Give us a quick overview of the business.

Whitestone is a publicly-traded REIT, trading on New York Stock Exchange. We launched it in 2006 from a small shell of assets of about $150 million. We did our IPO in 2010 and now in 2021, we are $1.5 billion in real estate and we’re in several of the best markets in the country including Houston, Dallas-Fort Worth, Austin, San Antoni, Scottsdale, and Gilbert. We basically handcrafted this portfolio to all these retail community centers.

We picked Arizona and Texas because they are business-friendly, and we picked the fastest-growing cities. What we do is, we provide services to the local neighborhoods or the consumers. That service could be a restaurant, a hair salon, or a cigar lounge, or a wine pub. They’re all the kinds of things that you couldn’t get on the internet. That’s basically what the company looks like.

You claim to be an e-commerce resistant concept. Can you just elaborate a bit on that?

Back in 2008, when we were deciding what we wanted to be, we began to see how Amazon was taking over the internet. And basically, that delivery system changed the retail hard-and-soft good marketplace. We saw that happening very early on. And so the big boxes that were very popular on Wall Street, were no longer popular. In fact, the devastation that happened in the retail industry carried over into retail real estate.

So, rather than trying to make our model adjust to the internet, we designed a model around smaller spaces. Great properties tucked into neighborhoods, with businesses that didn’t have to rely on the internet to sell their services. So in that way, we’re internet resistant. And our track record shows that. Our earnings and compound annual growth rates have been great.

At your properties, do you see footfalls returning to what was pre-pandemic?

In terms of our properties, we’ve had better growth than in the pre-pandemic, because you’re dealing with a different type of tenant. In other words, if a family member owns a restaurant, you’re going to see them there from 7 in the morning till 11 o’clock at night. You don’t see the manager of a national chain.

What you have is someone who works harder for that American dream and we’re seeing them even working harder than they did before to accomplish their success. That’s one of the things we see. Another thing we see is that the restaurants have cleverly figured out, because of the pandemic, that a lot of people like their carry-out services.

I think it’s getting better and better. And I think it’s helped us do a lot of things where it’s compressed in a time frame that we wouldn’t have done as quickly previously. For example, artificial intelligence. We have a great database of our artificial intelligence. And we use that to determine the traffic patterns — not only in and out of our centers — but in and out of specific properties. So we’ve seen the traffic to our centers go up in the mid-teens.

ALSO READ Trxade CEO Suren Ajjarapu: Will see the impact of GPO program by Q3 next year

