American Express Company (NYSE: AXP) is slated to report fourth quarter 2019 earnings results on Friday, January 24, before the market opens. The company is expected to report higher revenues and profits for the quarter.

Analysts estimate earnings of $2.01 per share, which is above earnings of $1.74 per share reported a year earlier. Revenue is expected to grow more than 8% to $11.36 billion.

The topline numbers are likely to benefit from cardmember

spending and revenues from fee-based products. The results might also be helped

by a growth in the small and medium-sized enterprise sector as well as in consumer

spending.

Last quarter, revenue growth was driven by a balanced mix of cardmember spending, loans and membership revenues from fee-based products, which grew 19% and exceeded $1 billion for the first time. The company also added 2.9 million new proprietary card members during the period.

Also read: American Express Q3 2019 Earnings Call Transcript

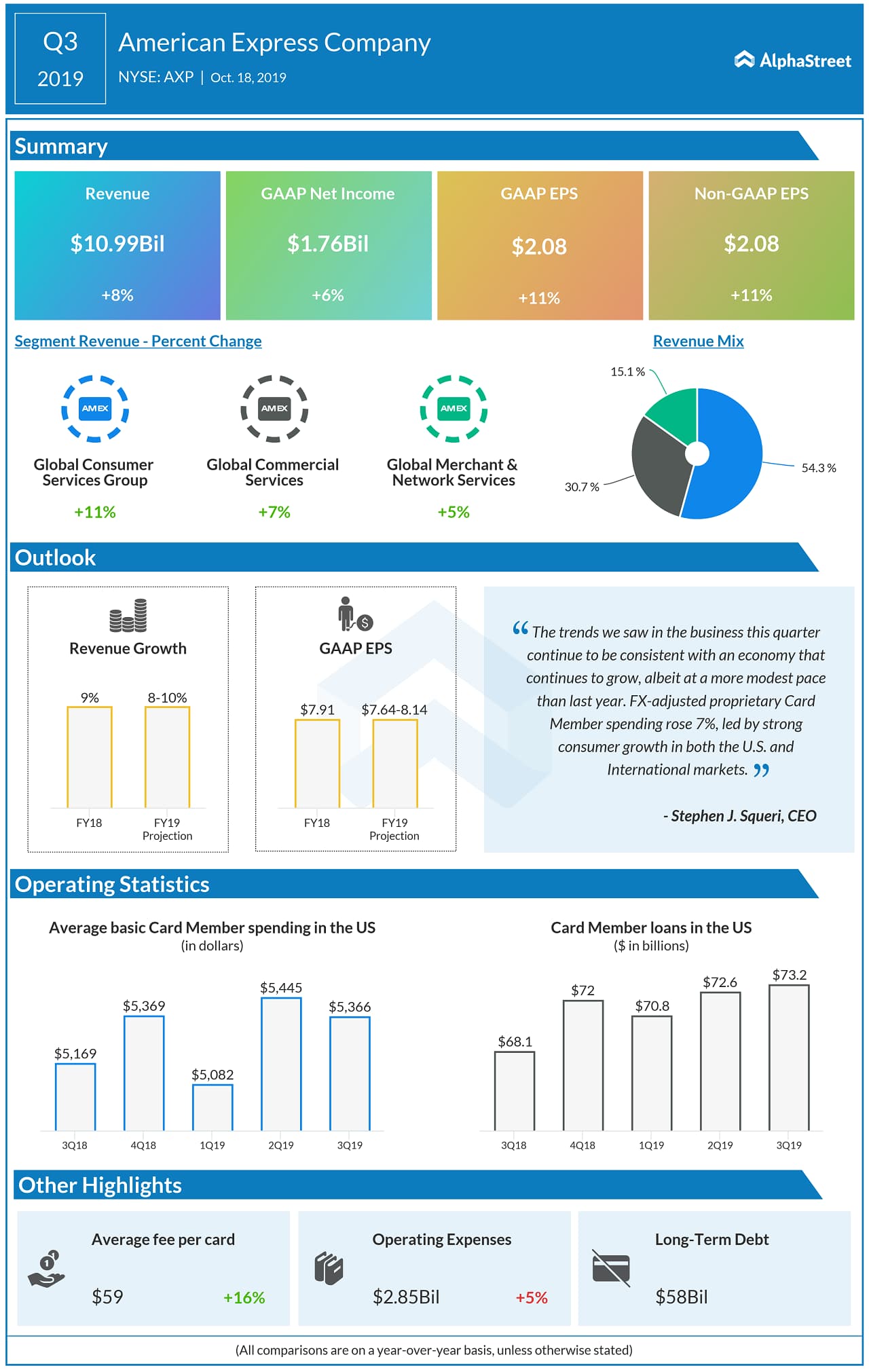

In the third quarter of 2019, American Express topped revenue and earnings estimates, with revenue growing 8% to $10.99 billion and adjusted EPS increasing 11% to $2.08. The company saw revenue growth across all its segments as well.

For the fourth quarter, American Express has guided for revenue growth of 8-10%. For the full year of 2019, the company expects GAAP EPS of $7.64-8.14 and adjusted EPS of $7.85-8.35.

Shares of American Express have gained 31% in the past one year and over 4% in the past one month. The majority of analysts have rated the stock as Buy and it has an average price target of $137.88.