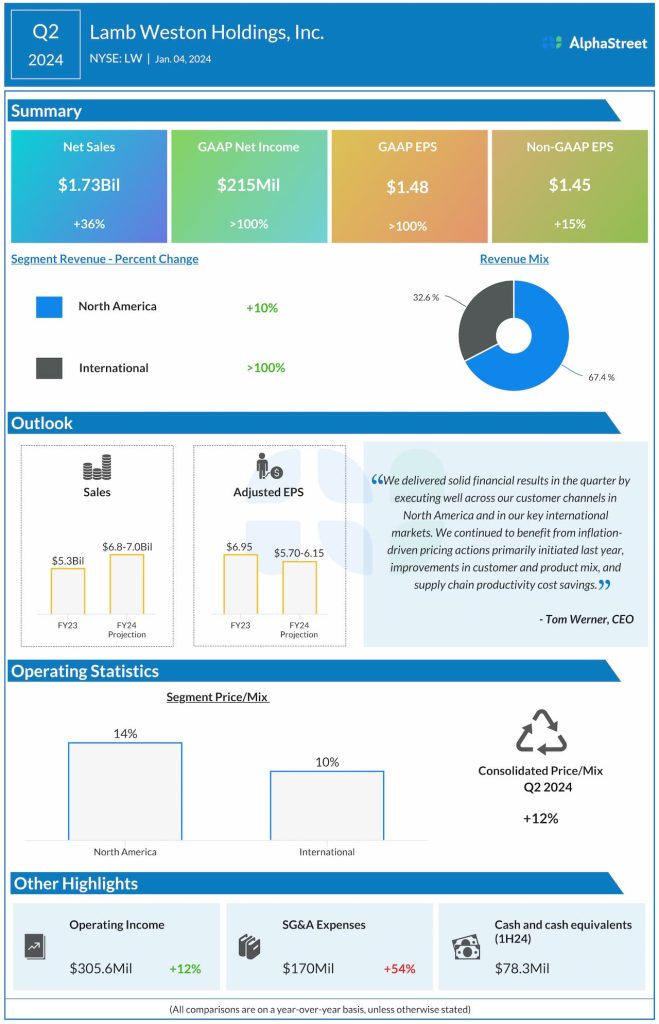

Record Sales

Net sales grew an impressive 36% to $1.73 billion in the second quarter when the core North American sales rose 10% and International sales more than doubled. The strong topline performance translated into a 15% increase in adjusted earnings to $1.45 per share. Both the top line and earnings exceeded estimates, marking the fifth consecutive beat.

From Lamb Weston’s Q2 2024 earnings call:

“We remain confident that our volume trends will continue to improve in the back half of fiscal 2024 as we begin to lap and backfill exited volumes with higher margin business. This includes our target for year-over-year volume growth in the fourth quarter. In addition, we expect our volumes will continue to recover in fiscal 2025 and have planned to contract for acres accordingly. While we are disappointed with the write-offs, the underlying fundamentals of the business, our operations, and the category remain solid.”

Outlook

For fiscal 2024, the management expects sales to be $6.8-$7.0 billion, the midpoint of which is up 30% from sales generated in the prior-year quarter. Meanwhile, full-year adjusted profit is expected to decline to $5.70-6.15 per share. Anticipating the operating environment to remain stable, the company is looking for sustained volume growth this year and beyond. In Q2, sales volumes declined, mainly reflecting the company’s decision to exit lower-price and lower-margin business.

LW has stayed close to its 52-week average so far this year. After opening Monday’s session lower, the stock traded down 1.5% in the afternoon.