Shares of Tyson Foods, Inc. (NYSE: TSN) stayed green on Friday. The stock has gained 8% over the past three months. The branded foods company is slated to report its second quarter 2024 earnings results on Monday, May 6, before market open. Here’s a look at what to expect from the earnings report:

Revenue

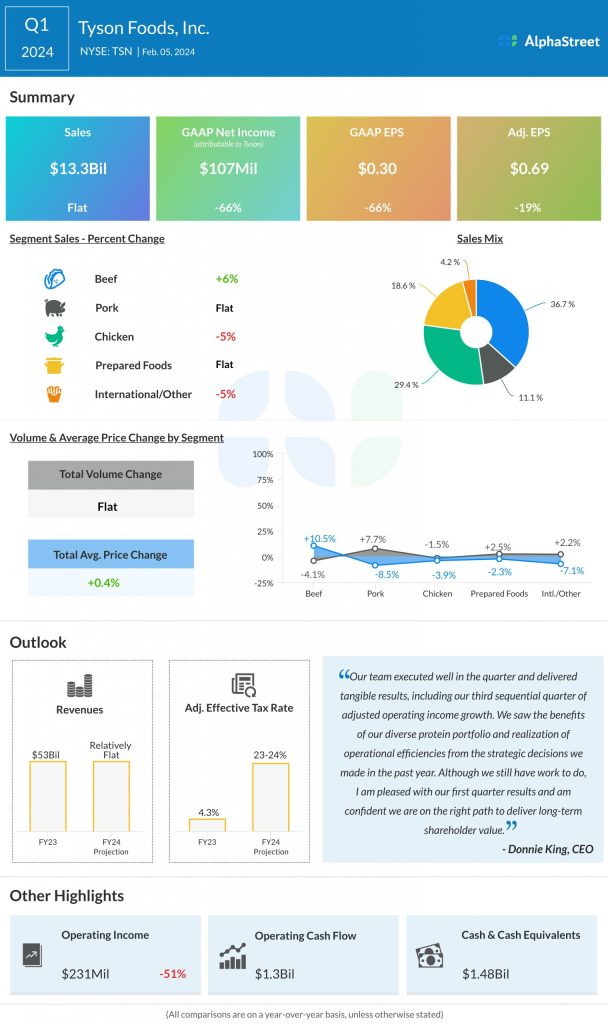

Analysts are projecting revenue of $13.16 billion for Tyson in Q2 2024. This compares to $13.13 billion reported in the same period a year ago. In the first quarter of 2024, sales rose slightly year-over-year to $13.3 billion.

Earnings

The consensus estimate for Q2 2024 EPS is $0.39. This compares to an adjusted loss of $0.04 per share reported in Q2 2023. In Q1 2024, adjusted EPS decreased 19% YoY to $0.69.

Points to note

Tyson can be expected to benefit from its core multi-protein portfolio and its brands, which continue to maintain strong market share. In an inflationary environment, when customers are more discerning in their purchases, they tend to opt for familiar brands. This trend can be expected to work in favor of Tyson. The company is seeing its household penetration rate grow and there appears to be further room for expansion.

On its last earnings call, Tyson said that Q2 is seasonally its weakest quarter for operating income and cash flow, driven by beef and chicken. In addition, the company’s operations were impacted by severe winter weather in January. Start-up costs in the Prepared Foods segment are also expected to impact the second quarter.

Last quarter, sales in the Chicken segment decreased mainly due to lower commodity protein prices. Volumes declined due to lower production. Revenue in the Pork segment dipped slightly as lower pricing offset volume growth. Revenues in Beef increased, helped by higher prices per pound.

In Q1, Prepared Foods benefited from volume growth led by the foodservice business gaining traction. The momentum in foodservice is expected to drive strong volume results for the remainder of the year, which bodes well for the second quarter. This segment is also expected to benefit from capacity additions.