AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects Ares Management to deliver another quarter of robust growth. Analysts are modeling earnings per share of $1.33 for the first quarter of 2026, based on a consensus of 13 analysts with estimates ranging from $1.19 to $1.40. The revenue consensus stands at $1.11B, with the estimate range spanning $1.09B to $1.12B. The alternative asset manager reports results on May 1st, providing investors with an early read on the health of private markets activity as we move deeper into the year.

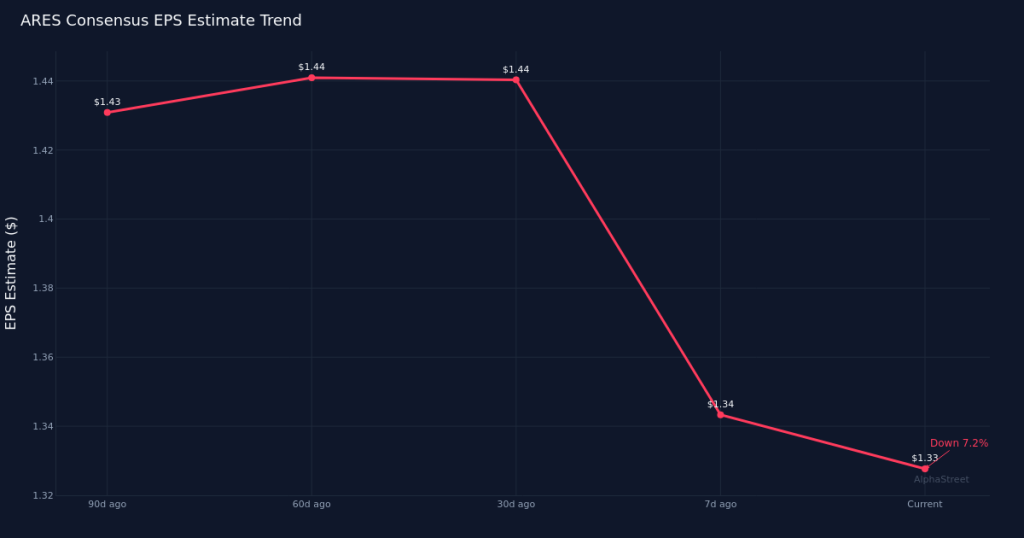

Analyst sentiment has cooled heading into the print. The EPS consensus has drifted down 7.6% over the past 30 days from $1.44, and down 7.0% over the past 90 days from $1.43. This recent downward revision pattern suggests analysts have grown more cautious, potentially reflecting concerns about the pace of deployment activity, fee-generating assets under management growth, or realized performance fees. When estimates move in a consistent direction, it often signals shifting visibility into near-term business drivers, and the downward trajectory here warrants attention from investors assessing the strength of the private capital markets environment.

The year-over-year comparison points to significant growth. Consensus implies EPS growth of 22.0% compared to year-ago earnings of $1.09 in the first quarter of 2025. On the revenue line, analysts are modeling growth of 25.5% versus the $884.6M reported in the prior-year period. For context, the year-ago quarter generated net income of $245.5M, translating to a net margin of 27.8%. If Ares delivers to consensus, the implied revenue expansion of more than a quarter year-over-year would represent a continuation of the firm’s growth trajectory, driven by its diversified platform across credit, private equity, real estate, and infrastructure strategies. The profitability baseline from a year ago provides a reference point for assessing whether margin expansion or contraction accompanies the anticipated top-line growth.

The stock sits at $119.70 heading into the report. Investor positioning and recent price action will influence how the market responds to results, particularly given the downward estimate revisions over the past three months. Where the shares trade relative to recent highs and lows often shapes the risk-reward setup, as does the sentiment backdrop around alternative asset managers more broadly. Fee-related earnings, fundraising momentum, and deployment rates across strategies will be critical inputs for investors recalibrating their views on the shares.

The asset management business model makes certain metrics particularly telling. Beyond the headline EPS and revenue figures, investors should focus on assets under management trends, both gross and net inflows, and the composition of fee-generating AUM versus dry powder. Management fee growth provides the stable revenue foundation, while realized and unrealized performance fees introduce variability. The split between fee-related earnings and performance-driven income matters for valuation, as the market typically assigns a higher multiple to predictable management fees. Commentary on fundraising pipelines, particularly for flagship funds across credit and private equity, will signal the firm’s ability to sustain growth momentum through 2026 and beyond.

Deployment activity and portfolio performance deserve close scrutiny. The pace at which Ares is putting capital to work influences both near-term performance fees and the velocity at which it can return to the fundraising market. Equally important is how existing portfolio companies and credit investments are performing in the current macro environment, as this drives both realized gains and the marks that will eventually translate into incentive fees. Any color on exit activity, refinancing trends in the credit portfolios, or stress in specific sectors would move the stock, particularly given the recent estimate cuts.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.