WAB|EPS $2.71 vs $2.54 est (+6.7%)|Rev $2.95B|Net Income $362.0M

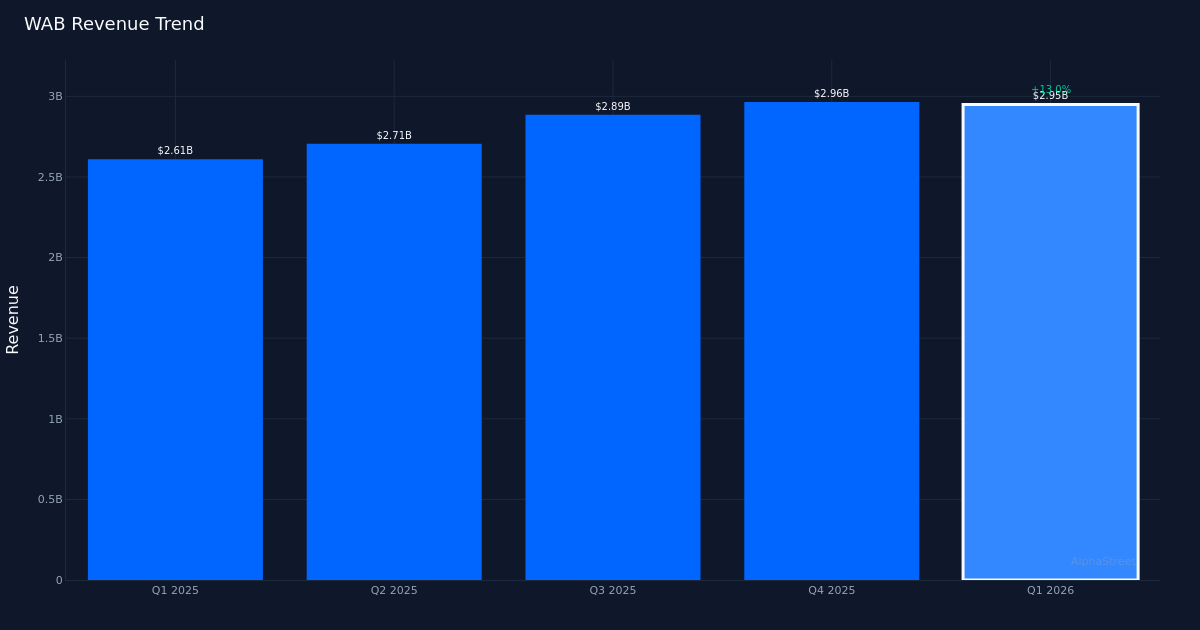

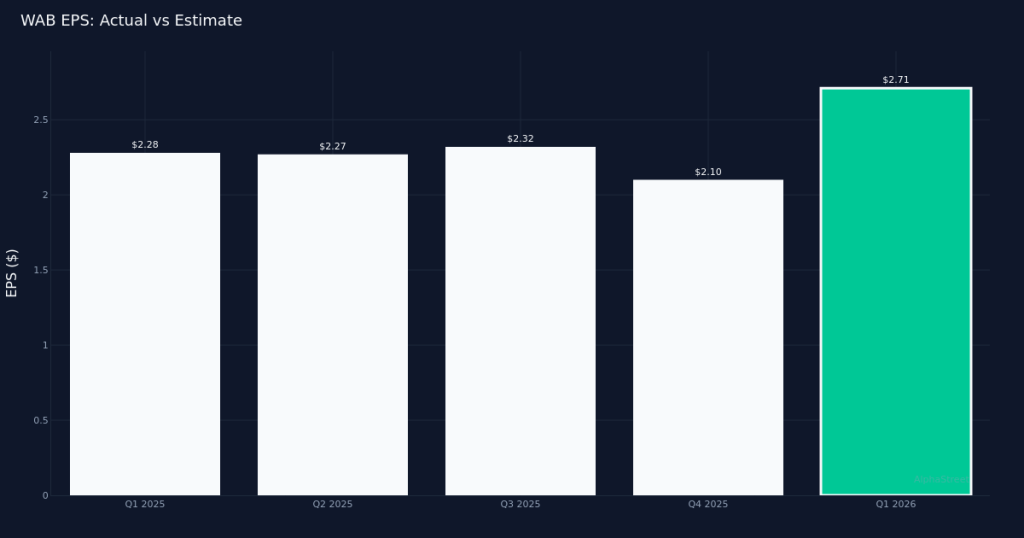

WAB|EPS $2.71 vs $2.54 est (+6.7%)|Rev $2.95B|Net Income $362.0MSolid Beat. Westinghouse Air Brake Technologies Corporation (WAB) delivered Q1 2026 adjusted diluted EPS earnings of $2.71 per share, surpassing analysts’ $2.54 forecast by 6.7%, demonstrating continued execution strength in the rail equipment supplier’s core markets. Revenue totaled $2.95B for the quarter, representing a 13.0% increase from the $2.61B recorded in Q1 2025. Net income reached $462.0M for the quarter, underscoring the quality of the earnings beat as top-line growth drove profitability expansion rather than solely cost-cutting measures.

