Bank of Marin Bancorp (Nasdaq: BMRC) reported higher net interest margins and continued loan and deposit growth in the fourth quarter of 2025, as the lender detailed its balance sheet and operating performance alongside its quarterly earnings disclosure.

Balance Sheet Trends

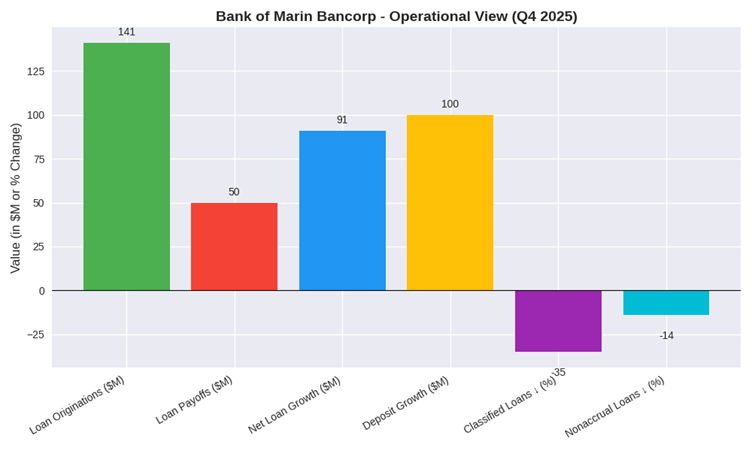

On December 31, 2025:

- Total loans: $2.121 billion, up $30.5 million quarter-over-quarter

- Total deposits: Increased by $33.0 million

- Non-interest-bearing deposits: 43.7% of total deposits

New loan fundings, excluding PPP loans, totaled $106.5 million during the quarter.

Revenue Generation and Margins

The company reported a tax-equivalent net interest margin of 3.32%, up from 3.08% in the third quarter.

Margin expansion reflected higher loan yields, increased securities income, and lower deposit costs, partly offset by interest expense on subordinated notes.

Capital and Funding Structure

During the fourth quarter, Bank of Marin Bancorp completed its balance sheet repositioning program, which included:

- Reclassification and sale of securities

- Issuance of $45.0 million in subordinated debt

At quarter end, total risk-based capital ratios were 15.25% for Bancorp and 13.90% for the bank subsidiary.

Asset Quality Review

Credit quality indicators at December 31, 2025, showed:

- Allowance for credit losses: 1.42% of loans

- Classified loans: 1.51%

- Non-accrual loans: 1.27%

- Net charge-offs: $64,000

- Loan loss provision: $300,000

Both classified and non-accrual loan ratios declined from the previous quarter.

Shareholder Returns

The board declared a quarterly dividend of $0.25 per share, payable February 12, 2026, marking the 83rd consecutive quarterly dividend.

Performance Summary

Bank of Marin Bancorp reported quarter-over-quarter growth in loans and deposits and an improvement in net interest margin. Credit metrics improved, and capital ratios remained above regulatory requirements. Shares declined on the day of disclosure as investors evaluated operating performance.