AlphaStreet Newsdesk powered by AlphaStreet Intelligence

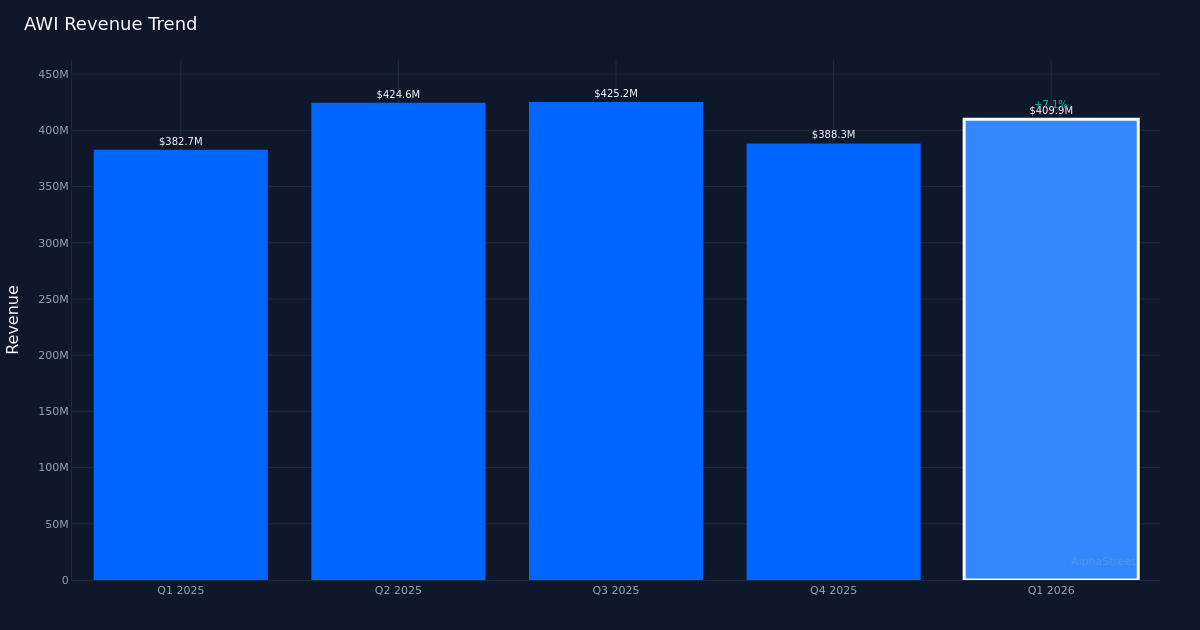

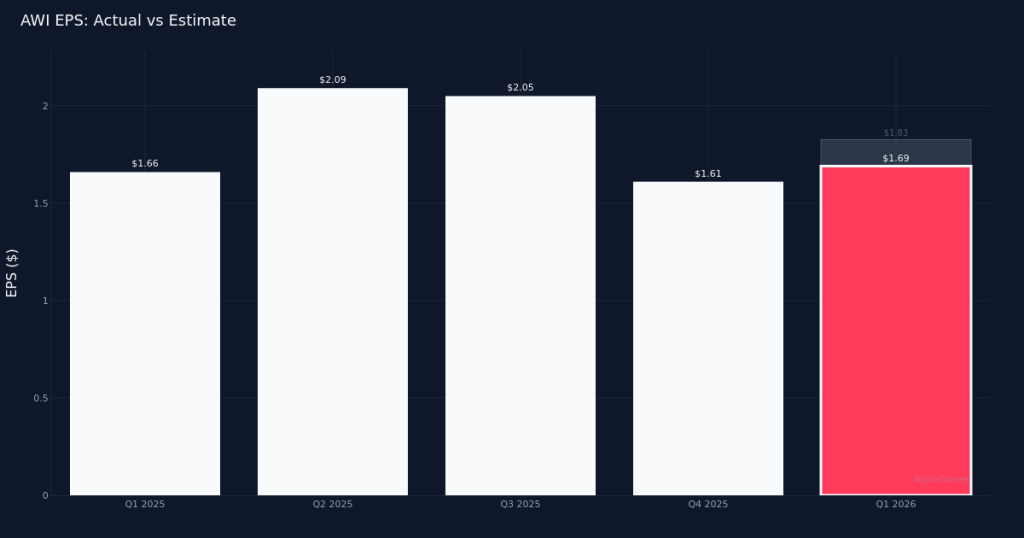

Earnings miss. Armstrong World Industries, Inc. (NYSE:AWI) reported Q1 2026 adjusted diluted earnings per share of $1.69, missing Wall Street’s $1.83 estimate by 7.7%. The building products manufacturer generated $409.9M in revenue for the quarter, up 7.1% from $382.7M in the prior-year period, reflecting continued demand for ceiling solutions despite the bottom-line shortfall. Adjusted net income came in at $73.0M as the company navigated persistent input cost pressures and operational investments.

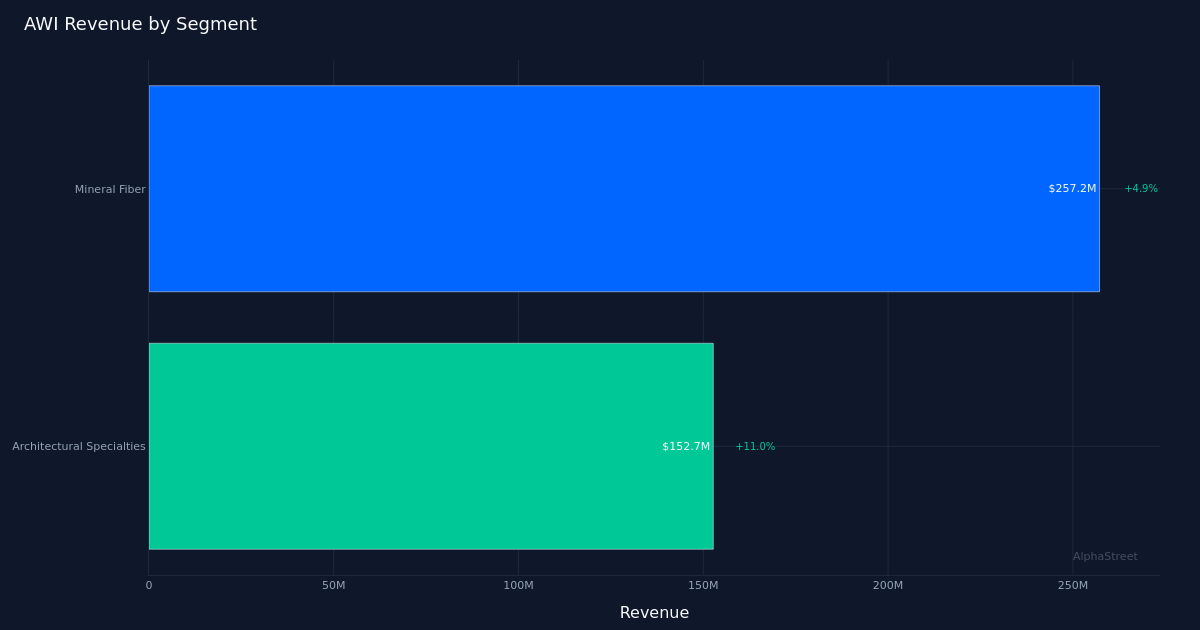

Revenue-driven growth. The top-line expansion signals genuine strength in Armstrong’s core markets, with the 7.1% year-over-year revenue increase suggesting healthy underlying demand rather than financial engineering through cost reductions. The Mineral Fiber segment led performance with $257.2M in revenue, up 4.9% year-over-year, demonstrating the resilience of the company’s flagship ceiling tile and grid products across commercial construction and renovation projects. The revenue beat relative to organic demand patterns indicates market share gains in key product categories, though margin compression remains evident given the EPS underperformance relative to revenue growth.

