Shares of Hormel Foods Corporation (NYSE: HRL) were up over 1% on Tuesday. The stock has gained over 6% in the past three months. The branded food company is set to report its third quarter 2024 earnings results on Wednesday, September 4, before market open. Here’s what to expect from the earnings report:

Revenue

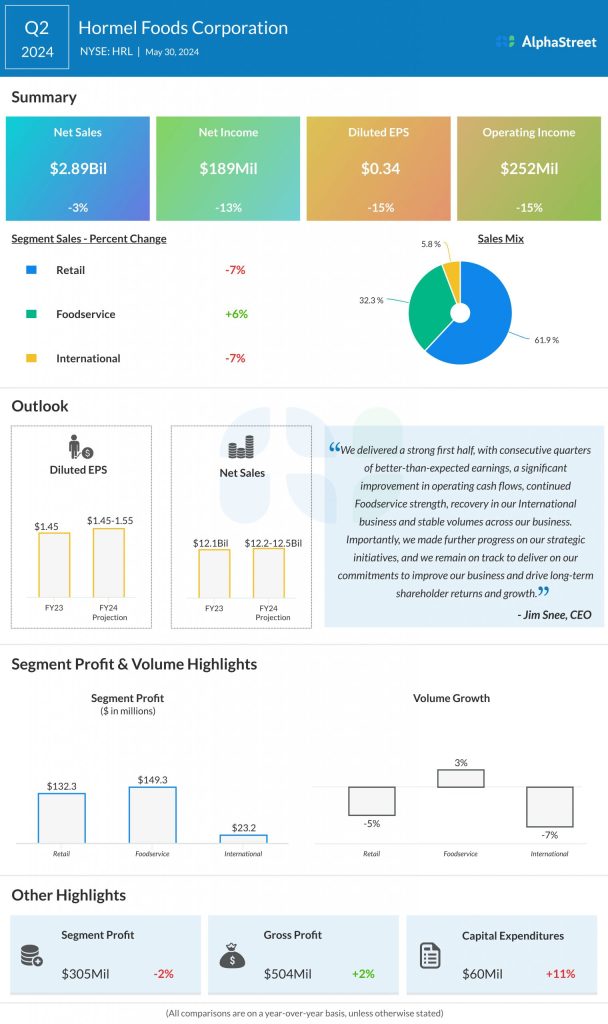

Analysts are projecting revenues of $2.95 billion for Hormel for the third quarter of 2024. This compares to net sales of $3 billion reported in the third quarter of 2023. In the second quarter of 2024, net sales decreased 3% year-over-year to $2.89 billion.

Earnings

Hormel expects its Q3 2024 adjusted EPS to be lower compared to the prior-year quarter and the previous quarter. The consensus target for EPS is $0.36. This compares to adjusted EPS of $0.40 reported in Q3 2023 and $0.38 reported in Q2 2024.

Points to note

Hormel expects its earnings in the third quarter to be pressured by lower volumes and pricing for commodity whole turkeys, as well as an unplanned production interruption at its Planters facility in Suffolk, Virginia.

The headwinds in whole turkey and the Suffolk production interruption are anticipated to take a toll on sales as well during the back half of the year. In Q2, sales in the Retail segment decreased year-over-year due to lower volume and pricing for whole-bird turkeys and lower sales in the convenient meals and proteins vertical.

The company also saw sales in the International segment fall last quarter due to lower commodity export volumes and lower net sales in China. The Foodservice segment recorded sales growth in Q2 helped by strength in bacon, premium prepared proteins and turkey.

Hormel expects to see strength in Foodservice continue in the back half of the year, which bodes well for the third quarter. The company expects to see continued volume growth in this segment, led by bacon, turkey, pizza toppings, and premium prepared proteins.

Hormel expects sales in its International business to gain from branded exports and recovery in China during the latter half of the year. In Retail, sales growth is expected to be driven by bacon and emerging brands. This could be a positive for the third quarter.

The company continues to focus on its strategic priorities which include driving growth for each of its segments, executing its entertaining and snacking vision, and continuing to transform and modernize the business.