Following a free fall of air traffic of approximately 95% in the aftermath of COVID-19 crisis, the aviation sector, which directly employs 750,000 people in the US, needed an anchor to survive. This anchor came in the form of CARES – Coronavirus Aid, Relief, and Economic Security Act.

The provision of this act includes direct grants worth $25 billion exclusively for employee payouts like wages, salaries and benefits, along with loans and loan guarantees of about $25 billion for continued operations.

Forbes estimates that approximately 80% of the aggregate grant amount goes out to American Airlines, Southwest, Delta, and United Airlines.

[irp posts=”52714″]

The Act comes with its own sets of restrictions, though. Businesses have to maintain their employment levels (with no more than 10% reduction) until September 30, 2020. The other few include Maintenance of essential scheduled air service, suspension of their share buyback programs and dividend payouts et. all, restrictions on increase in executive payouts, severance and other benefits. One that didn’t fit well with Boeing was – giving a stake to the Government through warrants, equity interest or debt (this is not compulsory for grants, but for loans). This might reduce managerial control over the company.

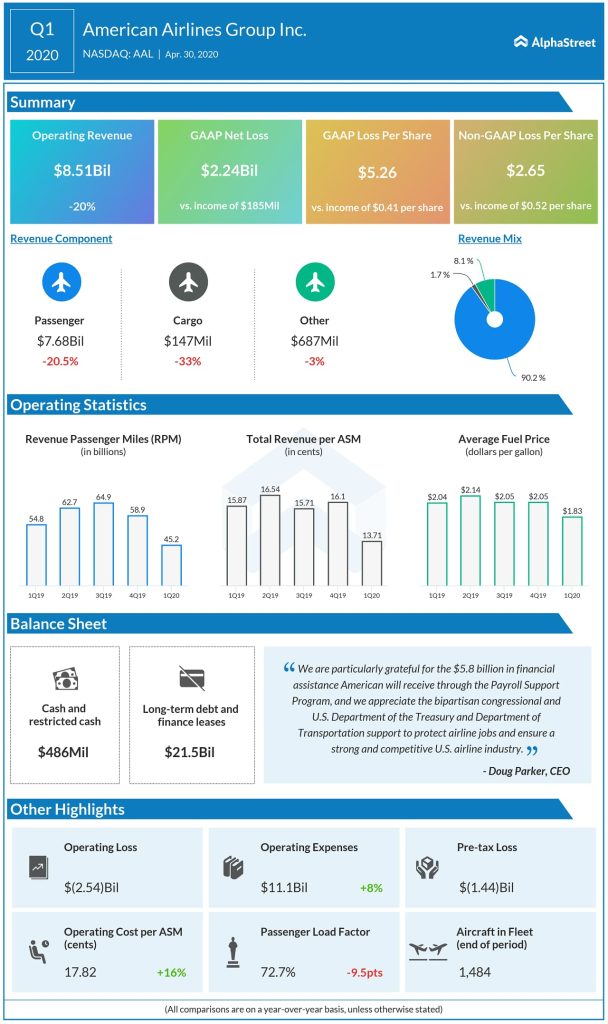

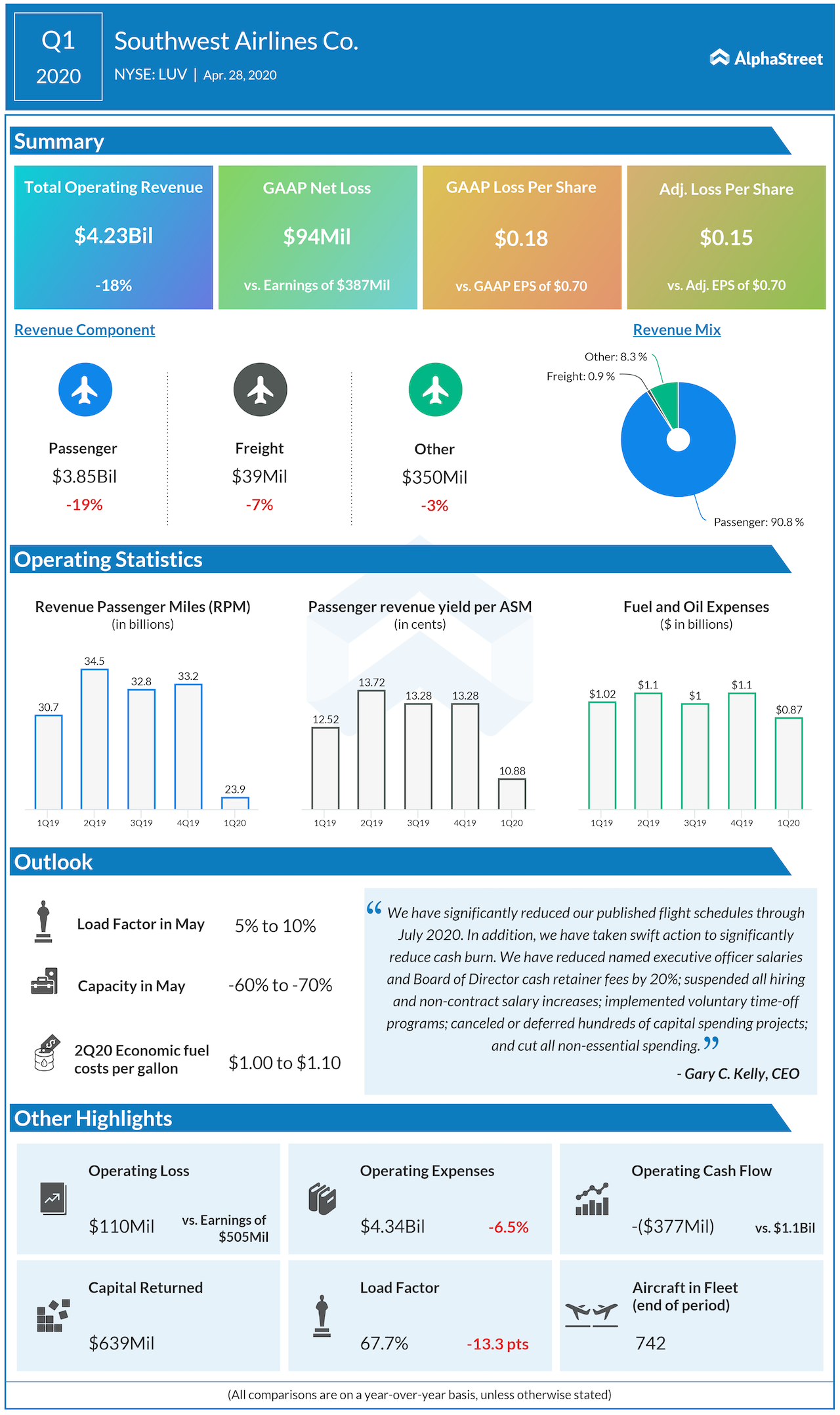

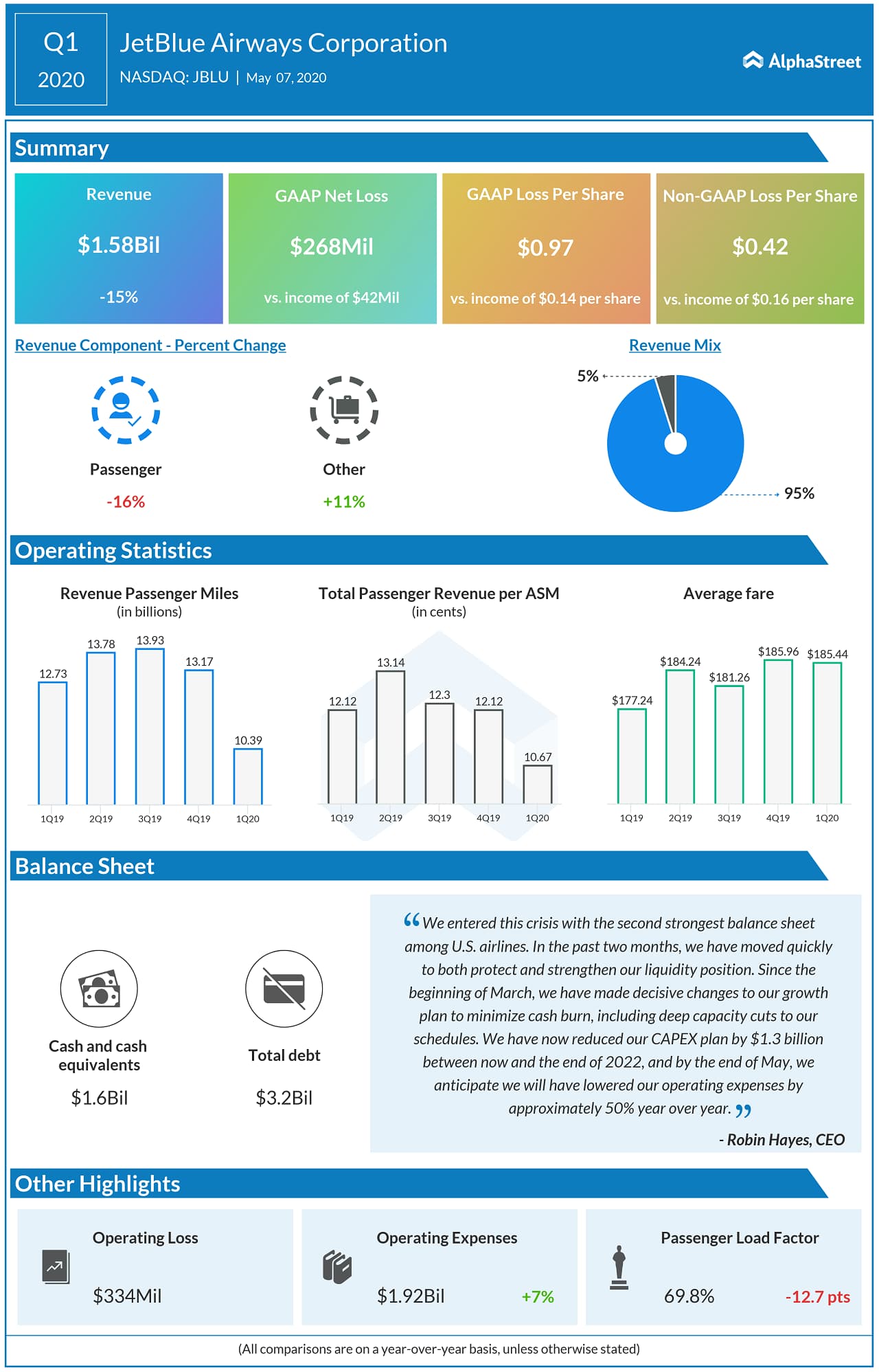

‘CARES’ was mentioned 20 times during the earnings call of American Airlines (NASDAQ: AAL), whereas United (NASDAQ: UAL) mentioned it 7 times, Southwest (NYSE: LUV) a total of 4 times, and in comparison Delta (NYSE: DAL) had 2.

American Airlines, an employer of 130,000 people globally, has been given approval of $5.8billion in assistance from the Treasury through CARES Act. The breakdown has a $4.1 billion direct grant and a LIBOR based loan of $1.7 billion. Additionally, it has applied for a loan of about $4.75 billion.

American Airlines CEO Doug Parker had said in 2016,

“We have gotten to the point where we like other businesses will have good years and bad years, but the bad years will not be cataclysmic. They will just be less good than the good years.”

He retracted from the statement during the conference call, saying “We will emerge from this in the fall with a smaller airline than we had anticipated prior to the virus, of course, and go into 2021 as a smaller airline.”

Currently, the company estimates its daily cash burn rate at $70 million per day, which it expects to bring down to about $50 million by June. This burn rate includes the refunds for their flights (which accounts for estimated at $1.2 – $1.3 billion for the quarter), amortizations, employer payouts, fixed overheads. Comparatively, Delta also plans to bring it down to $50 million by the end of the second quarter and United expects $40-$45 million a day by May.

So, American is focusing on ensuring liquidity and cutting costs by various measures such as retiring fleets early (causing a flurry of reduction in volume-related expenses such as maintenance, inventory, scheduling and training) and deferring marketing.

CARES has a clause that goes along the lines of proving that ‘obligor can’t avail the credit market’ for their requirement, which entails that American Airlines doesn’t have a lot of options to increase their liquidity and afford credit from the market. Given the market risk, and macroeconomic factors the interest rates have increased.

[irp posts=”59756″]

