Shares of Beyond Meat Inc. (NASDAQ: BYND) seem to have recovered, gaining over 5% on Monday. The stock has dropped 28% year to date and 68% over the past 12 months. The company delivered disappointing earnings results for the fourth quarter of 2021 last week which sent shares tumbling at the time.

There is a mixed sentiment around the stock with some experts expressing optimism for the long term while others opting for caution. Despite all this, the company remains optimistic about the coming year. Here are a few points to consider:

Lacklustre performance

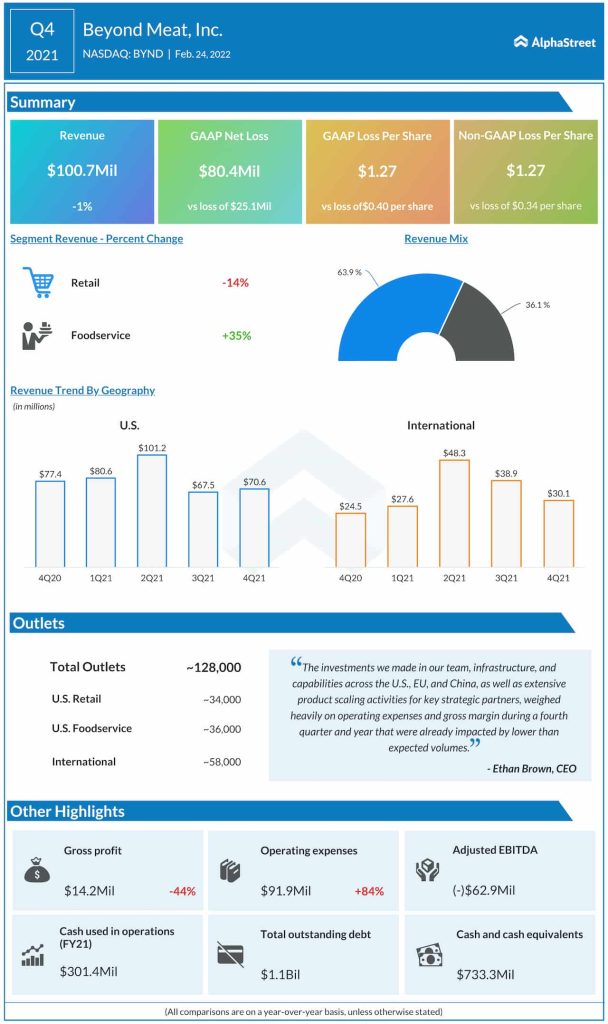

Revenues fell 1.2% year-over-year to $100.7 million during the fourth quarter of 2021, missing market estimates. This decline was mainly due to a drop of nearly 20% in US retail revenues due to reduced demand, five fewer shipping days, higher trade discounts and loss of market share. Increases in US foodservice and international revenues were not sufficient to offset the drop in retail revenues.

The company reported a wider-than-expected loss of $1.27 per share for the quarter. Gross margins declined to 14.1% due to product mix impacts, higher trade discounts, and increases in manufacturing costs. Investments in product scaling activities and other capabilities weighed heavily on operating expenses and gross margins.

On its quarterly conference call, Beyond Meat stated that according to SPINS data showing trends in consumer takeaway in US retail, during the fourth quarter, sales of Beyond Meat products were down 2.7% YoY compared to an increase of 0.4% for the category.

Why the optimism?

First off, since 2018, Beyond Meat has grown its business 428%, or at a three-year CAGR of 74%. Although the growth rate slowed down to 14% in 2021 from 37% in 2020, the company believes this deceleration is temporary and that growth will pick up in the years to come. There are a few reasons for this optimism.

Firstly, Beyond Meat does not expect certain pandemic-related consumer trends, such as a preference for comfort foods than healthy options and the inability to try out new food products, to continue going forward. The company expects to resume in-store sampling programs for retail items in the first half of this year. This, coupled with the company’s investments in product innovation and scaling, are expected to drive growth.

During the quarter, foodservice revenues in the US grew nearly 35% while international foodservice revenues rose 36%. Beyond Meat expects to build on this momentum in 2022. Lastly, the company has invested significantly in its priority markets – the EU and China. These investments have paved the way to meaningful retail and foodservice opportunities for both existing and planned products in these markets. In Q4, the international business posted revenue growth of 22.6% and this momentum is expected to continue in 2022.

Beyond Meat expects net revenue to grow 21-33% YoY to $560-620 million in fiscal year 2022. The company expects flat to modest net revenue growth in the first quarter, picking up through the year, helped by factors such as distribution expansion, new product launches, and acceleration in international markets.

All in all, while some analysts believe Beyond Meat is likely to see its growth gain significant traction over the long term, there are others who think the opposite is true and thereby prefer to take a cautious approach to this stock.