Shares of Beyond Meat, Inc. (NASDAQ: BYND) were up over 1% on Monday. The stock has dropped 13% year-to-date and 61% over the past 12 months. The company had a challenging first quarter in 2023 as revenues continued to decline but on the other hand, it managed to narrow its losses compared to the year-ago period. Here’s a look at what the company has planned for the remainder of the year:

Revenue

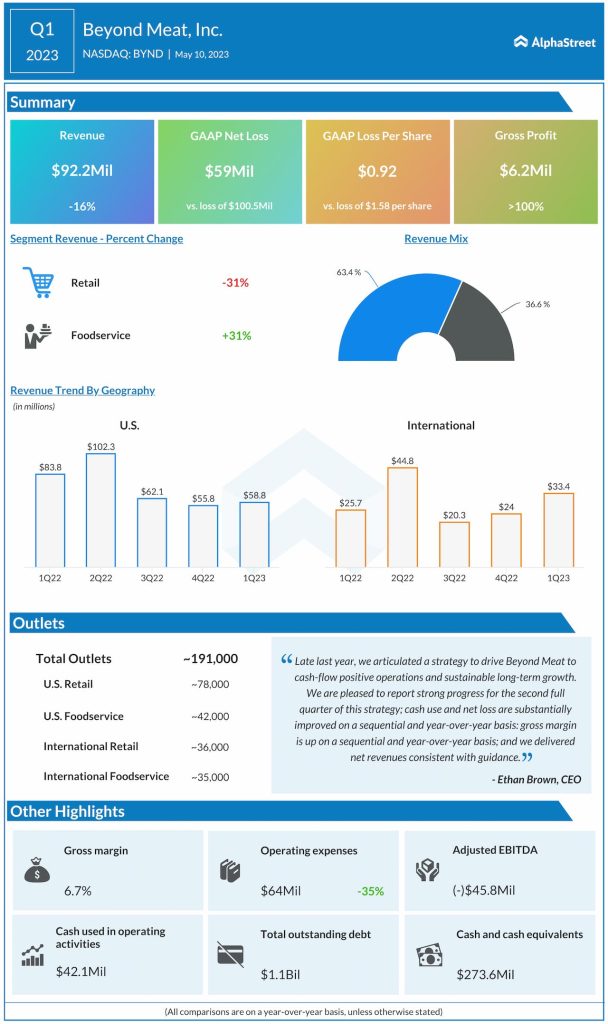

Beyond Meat’s revenues declined 16% year-over-year to $92.2 million in Q1 2023. However, it increased 15% on a sequential basis compared to the fourth quarter of 2022. The top line results were impacted by demand weakness and broader macroeconomic challenges.

Inflationary pressures forced customers to shift to lower-priced animal protein, which in turn put pressure on the US plant-based meat category. In Q1, the company saw net revenue per pound fall around 9.1% and volume of products sold decline 7.3% YoY.

For the full year of 2023, Beyond Meat expects revenues to decrease 1-10% YoY to a range of $375-415 million. In the second quarter of 2023, revenues are expected to increase 15% sequentially from Q1. The company anticipates a pickup in revenue growth during the back half of 2023, led by distribution expansion of products that were recently launched in the US like Beyond Steak and Beyond Chicken Nuggets, as well as contributions from new products in international markets.

Profitability

In Q1, Beyond Meat managed to narrow its net loss to $59 million, or $0.92 per share, compared to $100.5 million, or $1.58 per share, last year. Gross profit and gross margin improved to $6.2 million and 6.7% from $0.2 million and 0.2% from last year. The improvement in gross margin was driven mainly by lower manufacturing and logistics costs. In addition, during the quarter, the company managed to lower its operating expenses by 35% from last year.

For the full year, Beyond Meat expects gross margin to be 1-2 percentage points above its prior guidance of low double digits and it expects it to increase sequentially through the remainder of the year. Operating expenses are expected to be around $250 million for the year.

Prioritization of near-term growth opportunities

Beyond Meat is currently focusing more on the near-term restoration of growth. In US retail grocery, along with marketing and promotional campaigns, the company is working on strategic pricing actions in order to narrow the gap with animal protein. It is also working on revamping its product portfolio within the refrigerated category. The frozen category continues to be a growth area with increases in dollars and units both on a sequential and year-over-year basis in Q1.

In EU retail, Beyond Meat is expanding its product portfolio with new launches such as Beyond Chicken Burger, Beyond Schnitzel, and Beyond Nuggets. These products will complement the existing Beyond Meat portfolio in Europe.