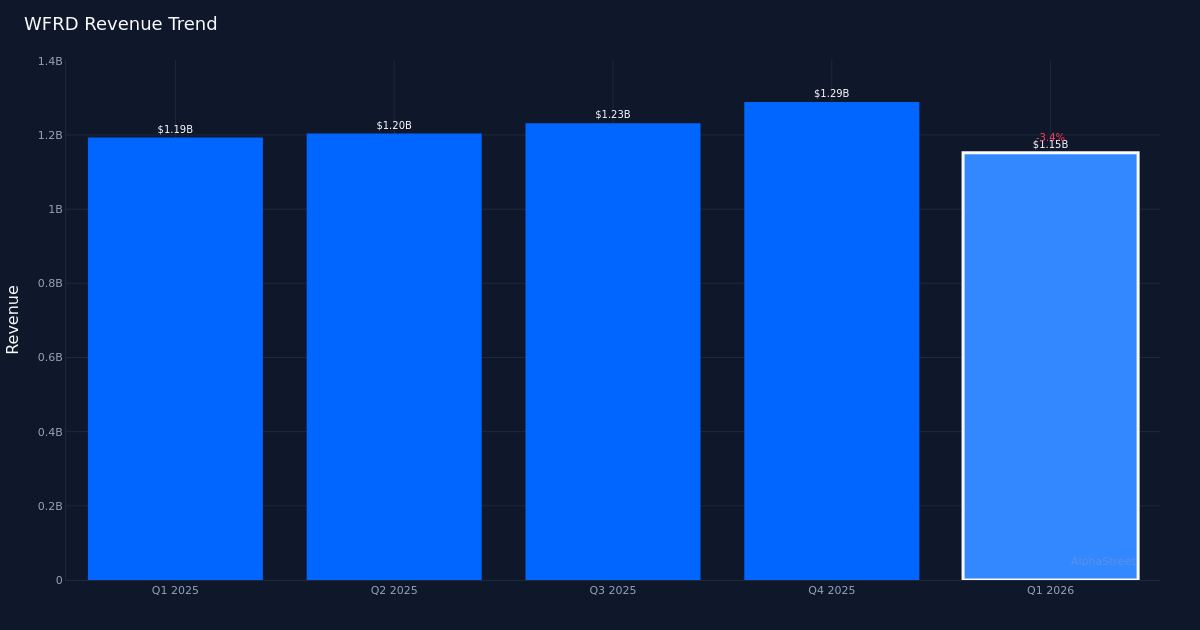

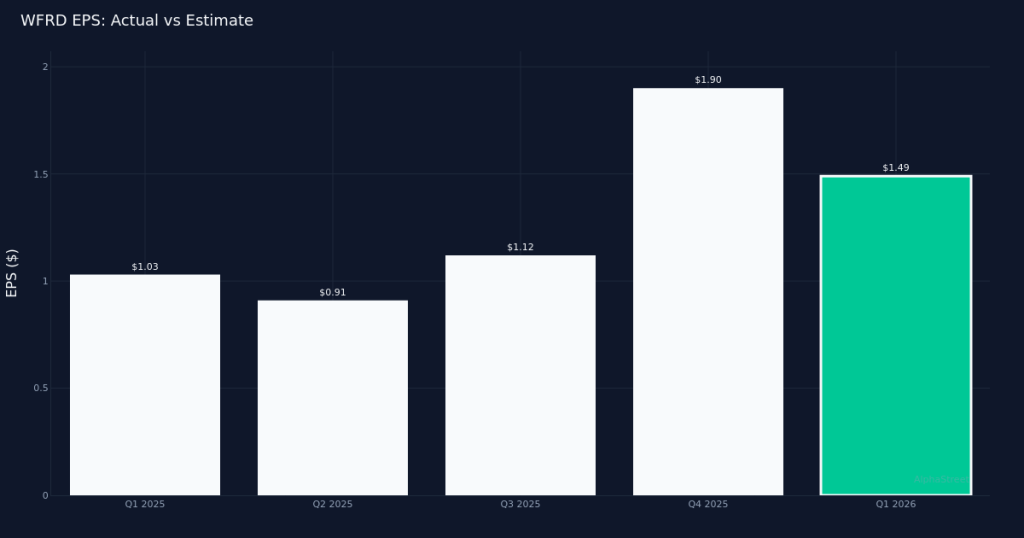

Solid Beat. Weatherford International plc (NASDAQ:WFRD) delivered a strong earnings performance in Q1 2026, posting diluted EPS of $1.49 against Wall Street’s $1.07 estimate, representing a beat by 39.3%. The company generated $1.15B in revenue for the quarter, while net income reached $108.0M. Year-over-year, EPS moved up 44.7% from the $1.03 posted in Q1 2025, though revenue declined 3.0% from the $1.19B recorded in the prior-year period. The stock traded largely unchanged following the report, suggesting investors may have expected the strong bottom-line performance or remain cautious about the top-line trajectory.