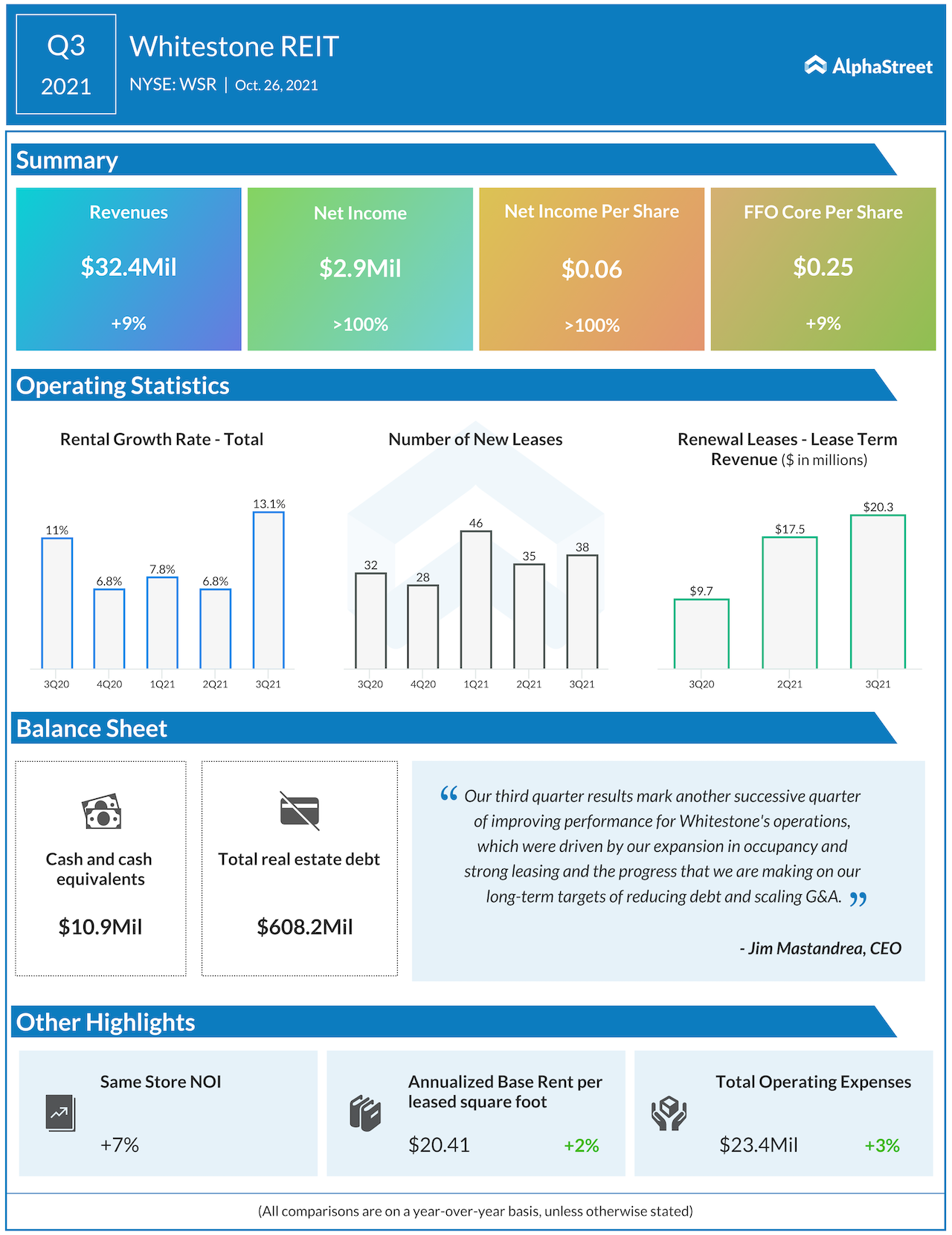

Last week you reported your Q3 results, where same-store non-operating income increased 7%. What factors drove this growth?

What drives the same-store increase is part of the secret sauce in our model, is that we keep our leases short term, relatively three to five years. In the retail industry that sounds pretty short. But if you compare it to the apartment industry, it’s long. We include in that, in our terms, 2-3% increase for inflation. We have the tenant pay the common area maintenance, the taxes, and insurance, and that’s passed through them as well. It really is a dynamic that helps us show same-store increases.

After last year’s dividend cut, do you intend to raise the dividends or will you opt for a more cautious approach in spending?

We look at it every quarter. The question is when do we want to raise it. We have plenty of cash flow to do that. We reduced the dividend because we didn’t know how long the pandemic would last. And when we did that, our cash flow stayed very strong, and we began to use the extra cash to pay down our line of credit.

Our line of credit has been reduced, and our EBITDA-to-debt is improving really well. So there’s a target we have, and when we hit that target, we’ll look at freeing up some more funds to consider increasing the dividend.

ALSO READ Kin Insurance CEO Sean Harper: Will expand into new states, enhance portfolio

What can investors expect from Whitestone over the next two years?

I look at where we’re trading today and one of the reasons we’re trading at that level is because we’ve had a contrarian business model. And the market hasn’t really understood our business. In other words, small space, short-term leases, internet resistance. I think you’ll see it catch on significantly by the end of the year, maybe early next year.

___

For more insights into Whitestone REIT, read the latest earnings call transcript.