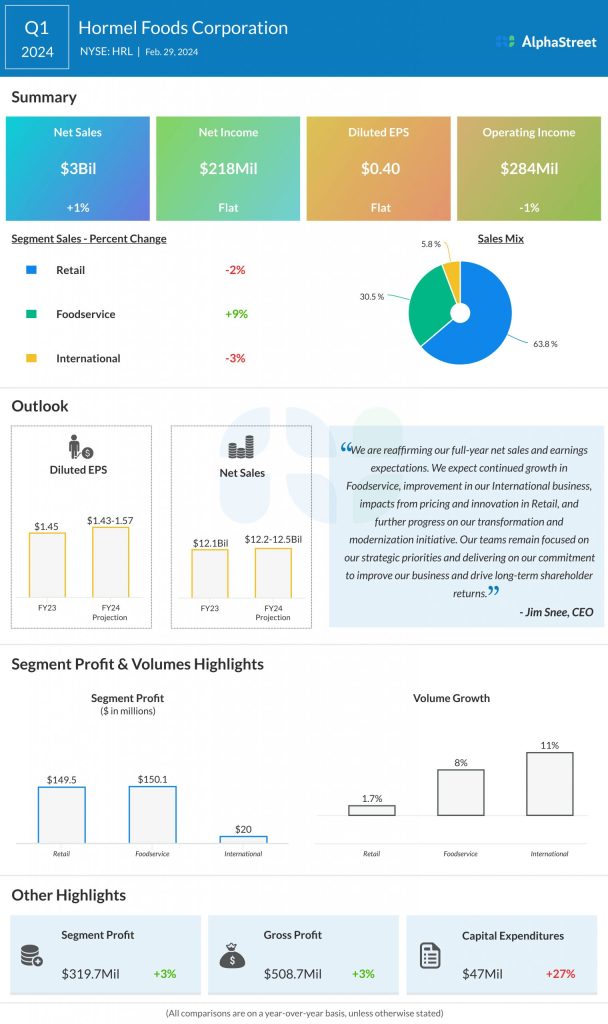

Shares of Hormel Foods Corporation (NYSE: HRL) dipped over 1% on Tuesday. The stock has gained 13% over the past three months. The company is slated to report its second quarter 2024 earnings results on Thursday, May 30, before markets open. Here’s a look at what to expect from the earnings report:

Revenue

Analysts are projecting revenue of $2.97 billion for Hormel in Q2 2024. This compares to sales of $2.98 billion reported in the same quarter a year ago. In the first quarter of 2024, sales rose nearly 1% to $2.99 billion.

Earnings

The consensus target for Q2 2024 EPS is $0.36, which compares to EPS of $0.40 reported in Q2 2023. In Q1 2024, adjusted EPS was $0.41.

Points to note

Last quarter, Hormel saw broad-based volume growth across its businesses, helped by brand strength and solid demand for foodservice products. It benefited from strong retail demand for products such as Skippy peanut butter, Planters snack nuts, and Hormel pepperoni, which led to volume and sales growth.

On its earnings call, the company said it expects higher sales across many of its verticals in retail for the full year, which could be a positive sign for the second quarter. It also expects the retail business to face pressure from whole bird turkey dynamics and an uncertain consumer backdrop.

Hormel’s foodservice business benefited from strong volume and sales growth last quarter, helped by gains in premium bacon and prepared proteins, poultry, and snacking. For the year, the company expects volume and sales gains to be led by turkey, pepperoni and bacon, which bodes well for Q2.

Hormel is also expected to benefit from momentum in the international business, which is expected to accelerate over the year, helped by the Skippy and SPAM brands, and refrigerated items. This momentum can be expected to benefit Q2 results as well.