Shares of Philip Morris International Inc. (NYSE: PM) were up slightly on Monday. The stock has gained 3% over the past month. The tobacco company is slated to report its first quarter 2023 earnings results on Thursday, April 20, before market open. Here’s a look at what to expect from the earnings report:

Revenue

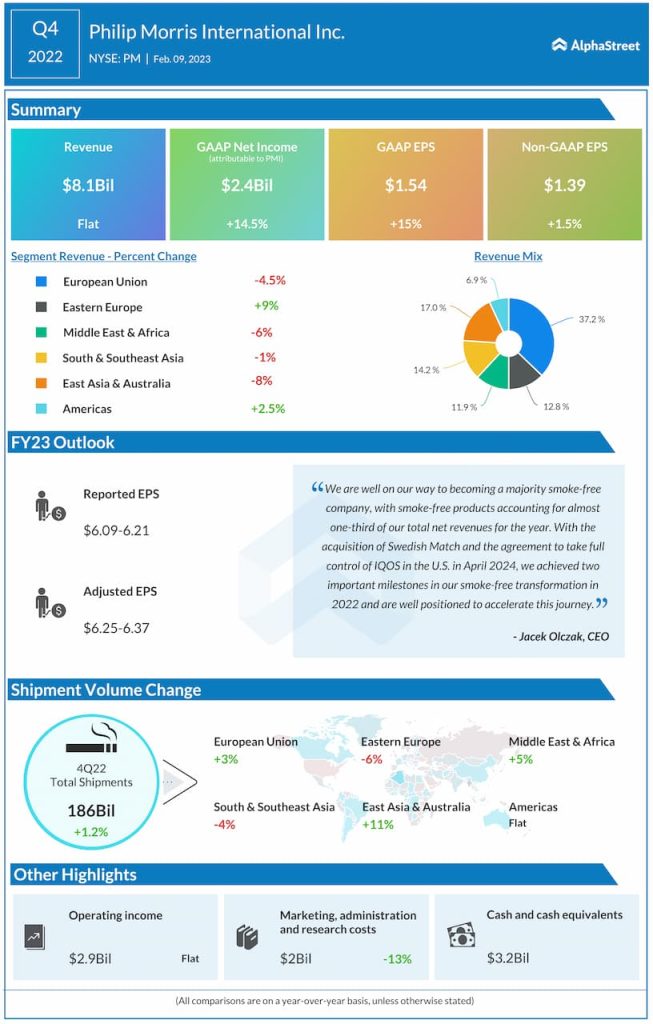

Analysts are projecting revenue of $8.1 billion for the first quarter of 2023, which represents an increase of nearly 5% from the same period a year ago. In the fourth quarter of 2022, the company reported revenue of $8.1 billion.

Earnings

The consensus estimate for EPS in Q1 2023 is $1.35, which compares to pro forma adjusted EPS of $1.46 reported in the year-ago quarter. Adjusted EPS was $1.56 in Q1 2022. In Q4 2022, adjusted EPS was $1.39 and adjusted EPS, excluding currency, was $1.58.

Points to note

Philip Morris’ goal is to become majority smoke-free by 2025 and the company has been making efforts to expand its smoke-free products portfolio. These efforts have been paying off and they are likely to have benefited the company’s performance in the first quarter.

The acquisition of Swedish Match and full control over IQOS are two factors that have the potential to drive significant growth for the company. The addition of the ZYN nicotine pouch brand provides compelling growth prospects in the US for PMI. In the fourth quarter, ZYN saw shipment volumes grow by 35% and it enjoys a strong position in the market.

The momentum of IQOS continues with around 24.9 million users at the end of the fourth quarter. IQOS is seeing gains across the EU, Japan and emerging markets. The IQOS ILUMA is seeing strong growth in its launch markets with upgrades from existing users and the acquisition of new users surpassing expectations.

Philip Morris’ top line performance in the fourth quarter of 2022 benefited from robust combustible pricing and strength in IQOS. This momentum is likely to have continued into the first quarter as well. However, its margins might continue to be impacted by inflationary pressures.