Shares of McCormick & Company, Incorporated (NYSE: MKC) were down 1% on Thursday. The stock has gained 5% year-to-date. The spice giant is slated to report its first quarter 2025 earnings results on Tuesday, March 25, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue

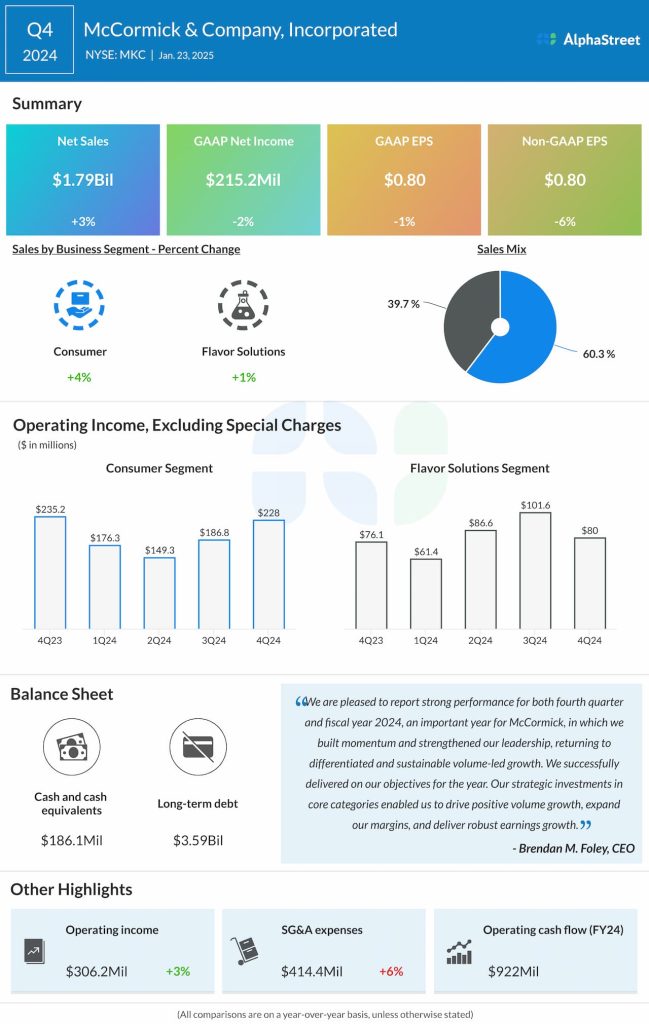

Analysts are projecting revenue of $1.61 billion for McCormick in Q1 2025, which implies a slight increase from $1.60 billion reported in the same quarter a year ago. In the fourth quarter of 2024, sales increased 3% year-over-year to $1.79 billion.

Earnings

The consensus target for Q1 2025 earnings per share is $0.64, which indicates a slight rise from adjusted EPS of $0.63 reported in Q1 2024. In Q4 2024, adjusted EPS fell 6% YoY to $0.80.

Points to note

McCormick can be expected to benefit from the trend of consumers continuing to cook meals at home as they seek healthier options along with maximum value. In an uncertain economic environment, consumers remain budget-conscious but at the same time unwilling to compromise on flavor.

The company has been seeing positive trends across its major markets and core categories. In Q4, volumes in the Consumer segment increased across the Americas and EMEA regions, but volumes in the Asia-Pacific region were impacted by headwinds in China. In Flavor Solutions, volumes were impacted by softness in CPG and QSR customers’ volumes.

MKC has been seeing positive volume and consumption trends in categories such as spices and seasonings, recipe mixes, mustard, and hot sauce. In terms of its products, the company is seeing high demand for larger-sized packets from value-conscious customers, while smaller or trial-sized packets are seeing rising demand from consumers looking to experiment with flavor. This momentum is likely to have continued in the first quarter. The uncertainty with regards to QSR traffic is also likely to persist.

McCormick’s efforts in brand marketing, product innovation, expanding distribution, and managing price gaps are expected to yield benefits, and its cost savings initiatives are expected to help boost margins. In Q4, gross margin expanded by 20 basis points, driven by cost savings from the Comprehensive Continuous Improvement (CCI) program. The company expects gross margin expansion in Q1 to be modest compared to the previous year, due to price gap management investments that have been in place since Q2 2024.