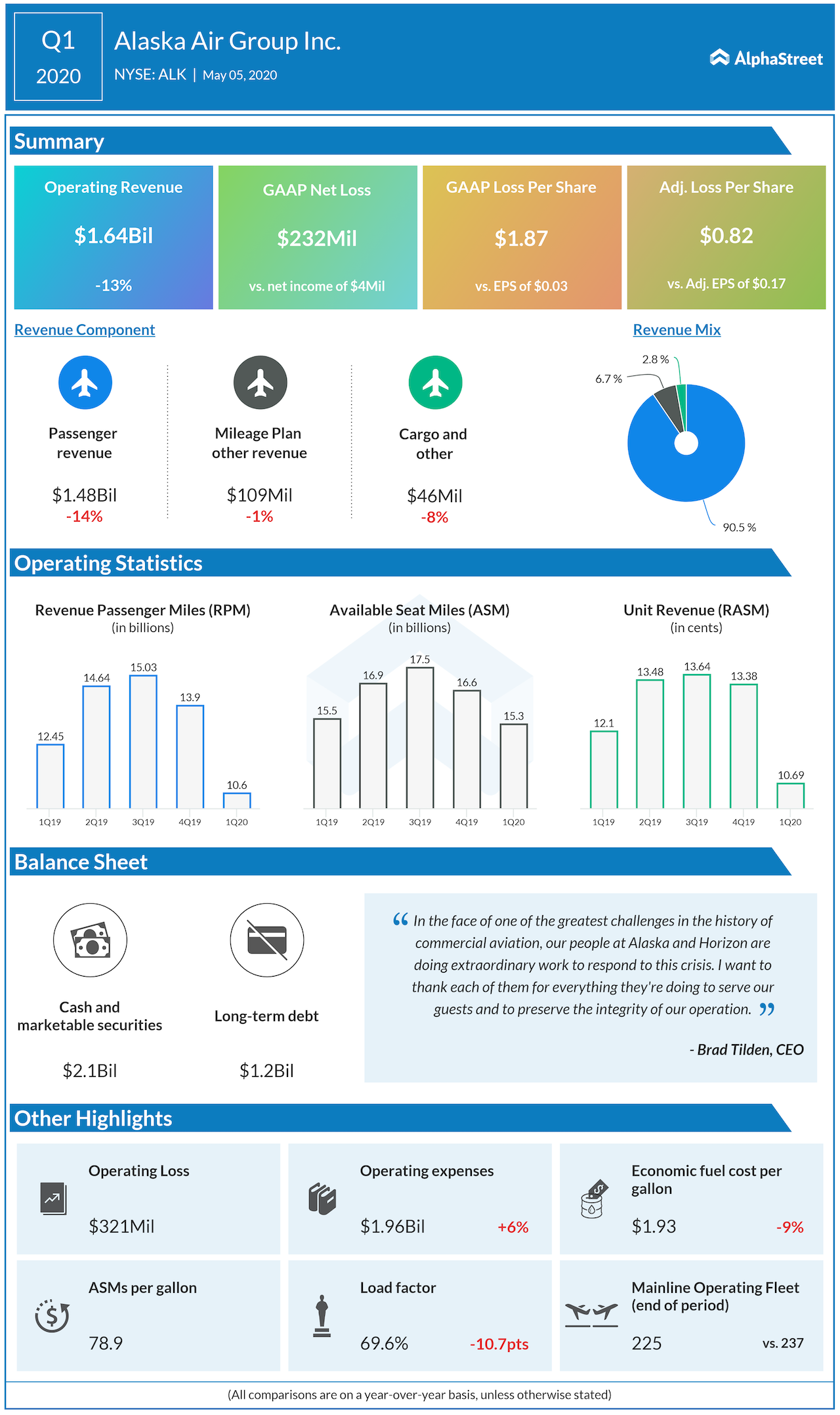

Parker said, “We did an unsecured deal at 3.7….today if we try and do [it]…it’s a double-digit number.” American seems to be a risky company to give capital to. It seems to have one of the highest leverage, entering 2020. It had a total of $33.4 billion of debt and lease liabilities, with only $3.8 billion in unrestricted cash and short term investments to make up for it. United has $23.4 billion in debt, with $5.2 billion in cash, etc.

-

American Airlines -

United Airlines -

Delta Air Lines -

Southwest Airlines -

Alaska Air -

Jetblue

While other airlines were moving towards lowering their debt over the periods of sustained profitability during the past 4-5 years, by using operating cash flows for reinvestment in their businesses, American Airlines was making significant CapEx investments, most of which was paid for by issuing debt and leaseback transactions. American Airlines’ cumulative CapEx as a percentage of Operating Cash Flow comes to a whopping 104%, compared with United at 76%, Delta at 57%, and Southwest at 45%.

The other clause is ‘the intended obligation was prudently incurred,’ which implies a need for good quality collateral. American boasts of its highly valued Advantage Loyalty Program, and assets like international flight routes, airport gates, and other ‘unencumbered’ assets worth $10 billion in aircraft, spare parts, engines, slots and accounts receivables, and real estate.

American Airlines ended Q1 with $6.8 billion liquidity, and as mentioned in their earnings call, it expects to end Q2 with about $11 billion liquidity, wherein it depends on no financing options other than the government’s. A lot is dependent on its ability to generate revenues and additional financing with the available collateral. Other financing options, after Q2, will require American to put more debt on their balance sheet, thus leveraging itself further. Needless to say, the next few months are crucial for the airline industry.

(Written by Shreya Chandra)

[irp posts=”60519″]