Mixed Quality. The earnings beat warrants closer examination given the divergence between profit and revenue trends. While the 44.7% year-over-year EPS growth is impressive, it came alongside a 3.0% revenue decline, raising questions about the sustainability of margin expansion in the oil and gas equipment and services sector. The company’s adjusted EBITDA was $233 for the quarter, providing additional context to operational profitability. This performance suggests margin discipline and cost management have played a meaningful role in driving the bottom line, which can be effective in the near term but may prove challenging to maintain if revenue headwinds persist.

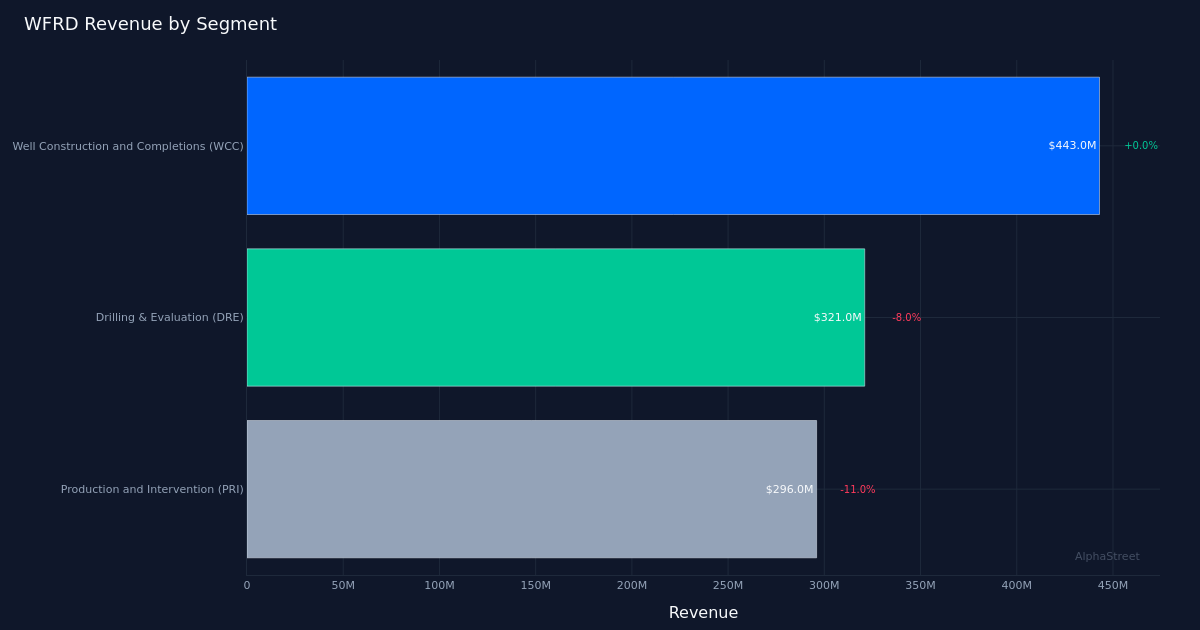

Segment Performance. Well Construction and Completions (WCC) led the company’s portfolio with $443.0M in revenue, flat year-over-year at down 0.0%. For a company operating in the cyclical energy services industry, maintaining segment revenue stability while the overall business contracts 3.0% indicates this division is holding up relatively well amid what appears to be a softer demand environment. The WCC segment’s performance will be critical to monitor as a bellwether for activity levels in global drilling and completion markets.

Analyst Sentiment. Wall Street maintains a constructive view on Weatherford shares, with consensus standing at 10 buy, 3 hold, and 0 sell ratings. The absence of any sell recommendations reflects confidence in the company’s market position within oil and gas services, though the presence of three hold ratings suggests some analysts are taking a wait-and-see approach, possibly concerned about revenue momentum or macro headwinds facing the sector.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.