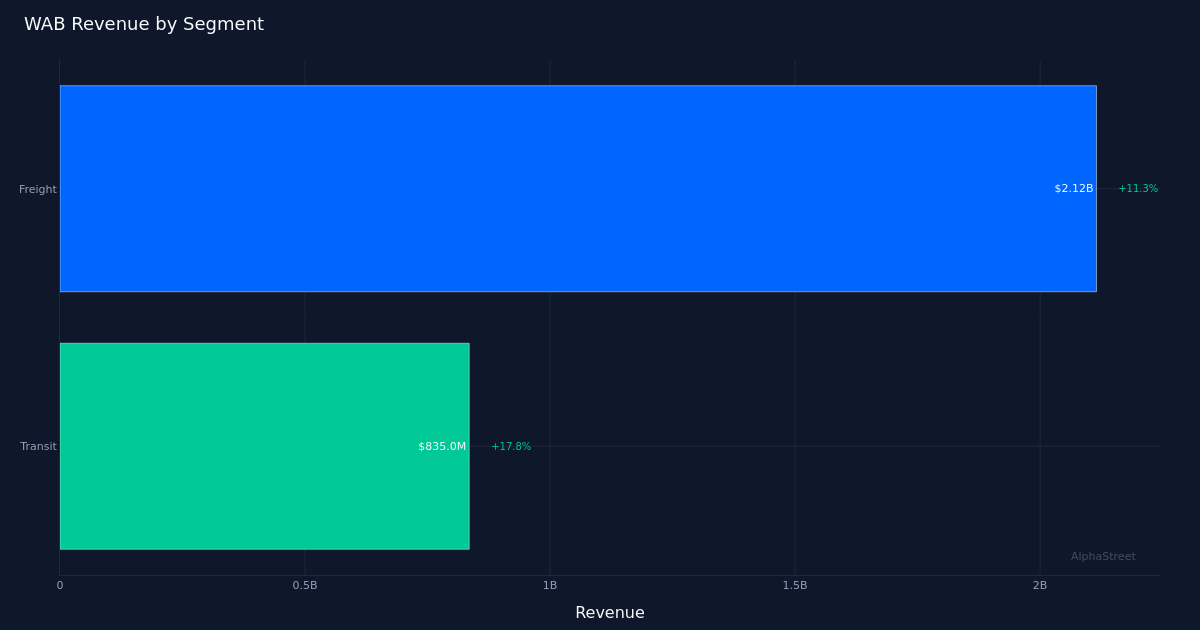

Freight Strength Leads. The company’s Freight segment powered results, generating $2.12B in revenue with 11.3% year-over-year growth. This performance reflects robust demand across Westinghouse Air Brake’s core railcar components, braking systems, and digital solutions as North American freight operators continue to modernize aging fleets. The segment’s double-digit growth trajectory demonstrates that the secular shift toward more efficient, technology-enabled rail operations remains intact despite broader economic uncertainty.

