Last year, Nvidia Corporation (NASDAQ: NVDA) solidified its leadership in high-performance AI compute, supported by the wide adoption of its GPUs and AI accelerators across cloud data centers, research institutions, and enterprise applications. The company has also built a robust ecosystem around its CUDA software and networking platforms, strengthening its competitive moat. With AI training and inference workloads expanding rapidly, Nvidia is positioned to capture outsized demand growth in the quarters ahead.

Bullish Outlook

The tech firm will report its fourth-quarter fiscal 2026 earnings on Wednesday, February 25, at 4:20 pm ET. On average, Wall Street analysts project a 71.3% surge in fourth-quarter revenues to $65.62 billion. The outlook also reflects an estimated 71% growth in fourth-quarter adjusted earnings to $1.52 per share. Nvidia has consistently beaten quarterly estimates since 2023.

Nvidia’s stock delivered a strong performance in 2025, maintaining momentum after a modest start. Shares have more than doubled over the past twelve months. After pulling back from the all-time highs of October 2025, the stock has consistently traded above its 52-week average of $160.25. Analysts view the recent dip as a buying opportunity and generally recommend NVDA this week.

ALSO READ: Nvidia Q3 2026 revenue & earnings beat estimates

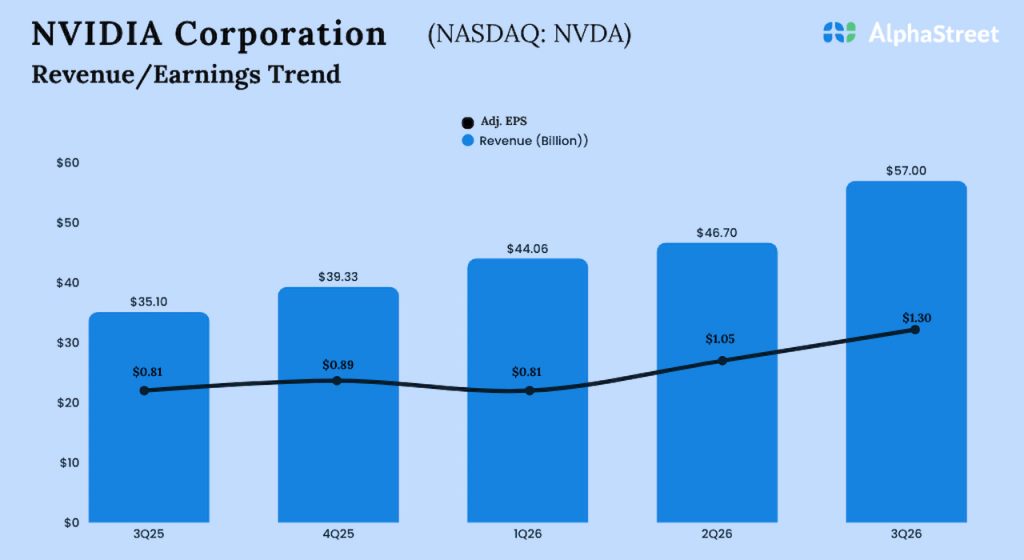

Record Revenue

In the third quarter of FY26, Nvidia’s revenue increased sharply to $57.0 billion from $35.08 billion in the prior year, boosted by a 66% surge in Data Center revenues. The top-line exceeded analysts’ expectations. On an adjusted basis, third-quarter earnings climbed to $1.30 per share from $0.81 per share a year earlier, beating estimates. On a reported basis, net income was $31.9 billion or $1.30 per share in Q3, compared to $19.3 billion or $0.78 per share in the year-ago quarter.

From Nvidia’s Q3 2026 Earnings Call:

“We have evolved over the past 25 years from a Gaming GPU company to now an AI Data Center Infrastructure company. Our ability to innovate across the CPU, the GPU, networking, and software, and ultimately drive down cost per token, is unmatched across the industry. Our networking business, purpose-built for AI and now the largest in the world, generated revenue of $8.2 billion, up 162% year-over-year, with NVLink, InfiniBand, and Spectrum-X Ethernet all contributing to growth. We are winning in Data Center Networking as the majority of AI deployments now include our switches with Ethernet GPU attach rates roughly on par with InfiniBand.”

Pivotal Year

Nvidia is at the intersection of rapidly expanding AI workloads and demand for high-performance compute. With its platforms deeply embedded across cloud providers, enterprise deployments, and research infrastructures, the company remains a bellwether for broader trends in AI hardware and software adoption. As competition intensifies and new architectures emerge, Nvidia’s ability to innovate and support evolving customer needs will be a key factor in how it navigates the opportunities and challenges this year.

Reversing the recent downtrend, Nvidia’s shares traded higher mostly during Tuesday’s regular session. The shares have declined 1.2% since the beginning of 2026.