With the pandemic defying predictions and affecting more people, there is a natural tendency to keep away from tobacco consumption. But the recent financial performance of Altria Group, Inc. (NYSE: MO), the company behind popular brands like Marlboro, shows the virus impact on the industry is not as severe as expected.

Altria’s positive quarterly performance during the crisis period came as a morale booster for the management, given the anti-tobacco movement that is gaining traction in key markets. However, a part of momentum can be attributed to the shelter-in-place orders that made people stock up on supplies, including tobacco products.

Right Valuation

Some experts see a buying opportunity in Altria’s low valuation and resilience to the COVID-19 crisis. Going by the strong buy rating and impressive target price — representing a 46% gain in the 12-month period — the stock is definitely worth trying. However, it might not be a wise bet from the short-term perspective.

The bad news is that tobacco companies might come under pressure from agencies like the World Health Organization and human rights activists if the threat of COVID-19 persists. That, combined with weakening spending power in the absence of additional government stimulus, could weigh on sales. Ultimately, companies and economies that depend on the industry would be forced to diversify and look for alternatives.

Smokeless Push

It is worth noting that adult smoking rates in the U.S have fallen to low-double-digits in the past few years. Altria’s executives recently claimed to have achieved significant progress in the ambitious ten-year Vision program, aimed at transitioning adult smokers into non-combustible alternatives.

Meanwhile, the company’s revival strategy is focused on shifting to smokeless tobacco products, and less harmful products like wine, while enhancing margins through cost-cutting and hiking prices. The recent acquisition of JUUL was an important step towards strengthening the smokeless segment, though e-cigarette maker needs to clear certain regulatory hurdles before becoming full-fledged.

From Altria’s third-quarter earnings conference call:

“The September 9 deadline for PMTA submissions represented an important milestone in the regulatory process for the e-vapor category. We believe it’s important that e-vapor remains an alternative for smokers and believe that a sustainable e-vapor category will be one that consists solely of FDA-authorized products. We encouraged FDA enforcement against non-compliant manufacturers including those who continue to sell e-vapor products without a PMTA submission.”

Earnings Beat

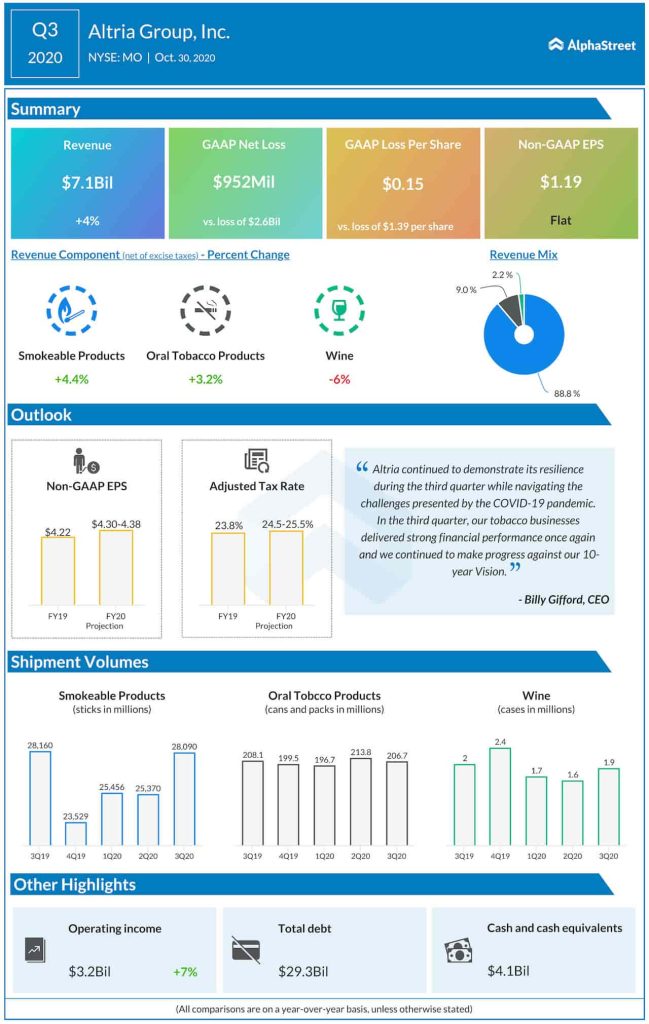

Smokeable products, the core segment that accounts for nearly 90% of the total business, performed well during the third-quarter when total revenues rose 4% to about $7 billion. While the bottom-line was impacted by one-off costs, adjusted earnings matched the prior-year number of $1.09 per share and topped the Street view.

Read management/analysts’ comments on quarterly results

“At retail, we estimate the number of tobacco consumer trips to the store rebounded in the third quarter and that tobacco expenditures per trip remained elevated versus the year-ago period. We also continue to believe that consumer stay-at-home practices allow for more tobacco usage occasions in the quarter. The smokeable products segment delivered strong financial and marketplace results in the quarter,” said Altria’s chief executive officer Billy Gifford.

Stock Performance

Shares of the company have been in a downward spiral for quite some time and the weakness intensified this year, especially after coronavirus derailed economic activity. Last week the stock pared a part of the recent losses, following the earnings release, and maintained the momentum since then. It has lost 25% in 2020, after starting the year on a high note.