Shares of Philip Morris International Inc. (NYSE: PM) stayed red on Monday. The stock has gained 42% over the past 12 months. The tobacco giant is slated to report its fourth quarter 2024 earnings results on Thursday, February 6, before market open. Here’s a look at what to expect from the earnings report:

Revenue

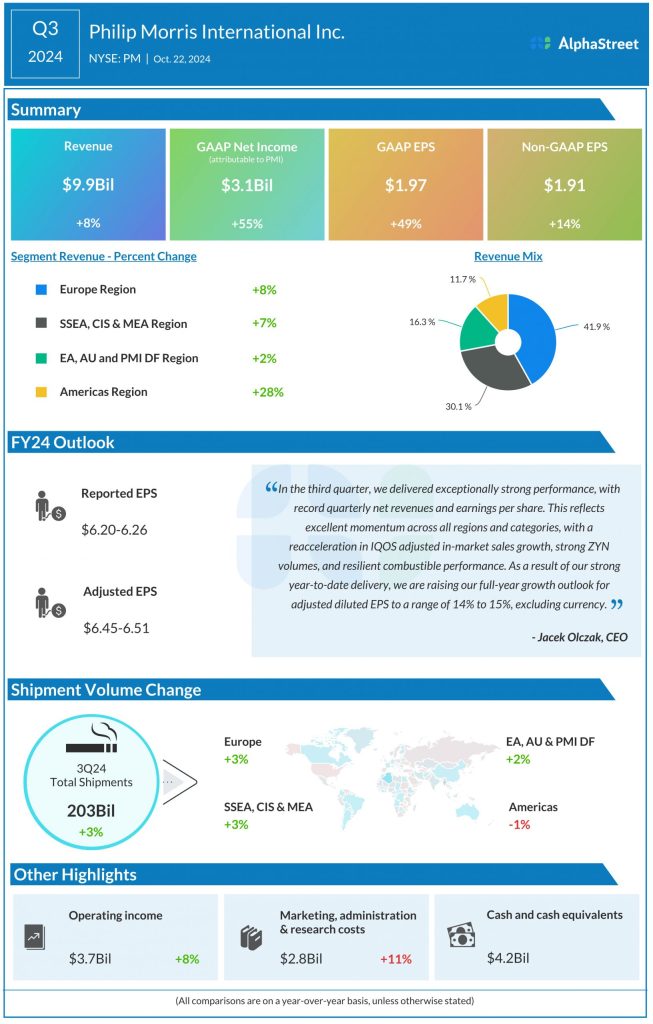

Analysts are projecting revenues of $9.44 billion for Philip Morris in Q4 2024, which represents a growth of over 4% from the same period a year ago. In the third quarter of 2024, revenues increased 8% year-over-year to $9.9 billion.

Earnings

The consensus estimate for earnings per share in Q4 2024 is $1.50, which compares to adjusted EPS of $1.36 reported in Q4 2023. In Q3 2024, adjusted EPS grew 14% YoY to $1.91.

Points to note

Philip Morris continues to see strength in its smoke-free business. In the third quarter, the smoke-free business recorded year-over-year growth of 14% in net revenues and 16% in gross profit, and accounted for 38% of total revenues and 40% of gross profit. In Q3, shipments of smoke-free products reached close to 40 billion units. This momentum is expected to continue in the fourth quarter.

The momentum in the smoke-free business is mainly driven by gains from IQOS and ZYN. IQOS holds a strong position, generating over $10 billion in annual net revenues. In Q3, heated tobacco units (HTU) adjusted in-market sales (IMS) volume grew nearly 15% YoY, supported by double-digit growth in Europe, continued momentum in Japan, and a gain in traction from global markets. This strong growth is expected to continue in Q4.

ZYN nicotine pouches continue to see strong growth. In Q3, oral smoke-free products shipment volume increased over 22%, driven by a 41.4% growth in ZYN shipments in the US. The launch of ZYN in Greece and Czech Republic has expanded its availability to 30 markets. Although the company was facing supply constraints for ZYN, it had anticipated shipments to match consumer demand at some point during the fourth quarter.

The combustibles business is also performing well. In Q3, revenues in this segment increased 5% YoY, helped by high-single-digit pricing and resilient industry volumes. The gain in combustibles was driven mainly by markets where smoke-free products are yet to gain a presence along with the impact of industry efforts on illicit trade in certain markets.

Philip Morris expects to deliver a strong performance in Q4, with margin expansion. It also plans to increase its investments in its smoke-free brands, which are anticipated to lead to a rise in costs.