AlphaStreet Newsdesk powered by AlphaStreet Intelligence

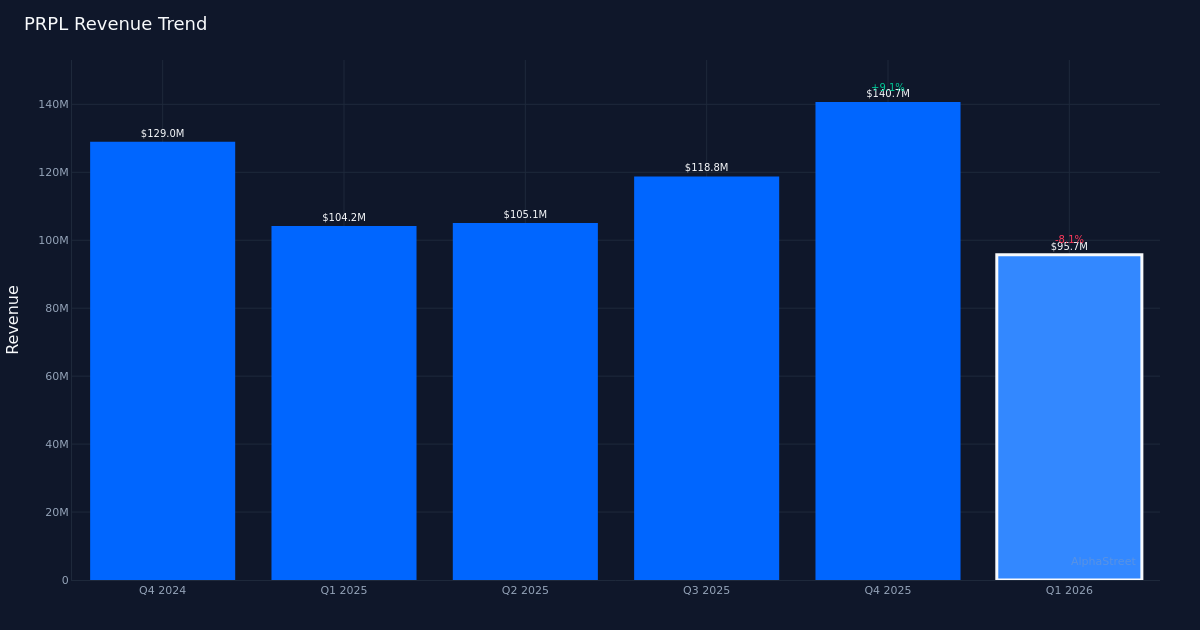

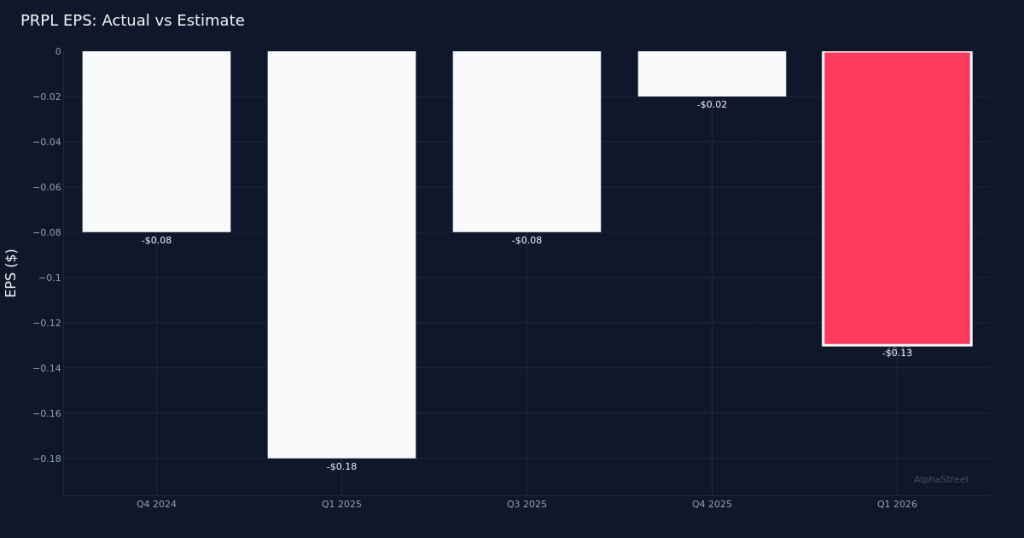

PRPL|EPS -$0.13 vs -$0.13 est (+0.0%)|Rev $95.7M|Net Loss $30.6M

PRPL|EPS -$0.13 vs -$0.13 est (+0.0%)|Rev $95.7M|Net Loss $30.6MIn-Line Results. Purple Innovation, Inc. (NASDAQ:PRPL) reported Q1 2026 results that met analyst expectations on the bottom line, posting an adjusted loss of $0.13 per share in line with consensus estimates. Revenue totaled $95.7M for the quarter, down 8.1% from $104.2M in the prior-year period. The company recorded a net loss of $30.6M as the specialty mattress and comfort products maker continues to navigate a challenging demand environment for home furnishings. Shares fell 19.6% to $0.51 following the release, suggesting investors remain concerned about the trajectory of the business despite the matched loss figure.

Top-Line Pressures. The 8.1% year-over-year revenue decline underscores persistent headwinds facing Purple as consumer spending on big-ticket home items remains subdued. The furnishings sector has been particularly vulnerable to higher interest rates and weakened housing turnover, factors that typically drive mattress replacement cycles. With the company meeting loss expectations rather than beating them through operational improvements, the quality of this in-line print appears limited. The revenue contraction suggests Purple is still struggling to drive unit volume and maintain pricing power in an increasingly promotional competitive landscape.

Showroom Strength. A bright spot emerged in the company’s retail operations, where showroom comps increased 7.0% for the quarter. This positive comparable metric indicates that Purple’s physical retail presence continues to resonate with consumers who visit its locations, likely benefiting from the experiential nature of mattress shopping where customers can test the company’s proprietary comfort technology. The divergence between strong showroom performance and overall revenue decline suggests challenges may be concentrated in other channels, potentially including e-commerce or wholesale partnerships.

Full-Year Outlook. Management provided full-year revenue guidance of $465.0M to $485.0M, offering investors visibility into expected performance for the balance of 2026. At the midpoint of $475.0M, this outlook implies sequential improvement from the Q1 run rate will be necessary to achieve targets. The guidance range will be critical for investors assessing whether Purple can stabilize its business and return to growth, or if further market share losses lie ahead in the competitive sleep products category.

Analyst Sentiment. Wall Street maintains a generally constructive view with analyst consensus standing at 5 buy ratings and 4 hold ratings, with no sell recommendations. This positioning suggests the investment community sees potential value in the beaten-down shares, though the hold contingent reflects caution about near-term execution risks. The company operated with $25M in cash and cash equivalents at quarter end, a figure that warrants monitoring given the ongoing losses.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.