On the heels of relatively strong earnings performance by major banks driven by lower allowance to credit losses and stronger-than-expected trading, Washington Trust Bancorp (NASDAQ: WASH) last week reported Q3 results that surpassed street expectations. In a post-earnings interview with AlphaStreet, executives of the Rhode Island-based community bank responded to five key questions on the fundamental strength of the firm, as well as views on the overall industry.

Tiding through the pandemic period

COO MARK GIM: As a 220-year-old financial institution, we have had a long history of a very conservative approach to both credit quality and concentrations. We tend to have less credit sensitivity to downward financial cycles, even in an environment such as today’s where the cause and scope of the economic downturn are very different from 2008-09.

Our history in the 2008-09 downturn was far better than our peers. And so, while bank stocks have been discounted today on the expectation of credit losses resulting from COVID, we are hopeful that care and attention to credit quality will produce similar outperformance this time.

Operating in a low-interest environment

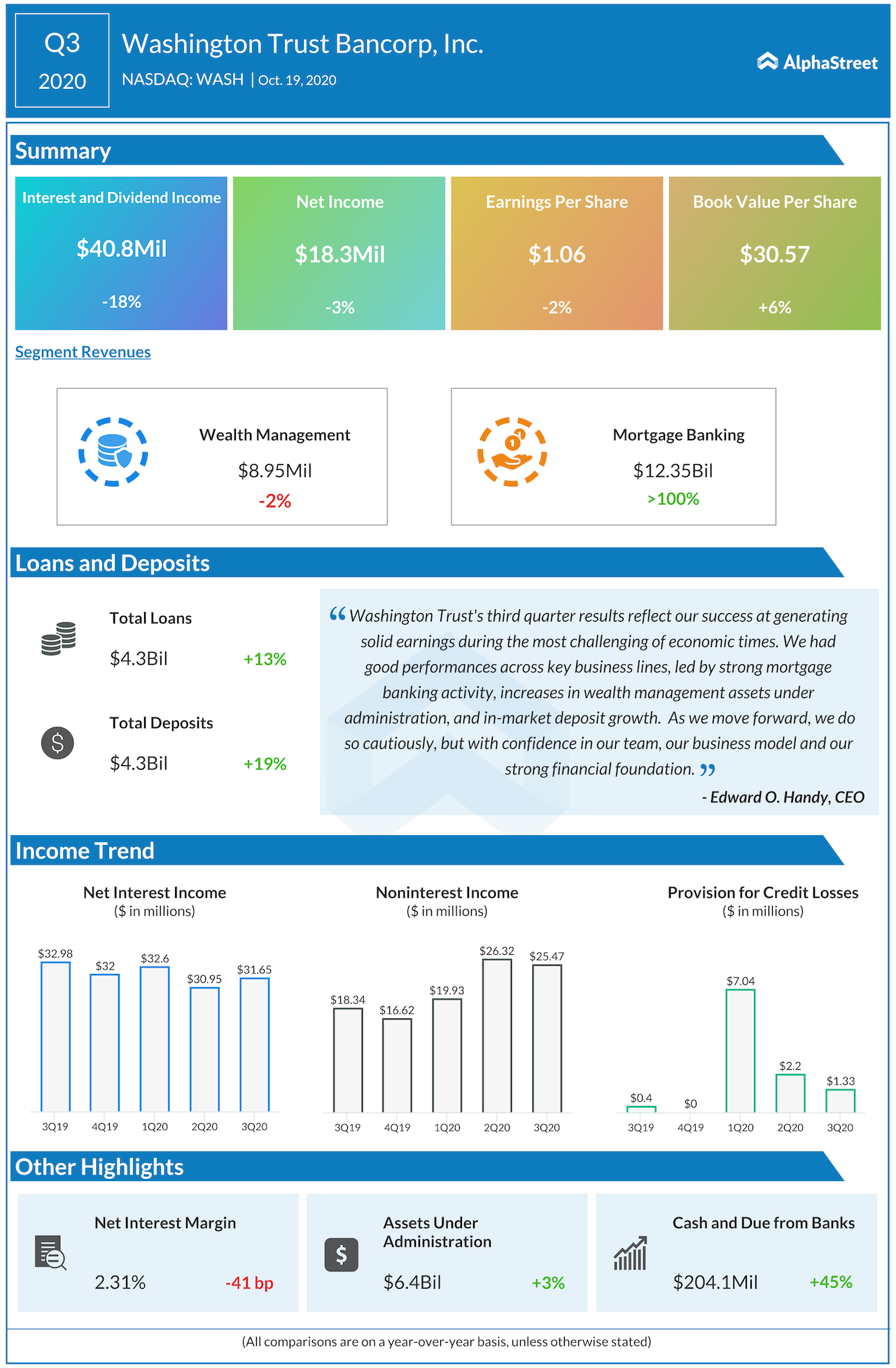

Bad loans aren’t the only major threat faced by banks. Low interest rates have weighed on the net interest margins for most banks, including Washington Trust. During the third quarter, the community bank’s NIM shrunk 41 basis points to 2.31%.

CFO RONALD OHSBERG: In terms of overall margin management, we do have an opportunity to lower our funding costs over the next couple of quarters. We have about $1.1 billion of variable-rate funding that will roll over in the next two quarters. The average rate on that is about 1.1%. While we do see some diminishment in the asset yield, we think that would be more than offset by liability rate reductions.

He added that there has been no significant impact of PPP loans on the margins so far. The bank had a portfolio of 1,770 PPP (Paycheck Protection Program) loans totaling $217 million, as of September 30, with an average loan size of approximately $122,000.

CEO EDWARD (NED) HANDY: It was something new for us. We did the front-end of that (PPP) internally, but it’s been a complicated process. We had to get about 10% of our employees involved in one way or another. And so a question that we will ask ourselves is if it came around again, would we automate it to a third party to avoid additional stress in the system. And we might rethink that and prepare ourselves better.

On provision for credit losses and expected delinquencies

In the third quarter, Washington Trust reported just $1.3 million in provision from credit losses, compared to $2.2 million in Q2 and $7 million in Q1. Though banks have generally lowered their allowances for bad debts, there is a general concern that delinquencies could increase by the second half of next year.

