Retail pharmacy chain Walgreens Boots Alliance, Inc. (NASDAQ: WBA) is on the path to a transformation as it looks to align the core business with new trends in pharmacy operation and become a full-service healthcare provider. The company is experiencing a slowdown now – compared to the pandemic era when sales boomed – mainly due to lower demand for COVID-related services and cautious consumer spending, with the weaker respiratory season adding to the problem.

Investing in WBA

WBA is among the worst-performing Wall Street stocks – the value more than halved in the past one-and-half years. Besides lower demand for COVID-19 vaccines and testing, the poor investor sentiment can also be attributed to the recent exit of then-CEO Rosalind Brewer. On the heels of Brewer’s departure, CFO James Kehoe also left ending his 5-year stint at the company, and more recently chief information officer Hsiao Wang stepped down.

While the valuation looks exceptionally attractive, not many investors would go for WBA because it is a risky bet now. The prolonged losing streak has brought the stock to the lowest level in about 12 years. The consumer segment, which sells products like toothpaste and cosmetics, is also experiencing a sales dip due to competition from cheaper products sold by others like Walmart.

Meanwhile, Walgreens has a turnaround plan in place, which focuses on ramping up its cost-saving program and taking measures to optimize profitability. The management is of the view that there are signs of a return to profitable growth and exudes optimism that its turnaround strategy would deliver long-term shareholder value.

Mixed Q4 in Offing

Experts believe that the company ended the fiscal year on a mixed note. Fourth-quarter profit is estimated to have declined to $0.69 per share from $0.80 per share last year. The sales estimate is $34.82 billion for the August quarter, which is down 7.3% year-over-year. The report is slated for release on October 12, at 7:00 am ET.

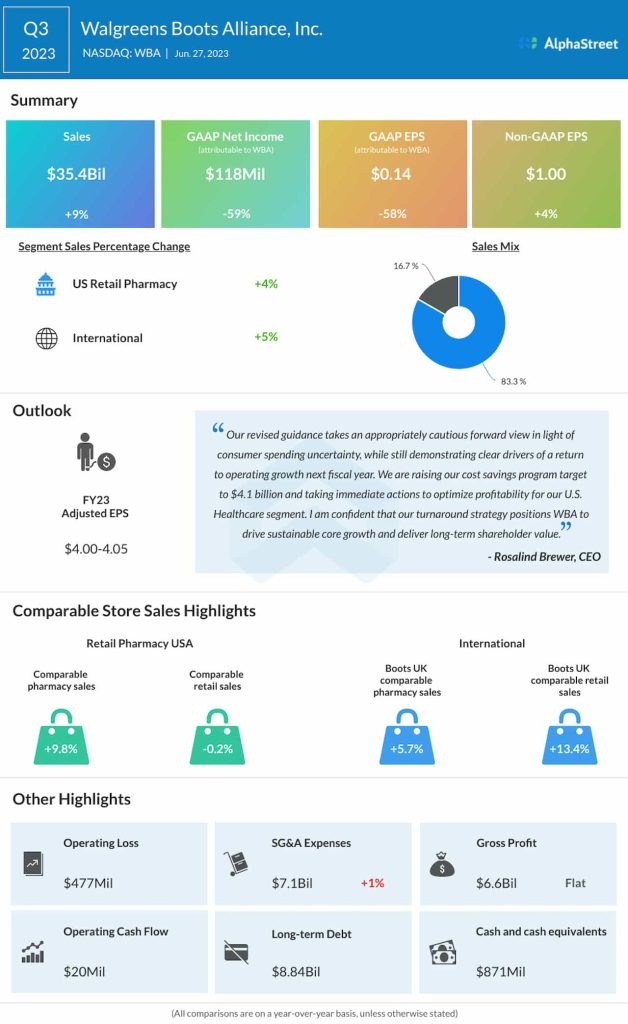

From Walgreens’ Q3 2023 earnings call:

“While we achieved good sales growth and returned to adjusted earnings growth in the quarter, several dynamics created margin pressures that we are factoring into our full-year outlook. We have seen changing market trends that have consumers prioritizing value in response to a more uncertain and challenging economic environment. There has been a steeper drop off in COVID-19 vaccines and testing with the end of the public health emergency. We are also experiencing a slower profit ramp for U.S. Healthcare.”

Earnings Miss

While presenting May-quarter results, Walgreens’ leadership said it was slashing full-year adjusted earnings guidance to the range of $4.00 per share to 4.05 per share, to reflect “consumer and category conditions, lower COVID-19 contribution, and the cautious macroeconomic outlook.” Muted consumer confidence and the reduction in discretionary spending will remain a drag on profitability.

Adjusted profit rose to $1.00 per share in the third quarter from $0.96 per share a year earlier. But the bottom line missed estimates, after beating consistently in every quarter for around three years. The growth reflects a 9% rise in net sales to $35.4 billion. Comparable pharmacy sales were up 9.8%.

Walgreens’ shares traded down 2% on Wednesday afternoon and stayed well below its 52-week average. The market’s cautious outlook indicates the downturn might continue in the near future.