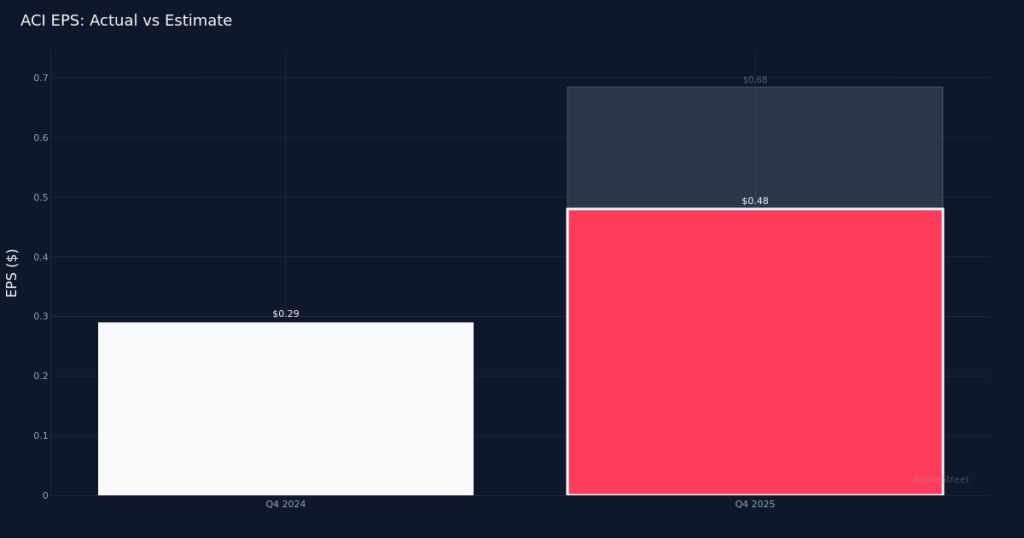

Disappointing Miss. Albertsons Companies, Inc. (NYSE:ACI) stumbled in Q4 2025, delivering adjusted earnings per share of $0.48 versus the Street’s $0.68 expectation—a significant 29.4% shortfall that sent shares down 3.2% to $16.31. Revenue of $20.25B reflected a solid 7.7% increase from the $18.80B recorded in Q4 2024, yet the substantial earnings miss signals margin compression challenges that overshadowed top-line momentum. Adjusted net income reached $251.7M for the quarter, but the divergence between revenue growth and bottom-line performance raises questions about operational efficiency and cost management during what should have been a strong holiday period for the grocery retailer.

Soft Comparables. Identical sales growth of just 0.7% for the quarter reveals a more troubling underlying story—much of the revenue expansion appears driven by the company’s expanding footprint across 2,244 total retail stores rather than organic strength within existing locations. This tepid comparable performance in an inflationary environment where food prices have generally elevated suggests Albertsons may be losing wallet share to discount competitors or facing traffic headwinds. The weak same-store metric explains why revenue growth failed to translate into earnings leverage, as new store economics typically carry higher operating costs that pressure near-term profitability.

Conservative Outlook. Management’s fiscal 2026 adjusted EPS guidance of $2.22 to $2.32 offers little comfort to investors hoping for a swift recovery. At the midpoint of $2.27, this projection implies modest improvement from what appears to be a challenging baseline, though the company will need to demonstrate better expense control and traffic trends to achieve even these muted targets. The guidance range suggests management remains cautious about the consumer environment and competitive dynamics in the grocery sector, where promotional intensity and shifting shopper preferences toward value channels continue to weigh on traditional supermarket operators.

Mixed Sentiment. Wall Street maintains a divided stance on Albertsons with 14 buy ratings, 7 holds, and 2 sells—reflecting uncertainty about the company’s ability to navigate persistent margin pressures while investing in omnichannel capabilities and price competitiveness. The substantial earnings miss and weak identical sales performance may prompt analysts to revisit their models and assumptions, particularly regarding the pace of margin recovery and same-store sales acceleration needed to justify current valuation levels.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.