RON: There’s obviously still uncertainty as to how the credit picture ultimately plays out. If it is out the way we expect them at this time, we would have enough reserves to ride out the situation. Our deferments reduced by 50% from the second quarter to the third quarter. We think they could drop by half again by year-end to about 4%.

The nature of the loans that we think are going to need an extended period of time to stabilize – hospitality businesses, parking lots, movie theatres – will probably need some more time. And so we are structuring these deferments in such a way to provide our customers with the time that they need to get their feet back underneath them. So we certainly feel at this time that we are adequately reserved unless something unexpected happens.

NED: We are all hopeful that the government comes to some kind of a decision for an additional package because frankly, it is needed to get through this. But I think in its absence, we have our arm around the portfolio and think that the tracking of our deferments has put us in a really good place in terms of knowing what to expect.

Achieving exceptional residential mortgages

Washington Trust continued to see strong performance in mortgage banking in the third quarter. Revenue jumped 155% riding on low interest rates and a relatively strong Boston economy.

MARK: The absolute level of falling rates has unquestionably helped both mortgage refinancing of existing loans, besides supporting strong fundamentals for the housing market in New England. There is a relative lack of supply, and as rates drop, the affordability of housing versus renting is improving. And it also provides, to some homeowners, a hedge against falling asset values in the stock markets.

We have been careful about expanding our residential mortgage operation but it extends beyond our retail branch footprint, into the Metropolitan Boston area, New England, and in residential areas of the Hartford area in Fairfield County and Connecticut as well.

And that has translated into significantly increased volumes of mortgages. To some extent that is counterbalanced by payoffs of mortgages as they refinance, either with us or away from us. But the sustainability of the mortgage boom, throughout the second and third quarter, has been remarkably strong, it has helped us offset a lower NIM. We think that this activity should persist into late 2020 and early 2021.

Stimulus and recovery

NED: When you look at our PPP portfolio, our average loan size run was a little over $100,000. So we were definitely targeting those loans at small businesses. A lot of those businesses continue to be challenged by COVID restrictions. Some of them have gradually come back and seem to be doing okay, but I think that more stimulus is needed. I think a lot of them would not survive long term if there isn’t another stimulus package.

If there is one, I think we will have a V-shaped recovery. Otherwise, some types of borrowers will do better than others. And we might have some inequality in the kind of recovery that occurs.

____

For more insights into Washington Trust, read the latest earnings call transcript here.