AlphaStreet Newsdesk powered by AlphaStreet Intelligence

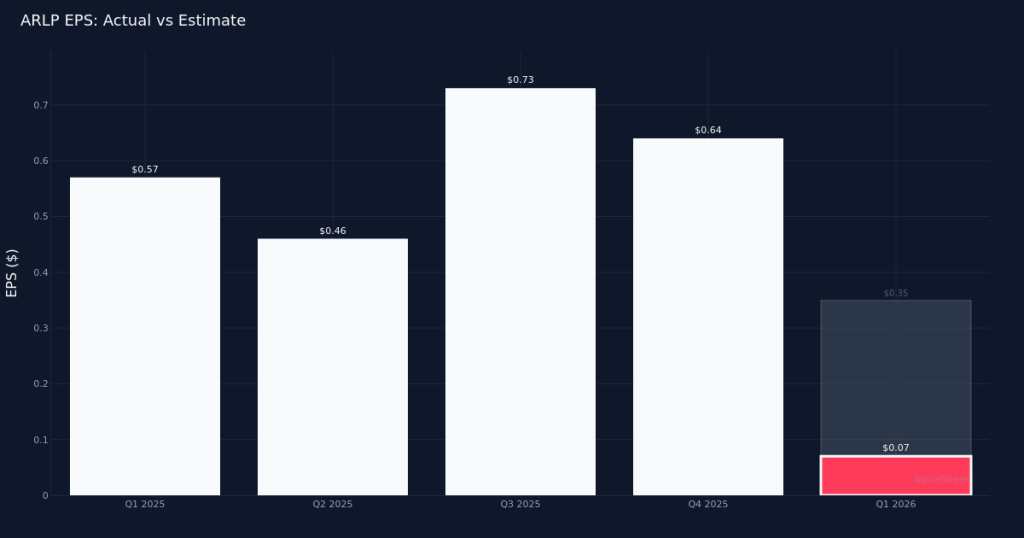

Margin Collapse Overshadows Revenue Stability. Alliance Resource Partners delivered a jarring miss in Q1 2026, reporting GAAP EPS of $0.07 against consensus expectations of $0.35—an 80.0% shortfall. The thermal coal producer’s net income plummeted to $9.1M from $79.3M in the year-ago quarter, an 87.7% decline that dwarfs the relatively modest 4.5% revenue contraction to $516.0M. This disconnect between topline resilience and bottom-line deterioration signals fundamental margin compression rather than a demand-driven revenue crisis, pointing to cost structure challenges that management must address with urgency.

Profitability Erosion Reveals Operational Stress. The quality of Alliance’s earnings deteriorated sharply, with net margin collapsing from 13.7% in Q1 2025 to just 1.8% in the current quarter—a 12.9 percentage point contraction that represents the story’s central concern. Management acknowledged this reality directly: “Net income attributable to ARLP in the 2026 quarter was $9.1 million or $0.07 per unit as compared to $74 million or $0.57 per unit in the 2025 quarter.” This isn’t a business maintaining profitability while revenues decline; this is a company barely breaking even despite generating half a billion in quarterly sales. The EBITDA figure of $105.6M provides some reassurance that operating cash generation remains intact at $105.5M, but the translation from operating earnings to net income shows severe degradation. Free cash flow of $13.3M, while positive, represents a concerning 76.7% decline from the cash generation implied by last year’s profitability levels.

