Booz Allen Hamilton Holding Corporation (BAH/NYSE), a U.S. management and technology consulting firm serving government and national security clients, shares were trading near $95.76, up modestly in early session. The stock has traded in a 52-week range of $79 to $138 and carries a market capitalization of approximately $11.6 billion.

Share Impact

BAH shares rose slightly following the release of third quarter fiscal 2026 results, reflecting investor focus on stronger-than-expected earnings despite a decline in revenue and slower new bookings.

Q3 Financial Results

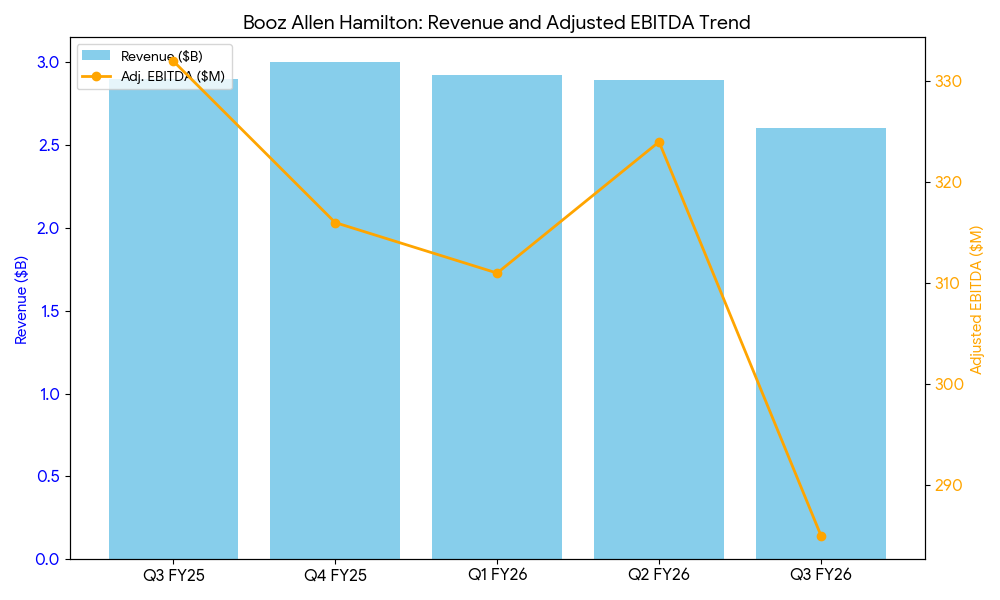

- Revenue: $2.62 billion, down 10.2% year-over-year, reflecting slower federal procurement, delayed contract execution, and reduced civilian agency spending.

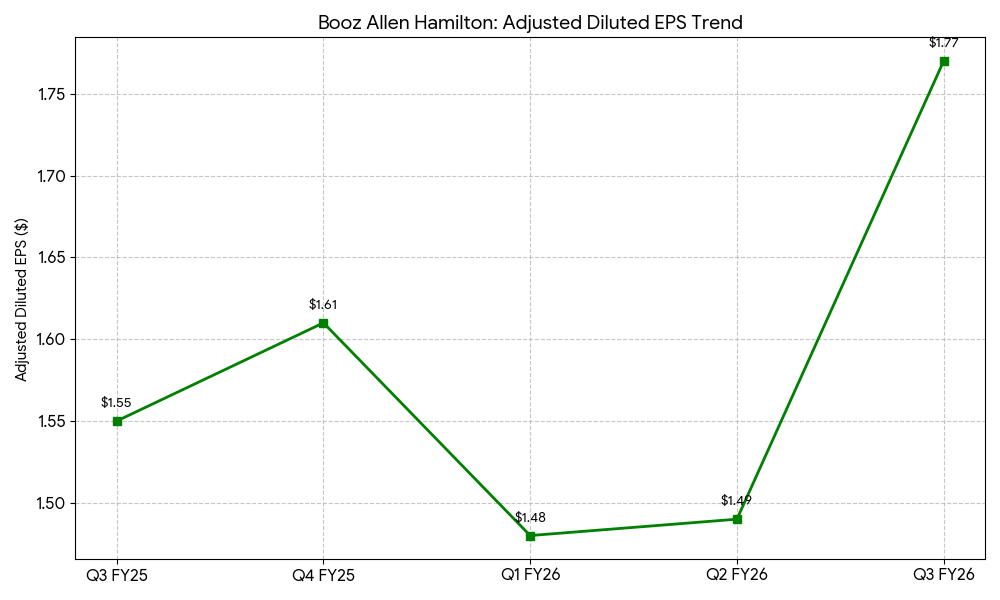

- Adjusted EPS: $1.77, above consensus expectations, aided by cost discipline and favorable tax items.

