Walmart Inc. (NYSE: WMT) has consistently delivered stable performance across various market conditions, with the company’s focus on grocery and other consumer essentials driving store traffic. The retail giant’s rapidly growing digital platform enhances the reach and efficiency of its extensive store network, providing significant convenience to shoppers. Walmart is expected to report third-quarter results on November 19, before the opening bell.

At the Bourses

Walmart’s stock is doing well ahead of the earnings, after gaining 25% in the past three months. The shares set a new record and outperformed the market this week. WMT has long been an investors’ favorite, and it remains a compelling long-term investment despite the recent rally. The company is building an ecosystem with focus on third-party marketplace, which could drive strong revenue and earnings growth in the future.

When the company releases its third-quarter report, Wall Street will be looking for earnings of $0.53 per share on revenues of $166.44 billion. In the year-ago quarter, the company earned $0.51 per share and generated revenues of $159.44 billion. The EPS estimate is slightly above the management’s guidance of $0.51-0.52 per share. It forecasts a 3.25-4.25% growth in Q3 sales, in constant currency. The report is slated for release on Tuesday, November 19, at 7:00 am ET.

Power of Scale

For the company, expanding its e-commerce platform has been a key priority lately, a strategy that is expected to narrow the gap between Walmart and industry leader Amazon, in the digital space. The recent improvement in consumer spending and lower interest rates bode well for the company, which has a history of effectively navigating macroeconomic challenges. Walmart’s healthy cash position gives it an edge over competitors like Kroger when it comes to spending heavily on growth initiatives. In the past four years, its free cash flow, after dividends, averaged around $9 billion.

From Walmart’s Q2 2025 earnings call:

“Our business outside the U.S. continues to lift the total company in terms of sales and profit growth. Walmex had another strong quarter, and India Flipkart again delivered positive contribution margin, and PhonePe continues to deliver amazing growth in total payment volume. In China, strong membership trends in Sam’s Club continued to drive double-digit sales growth, and about half of our sales there are digital. We continue to gain market share, including in general merchandise, and transaction counts and unit volume are up across markets.”

Q2 Results Beat

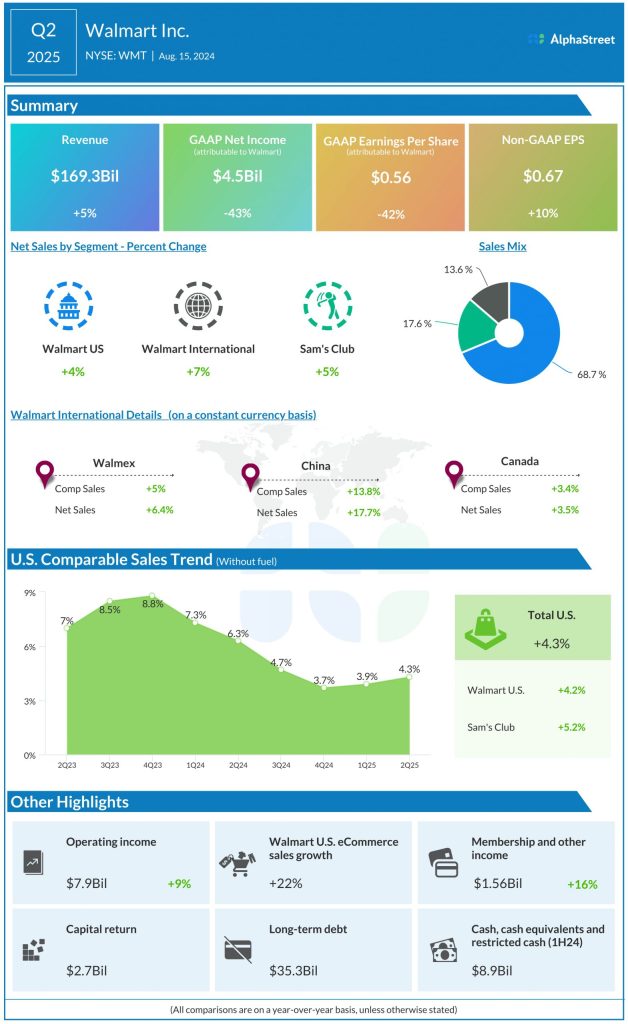

The company has an impressive track record of delivering stronger-than-expected quarterly results, including in the July quarter when revenue grew 5% to $169.3 billion. Second-quarter profit, adjusted for one-off items, increased 10% year-over-year to $0.67 per share. Net income attributable to the company, on a reported basis, was $4.5 billion or $0.56 per share. The management said it expects full-year sales to increase 3.75-4.75% YoY in constant currency. Adjusted earnings per share is expected to be $2.35-2.43 in FY25.

The stock price more than doubled in the past two years, continuing the long-term trend. On Thursday, the shares opened above $85 and traded slightly lower.