Shares of American Express Company (NYSE: AXP) turned red in afternoon trade on Wednesday. The stock has gained 13% in the past 12 months. The global payments company is set to publish its fourth quarter 2025 earnings results on Friday, January 30, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue

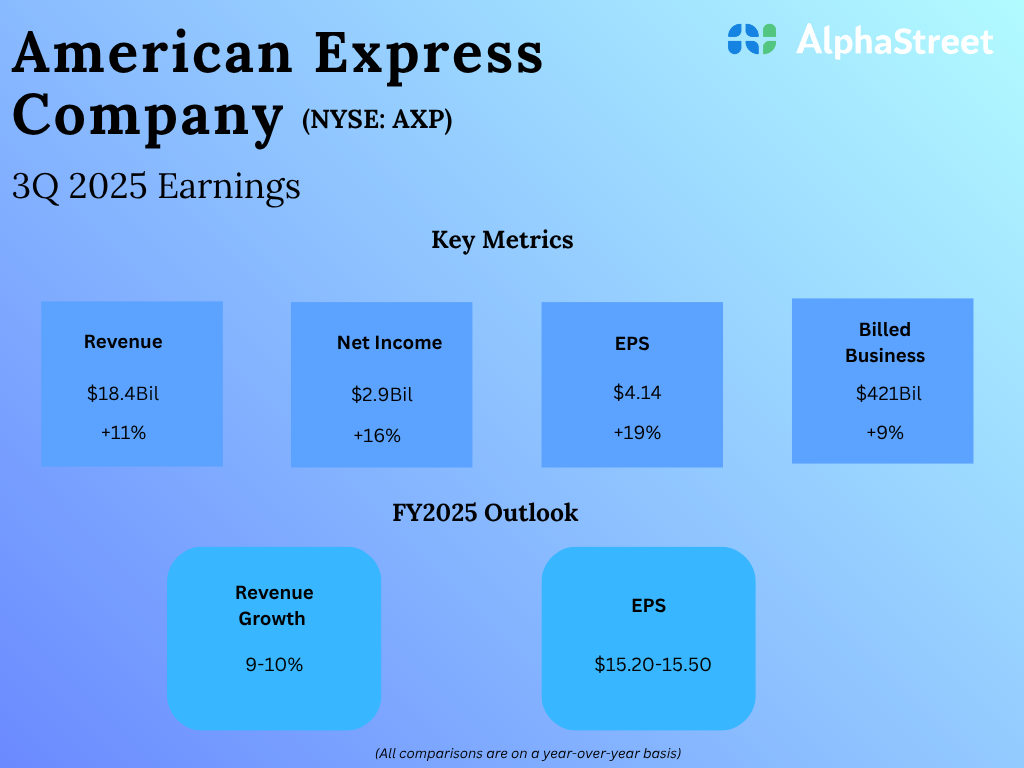

Analysts are projecting revenues of $18.93 billion for American Express in the fourth quarter of 2025, which indicates a 10% growth from the same period a year ago. In the third quarter of 2025, revenues increased 11% year-over-year to $18.4 billion.

Earnings

The consensus estimate for earnings per share in Q4 2025 is $3.53, which implies a 16% increase from the prior-year quarter. In Q3 2025, EPS increased 19% YoY to $4.14.

Points to note

American Express is expected to benefit from its solid premium customer base and strong demand and engagement for its products. It also has a strong network with 160 million merchants around the world who accept its cards. The company’s strategy of continuously refreshing its products and enhancing its value propositions to offer a range of benefits and services to customers is helping drive engagement and growth.

AXP has a strong customer base, including Millennials and Gen Z customers, with high spending levels and strong engagement. Its high spending customers on average spend nearly three times more annually on American Express cards than the average spend per card on other networks. The company’s premium customers attract world class merchant partners who add more value to membership, which in turn drives further engagement, thereby fueling continuous growth for the company.

In Q3, card member spending accelerated to 9% with strong retail spending and a rebound in travel. Credit performance remained stable with low delinquency and write-off levels. The company’s focus on premium products, which attract customers with high incomes and high credit-worthiness, has helped it reduce write-offs.

AXP continues to see robust demand for its premium products and its premium customer base gives it a strong advantage. The company’s business has remained resilient in an uncertain economic environment. Its performance in the fourth quarter is likely to have benefited from higher spending on travel and entertainment during the holiday season.