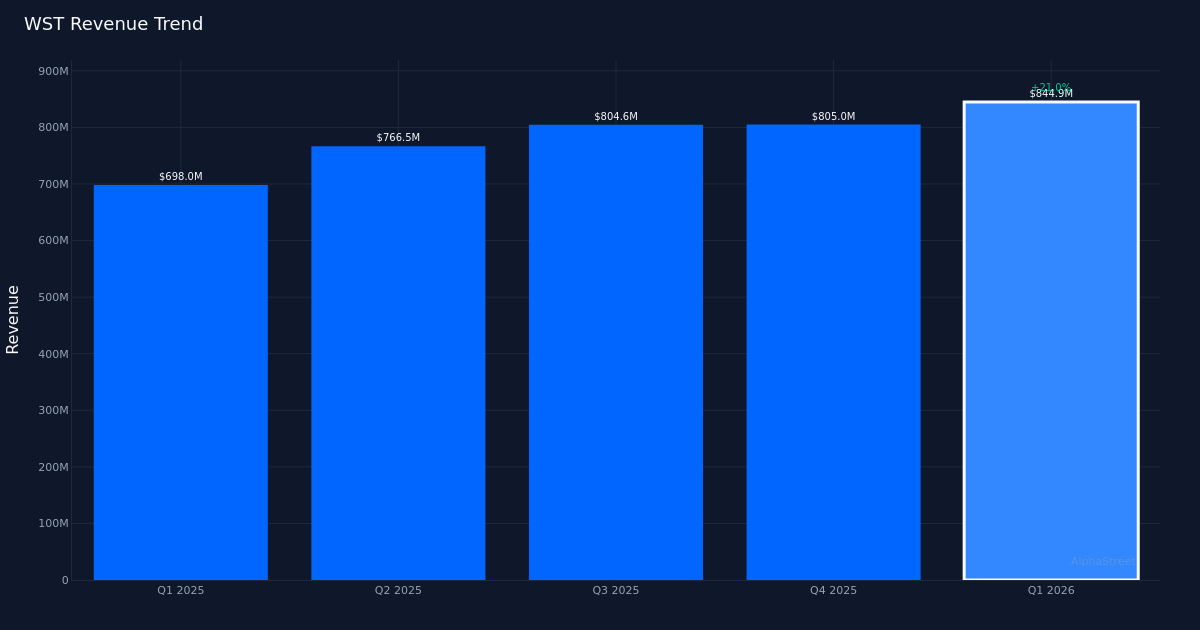

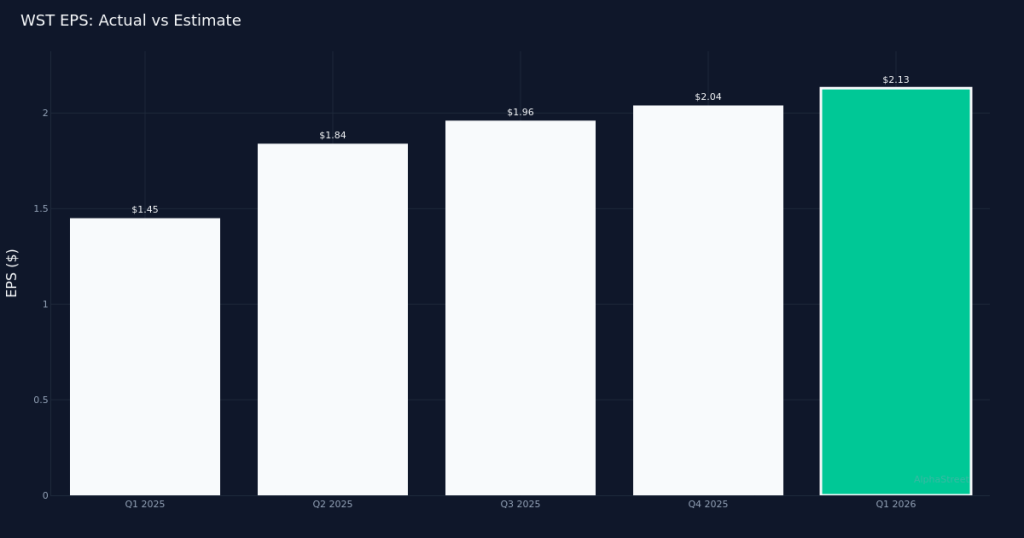

Strong beat. West Pharmaceutical Services, Inc. (NYSE:WST) delivered Q1 2026 adjusted earnings of $2.13 per share, crushing the $1.69 consensus by 26.0% and underscoring the company’s strong positioning in the pharmaceutical packaging and delivery systems market. Revenue reached $844.9M for the quarter, marking a robust 21.0% increase from the $698.0M recorded in Q1 2025. The company posted adjusted net income of $154.3M as demand for its high-value containment and delivery solutions remained elevated.