- Adjusted EBITDA: $285 million, yielding a margin of about 10.9%, broadly stable despite revenue decline.

- Operating Income: Declined year-over-year, consistent with lower top-line performance.

- Net Income: Approximately $200 million for the quarter.

- Free Cash Flow: $248 million, up more than 80% from prior year due to disciplined working capital management.

Backlog and Billings

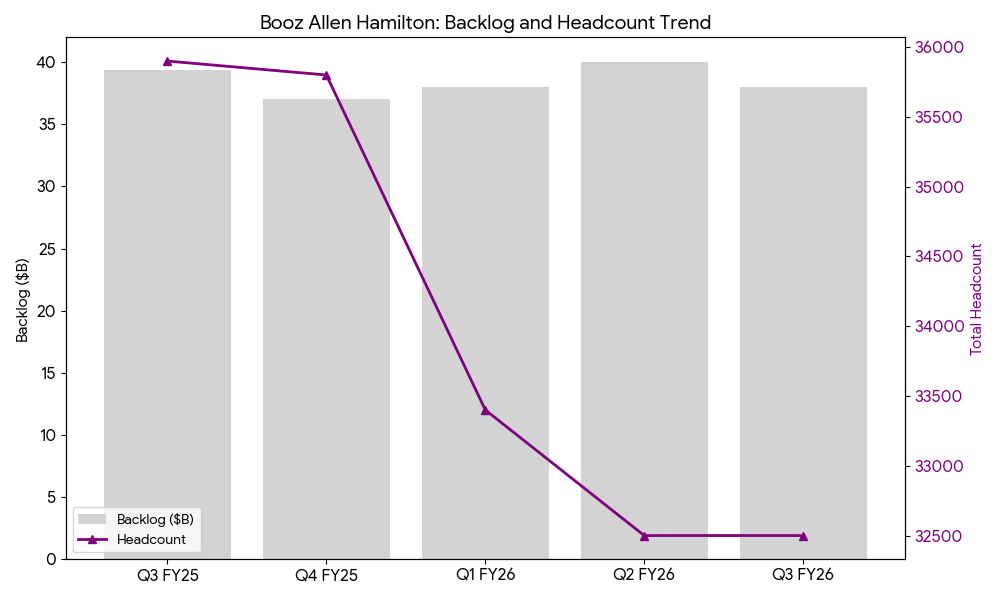

- Total Backlog: ~$38 billion, largely stable year-over-year, providing multi-year revenue visibility.

- Book-to-Bill Ratio: ~0.3x, indicating slower new bookings during the quarter.

- Headcount: Approximately 31,000 employees, relatively flat sequentially, reflecting the company’s focus on efficiency and cost management amid slower new contract awards.

Year-Over-Year and Full-Year Context

Quarterly revenue declined from Q3 fiscal 2025 levels of ~$2.92 billion. Backlog remained solid, though slower bookings signal potential top-line pressure in upcoming quarters. Headcount stability suggests tight control over labor costs and productivity during a period of weaker revenue growth.

Full-Year Guidance:

- Revenue: $11.3 billion – $11.4 billion, below prior expectations.

- Adjusted EPS: $5.95 – $6.15, reflecting anticipated margin resilience and lower share count.

Analyst Activity

No major analyst upgrades or downgrades were reported with the results. Consensus ratings remain cautious, with revenue and EPS forecasts trimmed amid ongoing federal procurement uncertainty.

Sector and Macro Pressures

Booz Allen operates in a sector sensitive to U.S. federal spending cycles. Delayed budget approvals, slower contract awards, and tighter civilian agency budgets have pressured revenue and billings. Defense and intelligence spending remains relatively resilient, supporting backlog execution and strategic staffing stability.

Competitive Landscape

Booz Allen competes with CACI International, Leidos, and SAIC across cybersecurity, mission support, analytics, and technology modernization. Competitors face similar exposure to federal funding uncertainty, with relative performance tied to contract mix, segment exposure, and ability to manage headcount in line with backlog trends.

Bottom Line

Q3 results showed revenue contraction and weak new bookings, partially offset by strong adjusted earnings, stable margins, solid free cash flow, and stable headcount. Backlog remained robust but slower bookings signal potential top-line challenges ahead. Full-year guidance reflects moderated growth expectations, and investor focus will remain on backlog execution, contract awards, and cost discipline amid ongoing federal budget pressures.