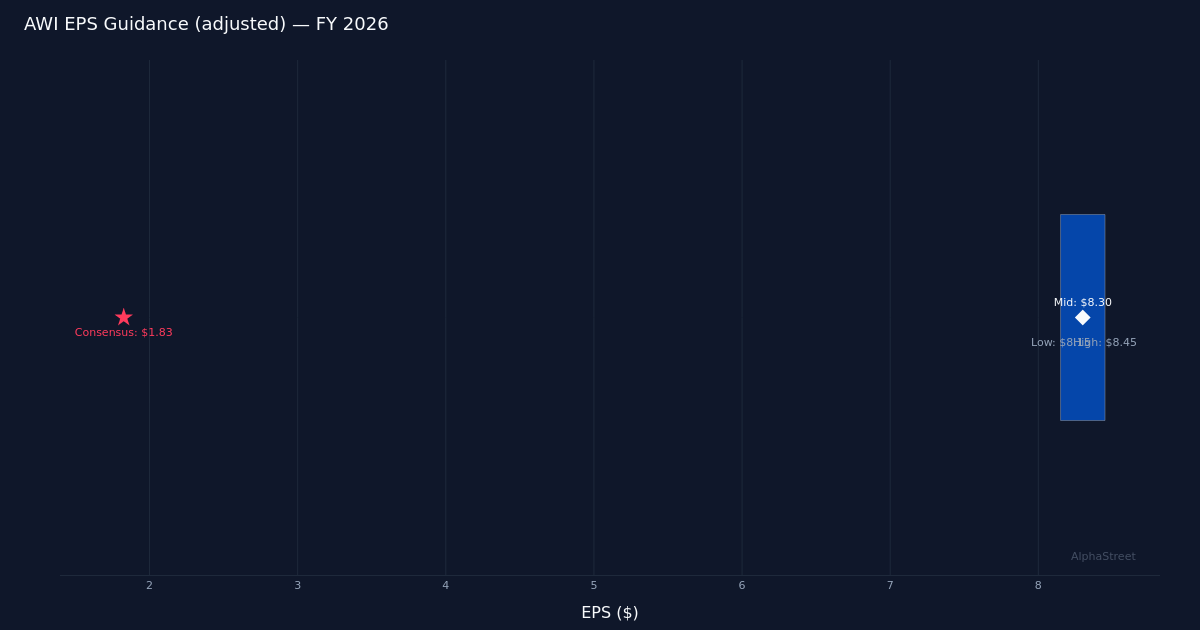

Guidance provides clarity. Management projected full-year 2026 adjusted EPS in the $8.15 to $8.45 range, establishing a framework for investors to assess the trajectory beyond the first-quarter stumble. The company expects FY 2026 revenue of $1.74B to $1.78B, implying sequential acceleration from the Q1 run rate and suggesting confidence in project pipelines and pricing initiatives taking hold in subsequent quarters. The guidance midpoint reflects management’s expectation that operational leverage will improve as manufacturing efficiencies materialize and pricing actions offset raw material headwinds that likely contributed to the Q1 margin compression.

Market reaction. Shares fell 6% following the report. With 43.2M diluted shares outstanding, the company maintains a focused equity base that has historically supported premium valuation multiples relative to broader building products peers. Wall Street consensus stands at 7 buy ratings and 6 hold ratings with no sell recommendations, indicating analysts maintain constructive views on the company’s market positioning and execution capability despite the near-term earnings disappointment.

Execution imperative. The juxtaposition of solid revenue growth against weaker profitability points to operational challenges that management must address through the balance of 2026. Armstrong’s ability to translate market demand into margin expansion will determine whether the stock can work higher from current levels, particularly as commercial construction activity remains sensitive to interest rate conditions and broader economic uncertainty.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.