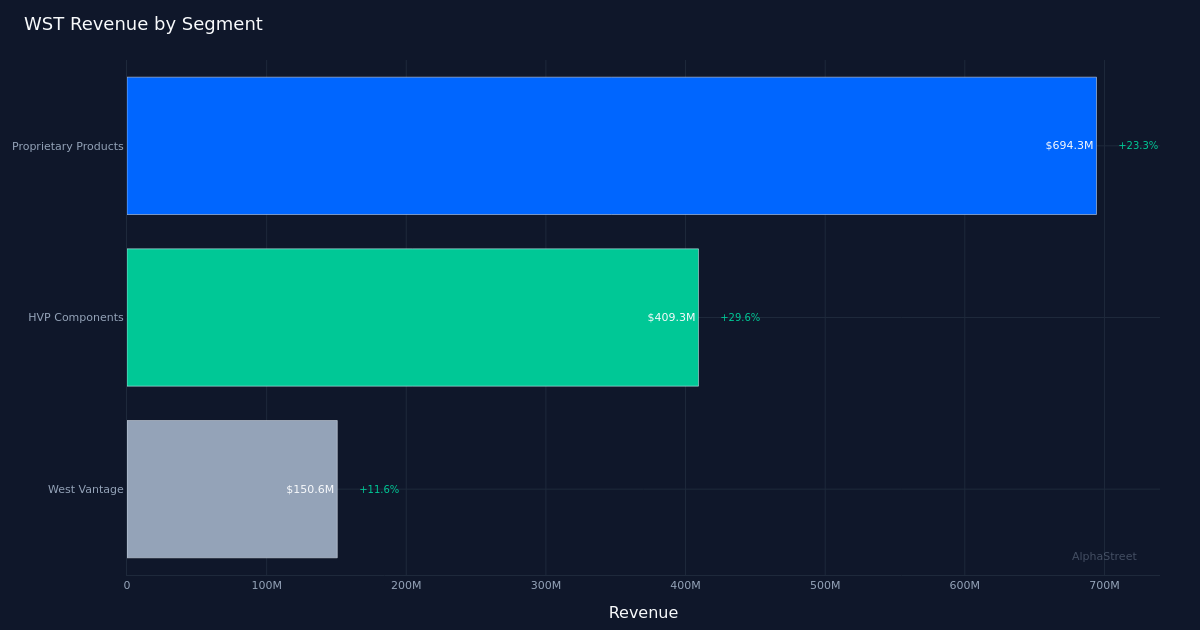

Revenue-driven performance. The quality of this beat appears solid, fueled by top-line expansion rather than merely cost management. Organic growth of 15.3% for the quarter signals genuine market share gains and underlying demand strength, particularly important in the medical instruments and supplies sector where volume growth reflects real manufacturing activity. The Proprietary Products segment demonstrated the company’s competitive advantage, generating $694.3M in revenue with a 23.3% year-over-year increase. This segment, which includes high-margin containment and delivery components for injectable medicines, continues to benefit from the pharmaceutical industry’s growing reliance on biologics and advanced therapies.

Guidance framework. Management provided a confident outlook for fiscal 2026, projecting adjusted EPS in the $8.40 to $8.75 range alongside revenue expectations of $3.29B to $3.35B. This forward guidance suggests management sees continued momentum in customer demand, likely driven by ongoing strength in biologics production and GLP-1 medication delivery systems. The guidance range implies sequential improvement throughout the year, positioning the company to sustain its growth trajectory beyond the first quarter’s exceptional performance.

Muted market reaction. Despite the substantial earnings beat and healthy revenue growth, shares traded largely unchanged following the report. This tepid response may reflect investor expectations that had already incorporated strong performance given recent pharmaceutical industry tailwinds, or perhaps concern about valuation multiples in the medical supplies space. Alternatively, the market may be adopting a wait-and-see approach regarding sustainability of the growth rates demonstrated this quarter.

Analyst positioning. Wall Street maintains a constructive view on the stock, with consensus standing at 12 buy ratings, 5 hold ratings, and zero sell recommendations. This skew toward positive ratings reflects confidence in West Pharmaceutical’s market position as a critical supplier to the pharmaceutical industry, where switching costs remain high and quality standards create meaningful barriers to entry.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.