Backlog Momentum Building. The company operated 30,802,000,000 in total backlog at quarter end, while 12-month backlog growth accelerated to 12.8% for the quarter. This sequential improvement in order intake provides strong visibility into second-half revenue conversion and suggests customers are committing to multi-year equipment upgrades. The backlog expansion across both freight and transit customers indicates that Westinghouse Air Brake’s competitive positioning in digital locomotive solutions and aftermarket services continues to resonate with operators focused on reliability and operating ratio improvements.

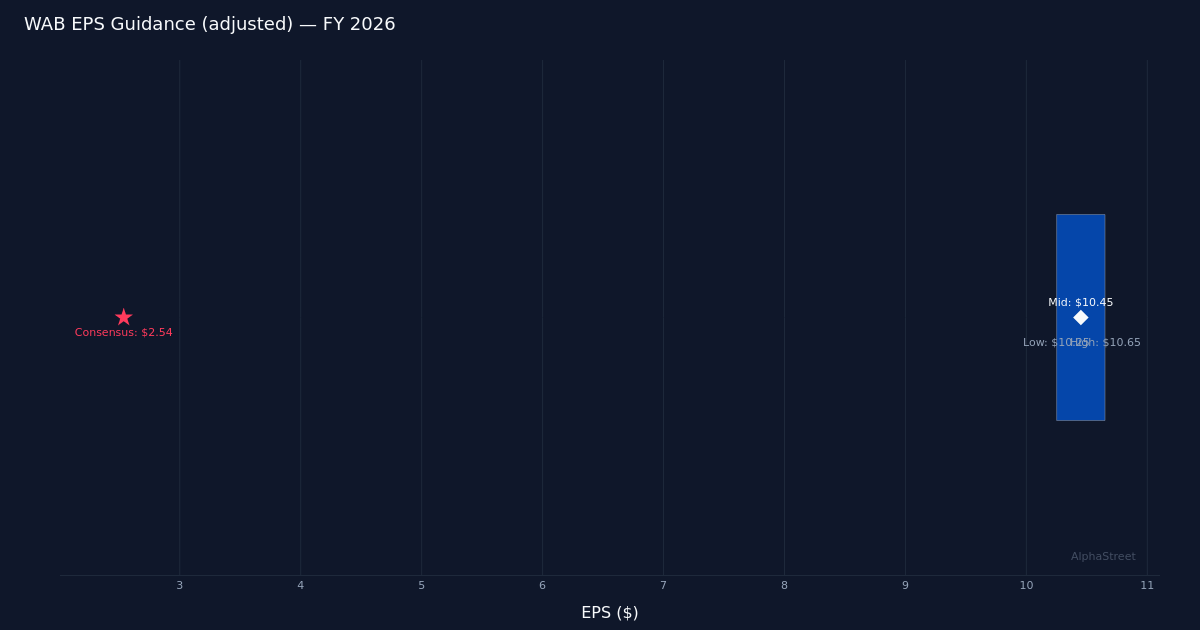

Guidance Affirms Confidence. Management guided FY 2026 adjusted EPS to $10.25 to $10.65, while revenue expectations range from $12.19B to $12.49B. The guidance implies continued momentum through the balance of the year, with the midpoint suggesting sequential acceleration from Q1’s performance. The company’s willingness to maintain this outlook despite macroeconomic headwinds reflects confidence in backlog conversion rates and the resilience of freight and transit capital spending budgets.

Market Reaction Overdone. Shares traded down 2.5% to $257.63 following the report, a puzzling response given the across-the-board beat and reaffirmed guidance. The sell-off likely reflects profit-taking after the stock’s recent run rather than fundamental concerns, particularly as Wall Street consensus stands at 7 buy ratings, 5 hold ratings, and 0 sell recommendations. The analyst community clearly views the current setup favorably, with the backlog growth and margin expansion supporting the bullish thesis.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.