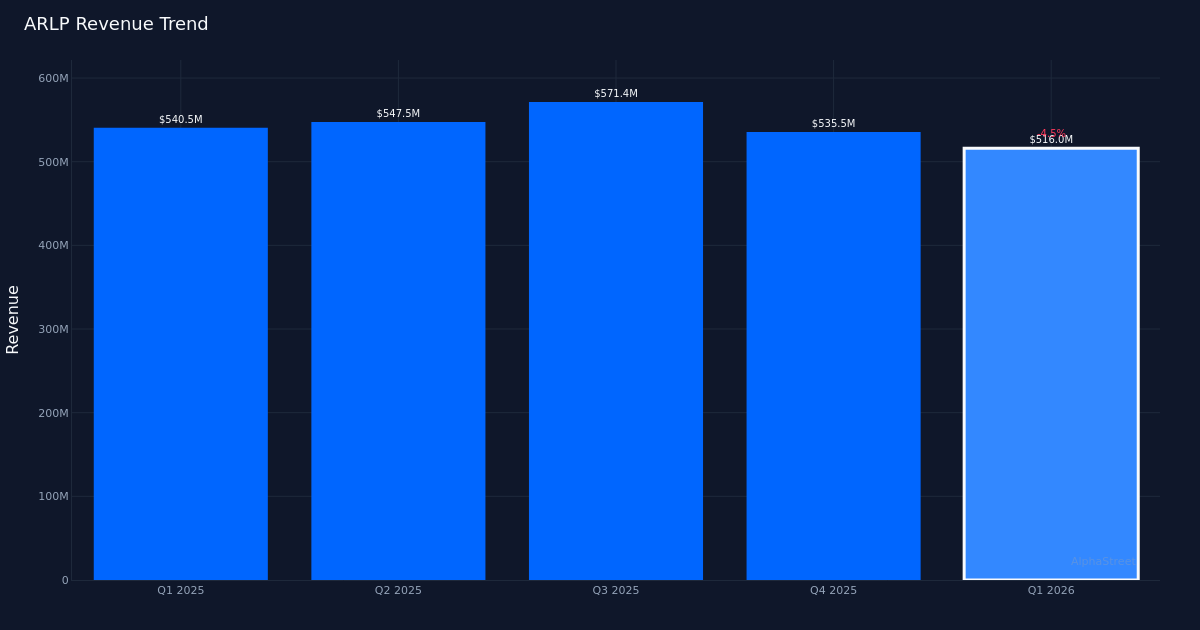

Sequential Deterioration Compounds Year-Over-Year Weakness. The four-quarter trend reveals an alarming trajectory: EPS has plunged from $0.73 in Q3 2025 to $0.64 in Q4 2025 and now $0.07 in Q1 2026, while revenue declined from $571.4M to $535.5M and now $516.0M. This represents both sequential and year-over-year pressure, eliminating any argument that Q1 represents a seasonal anomaly. Management noted that revenues were “down 3.6% compared to the sequential quarter,” confirming the downward momentum. The consistency of this decline across three consecutive quarters suggests structural headwinds rather than temporary disruptions. Net income followed an even steeper path: $95.1M in Q3 2025, $82.7M in Q4 2025, then the collapse to $9.1M this quarter—a pattern that indicates margin compression accelerated dramatically in the most recent period.

