The market mayhem could not have come at a worse time for Bed Bath & Beyond Inc. (NASDAQ: BBBY). For long, the home furnishing retailer has been struggling, with a lack of innovation and the obsolete business model weighing on sales and market share. Mark Tritton, the retail veteran who took the helm as the company’s CEO last year, faces the tough task of putting the house in order.

[irp posts=”65444″]

After effecting a major executive reshuffle under its transformation plan, currently, the management’s focus is on preserving liquidity by cutting operating expenses and discretionary spending. The company withdrew its debt reduction initiatives and the decision to return up to $600 million to shareholders this year, besides scrapping major capital spending plans including those related to store remodeling.

Bearish Outlook

The near-term outlook for the retailer does not look very optimistic as several orders were canceled due to store closures, which left the majority of the outlets non-operational during the latter part of the May-quarter including the buy-buy BABY and Harmon Face Values stores. It needs to be seen whether the ongoing efforts to curb cash burn, which resulted in a $1.4-billion cash balance, would help the company stay afloat in the post-COVID market.

“In the last few months, despite the crisis, we’ve continued to accelerate and make strong progress into our strategy, delivering significant growth in digital while our stores remained closed. We have maintained a strong liquidity position, including recent initiatives around cash preservation and the new ABL facility, and believe we can continue to manage for these uncertain times.”

Mark Tritton, chief executive officer of Bed Bath & Beyond

Statistics show that Bed Bath & Beyond has been trailing its peers and the sector in terms of store performance and digital capabilities. The existing store capacity is not sufficient to tap the market opportunity, which calls for efforts to try different store formats so that profitability and market share do not get affected. For the company, the key to turning around the business is to adapt to consumers’ changing shopping habits and ensure balanced inventory levels. Going forward, the move to invest more in the online capabilities should ease the pressure on margins.

Supply Chain Redesign

With the aim of giving the ailing business a fillip, the management has laid a roadmap to redesign the global supply chain. The immediate goal is to reduce working capital requirements, enhance overseas procurement, and optimize network routing. The initiative is expected to help grow in-house brands and boost omnichannel capabilities. Meanwhile, several product launches are lined up for next year across multiple categories.

While plans are afoot to reopen the remaining stores in the current quarter, the main priority is to strengthen the e-commerce platform and also to ensure improvement in customer’s omnichannel experience by re-routing products from stores to web warehouses and converting stores into regional fulfillment centers. Digital sales surged 82% in the most recent quarter.

Posts Q1 Loss

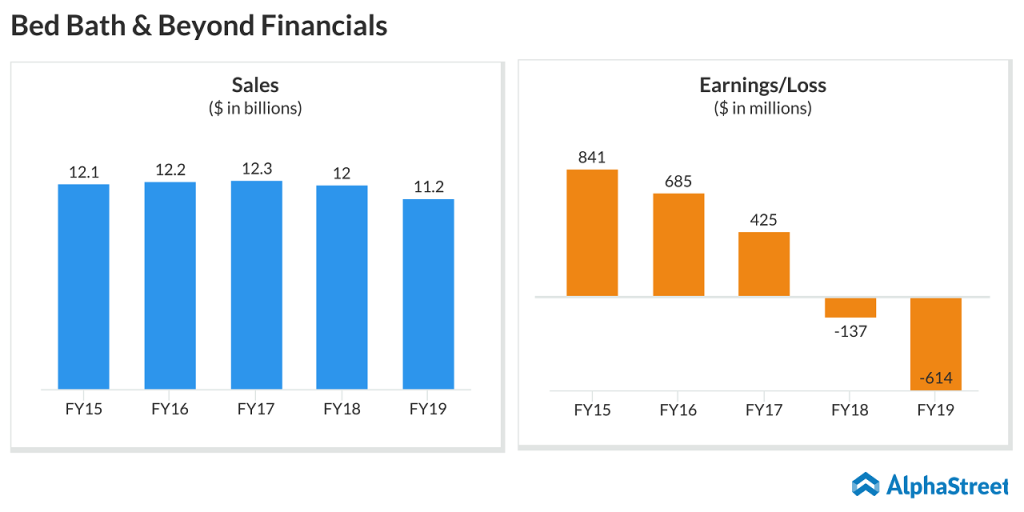

The company slipped to a loss of $1.96 per share in the first quarter of 2020 when sales plunged about 50% as customers stayed away from stores due to the shelter-in-place orders. It was worse than the downturn analysts had forecast and that prompted the management to announce the closure of around 200 stores in the next two years, under its fleet optimization strategy. Initial estimates show that comparable sales per store dropped in low-single digits on average during June, with the second half of the month witnessing a modest pickup.

“As part of our store network optimization project, we plan to close approximately 200 stores over the next two years, representing about 21% of our total Bed Bath & Beyond stores, and we’ll continue to focus on other SG&A expense reductions. We believe the aggregate benefits from these actions will generate future annualized savings of between $250 million and $350 million,” said Gustavo Arnal, the company’s chief financial officer.

[irp posts=”61912″]

In early April, shares of Bed Bath & Beyond slipped to the lowest level in more than 25 years and traded below $10 in the weeks that followed. They suffered a fresh jolt after this week’s earnings report and reversed the modest recovery seen ahead of the announcement. The stock been on a losing streak for the past several years, all along underperforming the market.