Real estate investment trust companies, which were considered to be the safest for investment, have been shattered since March of this year. Hotels and resorts have been mostly closed with the authorities issuing stay-at-home orders across the US . With many of the hotels and resorts are still closed, it is unknown when these companies would bounce back from their downtime. Let’s look at what the future holds for hotel REIT Park Hotels & Resorts (NYSE: PK).

Q1 results

Park Hotels & Resorts, which spun off from its parent Hilton in 2017, reported its first quarter 2020 earnings results on May 11, 2020. Revenue per Available Room (RevPAR), which is the key indicator of the company’s performance, decreased 23% from the first quarter of 2019. Adjusted FFO per share plunged 64% year-over-year to $0.24. COVID-19 resulted in decreases of 26% and 24% in group and transient segment revenues, respectively.

Portfolio

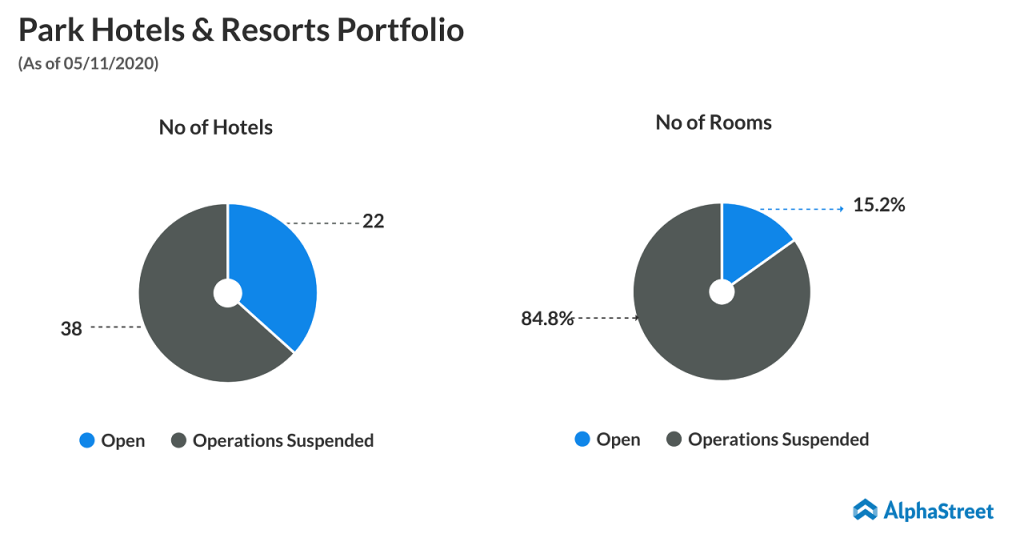

As of May 11, 2020, Park’s portfolio consists of 60 premium-branded hotels and resorts with over 33,000 rooms, primarily located in prime United States markets with high barriers to entry. The company operates many properties at a significantly reduced capacity with consolidated towers and closed floors. As of May 11, only about 15% of its rooms are available to guests.

The majority of the hotels that remained open are either airport or suburban properties that are housing airline crews or special circumstance groups.

Outlook

The situation

remains very fluid. The vast majority of international flights have been

canceled and domestic air travel has also slowed significantly. The hotel REIT expects

leisure travel to be the first segment to generate the highest demand. This will

be followed by business travel.

In general,

Park expects a different operating model overall for its hotels when the travel

resumes. The company has to think about the various components that need

to be re-imagined to accommodate social distancing such as food and beverage

outlets or meetings and banquet programs and they need to focus on guest and

employee safety and cleanliness.

Given the devastation

that occurred and being at the epicenter of the COVID-19 in the US, the company

expects that hotels in New York would be among the last in the company’s portfolio

to reopen. Park expects the demand will be tougher to figure out in

certain markets and the reopening would be delayed there.

Response to

COVID-19

Park has shifted its priorities and actions

to focus on operational and corporate cost reductions. The second largest

publicly traded REIT suspended its operations at 38 out of 60 hotels and

reduced capacity at open hotels. The company had canceled or deferred about 75%

of its planned $200 million CapEx program for 2020. It also suspended dividends

until further announcement.

Park drew $350 million on March 16 and then drew the remaining $650M of capacity on March 25. In May, Park issued $650 million of senior secured notes. A portion of the proceeds ($389 million) was used to pay down the credit facility and its term loan due 2021. CEO Tom Baltimore waived his salary for the remainder of 2020.

Cash burn

Along with its operating partners, Park

developed projected hotel working capital needs assuming suspensions for all

hotels, resulting in an average aggregate hotel funding burn rate of

approximately $50 million per month across the portfolio.

Based on $1.8 billion of liquidity and

assuming a conservative total burn rate of roughly $73 million per month, Park

currently has approximately 25 months of liquidity under extreme conditions.

Long-term view

When asked about the demand recovery, CEO

Tom Baltimore stated in first quarter earnings call,

“You’re seeing the reopening process, it’s going to be uneven, it’s going to be choppy. But I do think that we could get back to ’19 levels. Wouldn’t surprise me if we were back in ’22. I know some push it out to ’23, ’24, ’25. We are not believers of that. We think that it will wrap up soon.”

Now, Park is more focused on the balance sheet, cash preservation and rightsizing the operating model. The company, which completed the $2.5 billion acquisition of Chesapeake in September 2019, said that it will not focus on buying the available small portfolios in the current situation. Park has worked to strengthen its finances with a focus on liquidity. But now the company requires reliable revenue. However, with the current uncertain situation, it increasingly looks like that won’t be happening in the near future.