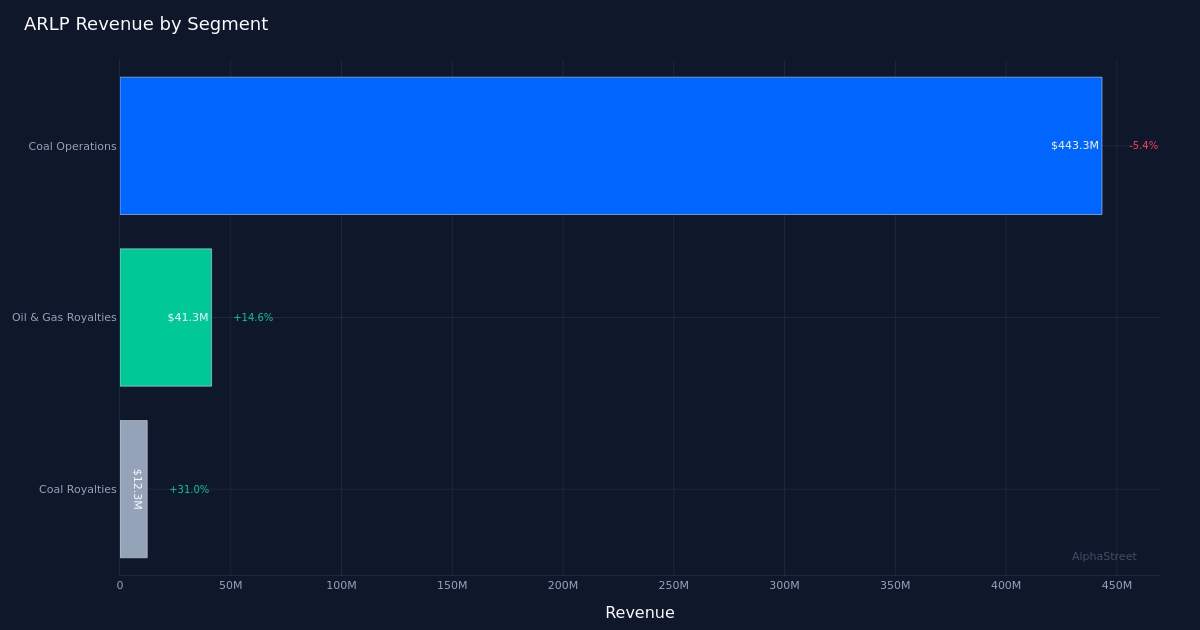

Segment Mix Provides Limited Offset. The segment breakdown reveals that Coal Operations, the company’s core business at $443.3M in revenue, declined 5.4% year-over-year and continues to face pricing pressure. Management disclosed that “our average coal sales price per ton for the 2026 quarter was $56.40, a 6.5% decrease versus the 2025 quarter and a 2% decrease sequentially,” directly explaining the revenue and margin pressure in this segment. The twin headwinds of volume and price create a challenging environment for the thermal coal business. More encouragingly, Oil & Gas Royalties grew 14.6% to $41.3M, while Coal Royalties surged 31.0% to $12.3M, demonstrating that Alliance’s diversification efforts are gaining traction. However, these higher-margin royalty streams remain too small at approximately 10% of total revenue to offset the operational challenges in the core coal business. Total coal inventory of 1,200,000 tons suggests adequate supply positioning but raises questions about demand absorption rates given the pricing deterioration.

Execution Against Historical Standards Deteriorates. Alliance’s track record shows a company that beat earnings expectations 0 of the last 1 quarters—a 0% beat rate that, while limited in sample size, reflects the current quarter’s significant miss. More concerning is the magnitude: missing by 80.0% isn’t a rounding error or slight miscalculation; it represents a fundamental disconnect between what management guided (implicitly, through analyst models) and what the business delivered. An analyst probed this dynamic during the earnings call, noting: “I noticed that the pricing for Appalachia Coal came in above $74, which is above your guidance, and yet guidance remains unchanged.” This suggests management may be maintaining conservative guidance even as certain segments outperform, but the overall results demonstrate that spot outperformance in Appalachia couldn’t overcome broader operational challenges.

Capital Allocation Comments Hint at Strategic Pivots. Management’s discussion of capital deployment provides clues about their strategic response to margin pressure. One executive noted: “Yeah, I think that, you know, as we look at the pipeline, you know, we mentioned that we did 16 million in the first quarter, we did 14 million in the fourth quarter.” While the context of this $16M deployment isn’t fully specified in the data, the sequential increase from $14M to $16M suggests management is maintaining investment discipline even as profitability contracts. This could represent continued investment in the higher-growth royalty segments or essential maintenance capital in coal operations. The free cash flow generation of $13.3M, though diminished, indicates the company retains capacity for modest capital allocation beyond operational requirements.

Muted Stock Reaction Suggests Lowered Expectations. The relatively modest stock decline following an 80.0% earnings miss reveals that market expectations had already adjusted downward. Investors appear to have anticipated significant margin compression, tempering their reaction to results that would typically trigger a more severe sell-off. This muted response suggests either that the market focuses more on cash generation metrics (where EBITDA of $105.6M provides some comfort) or that the stock had already priced in substantial operational challenges. The current price level likely reflects continued uncertainty about whether Q1 represents peak margin pressure or the beginning of a sustained downturn in coal economics.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.