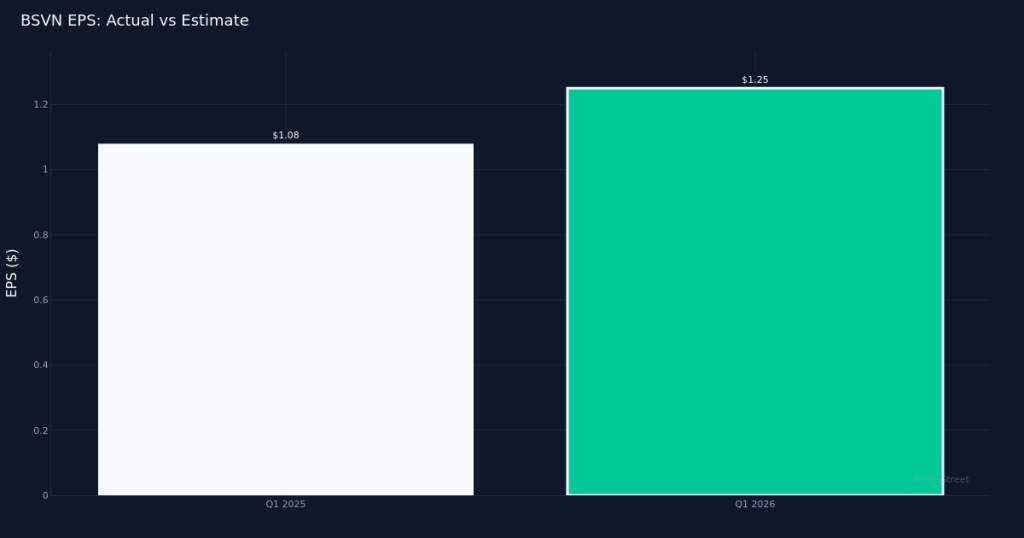

Strong Beat. Bank7 Corp. (NASDAQ:BSVN) delivered Q1 2026 diluted earnings of $1.25 per share, surpassing analysts’ $1.04 forecast by 20.2%. Revenue totaled $33.8M for the quarter, representing a 11.0% increase from the $30.4M recorded in Q1 2025. Net income reached $12.0M for the quarter, while EPS was up 15.7% from $1.08 in Q1 2025. The regional bank’s shares traded jumped 4.8% following the report.

Quality Fundamentals. The beat appears driven by genuine revenue growth rather than mere expense management, with the double-digit revenue expansion providing a solid foundation for the earnings outperformance. The company’s total loans reached $1.59B for the quarter, while total assets stood at 1.95B at quarter end, reflecting the balance sheet scale supporting the Oklahoma City-based lender’s operations. The year-over-year EPS growth of 15.7% outpacing the 11.0% revenue increase suggests improving operational leverage, a positive indicator of the bank’s ability to generate incremental profitability as it scales.

Management Perspective. Leadership struck a confident tone on the results, with management noting, “And so, I suppose it’s a little boring for some people quarter after quarter where we’re always putting up these fantastic results.” The comment underscores the consistency of Bank7’s execution. Management also acknowledged the shifting macro backdrop, observing, “And so last quarter, I think the markets were expecting rate cuts in this quarter,” highlighting how expectations around Federal Reserve policy continue to influence the operating environment for regional banks dependent on net interest margin dynamics.

Analyst Sentiment. Wall Street maintains a constructive view on Bank7, with consensus standing at 5 buy, 2 hold, and 0 sell ratings. The lack of any sell recommendations reflects confidence in the bank’s business model and execution track record, even as regional banks navigate ongoing concerns about commercial real estate exposure and deposit competition. The 20.2% earnings beat relative to the $1.04 consensus estimate suggests analysts may have been conservative in their modeling, potentially leaving room for upward estimate revisions in coming quarters.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.