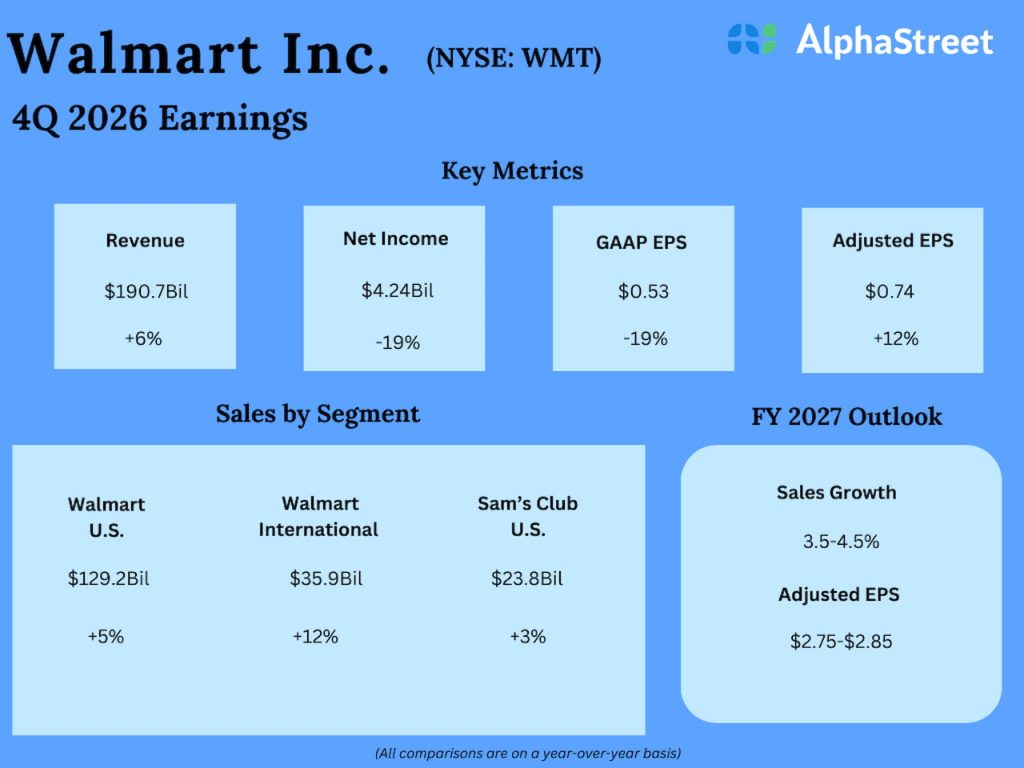

Walmart Inc. (NASDAQ: WMT) reports Q4 FY26 earnings with revenue of $190.7 billion, up 5.6% year-over-year. Walmart’s Q4 FY26 earnings show the company is executing its omnichannel strategy. Global eCommerce sales rose 24%. Operating income jumped 10.8%. This report marks a turning point in retail.

Market Position

Walmart holds a dominant position in U.S. retail. The company serves nearly 280 million customers weekly. Its stock trades on the NASDAQ under ticker WMT. Walmart’s Q4 FY26 earnings confirm the retailer’s market dominance. Execution continues across all segments.

Financial Results

Q4 FY26 delivered robust performance. Revenue reached $190.7 billion, up 5.6%. Also, this outpaced the prior year. Operating income grew faster at 10.8%. So, gross margin expanded 13 basis points. The company achieved better expense leverage. In fact, adjusted operating income grew 10.5% in constant currency.

Full Year FY26 Results

Walmart’s full-year fiscal 2026 results show momentum. Net sales reached $713.2 billion, up 4.7%. Also, operating income grew 1.6% on a reported basis. Adjusted basis showed 5.4% growth in constant currency. Plus, operating cash flow jumped $5.1 billion to $41.6 billion. Free cash flow increased $2.3 billion to $14.9 billion.

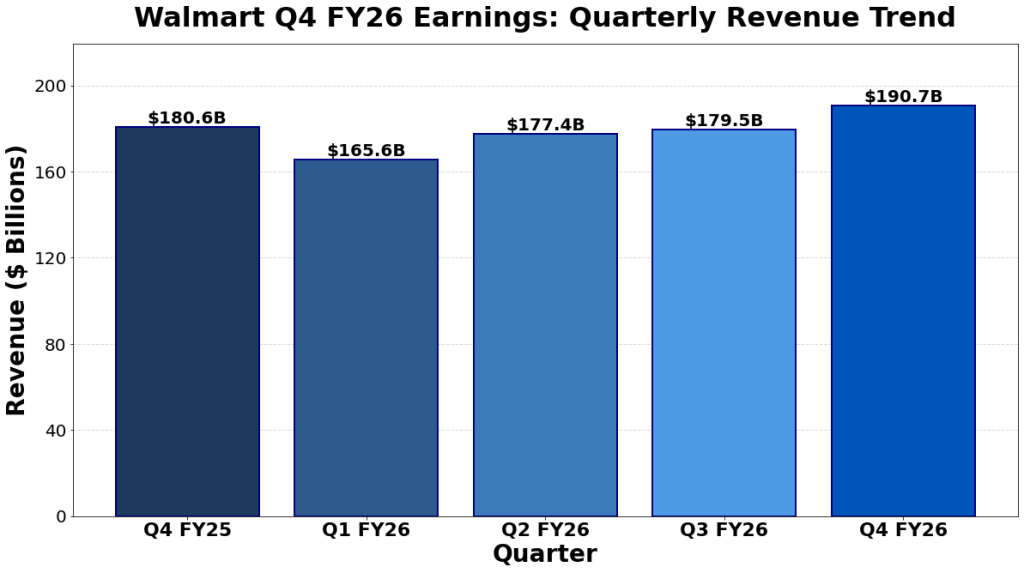

Walmart Q4 FY26 earnings show increasing quarterly revenue momentum from Q4 FY25 through Q4 FY26.

eCommerce Growth

eCommerce growth continues to accelerate. Global eCommerce sales surged 24%. So, this represented 23% of total net sales. Store-fulfilled pickup and delivery channels grew over 50%. Also, marketplace sales expanded across all regions. Membership revenue grew 15.1% globally. Plus, advertising sales jumped 37%. Walmart Connect in the U.S. rose 41%.

Segment Performance in Q4 FY26

Walmart U.S. net sales grew 4.6% to $129.2 billion. Comp sales (excluding fuel) rose 4.6%. Also, eCommerce contribution to comp sales reached 520 basis points. Operating income increased 6.6% to $7.0 billion. Meanwhile, Walmart International net sales reached $35.9 billion, up 11.5%. Operating income jumped 36.0% to $1.9 billion. Plus, Sam’s Club U.S. net sales grew 2.9% to $23.8 billion. Operating income rose 3.8% to $596 million.

Forward Guidance

Management provided detailed guidance for FY27. Net sales are expected to grow 3.5%-4.5% in constant currency. Also, adjusted operating income will grow 6.0%-8.0% in constant currency. Interest expense will increase approximately $200 million-$300 million. So, the effective tax rate is expected to be 23.5%-24.5%. Capital expenditures will be approximately 3.5% of net sales. Plus, channel expansion continues to support long-term growth.

Key Takeaways from Walmart Q4 FY26 Earnings

Walmart continues to execute well in a competitive environment. Also, the company is leveraging omnichannel capabilities effectively. eCommerce remains a key growth driver at 24% growth. Plus, membership revenue and advertising sales demonstrate diversification. In fact, margin expansion reflects operational leverage. So, management shows confidence in continued growth. Overall, FY27 guidance reflects healthy market positioning.