Shares of Box Inc. (NYSE: BOX) were up 6% on Thursday, a day after the company reported strong results for the second quarter of 2021. The stock has gained 22% since the beginning of this year. Like many other cloud computing companies, Box has gained from the shift to a remote work environment accelerated by the COVID-19 pandemic.

Quarterly performance

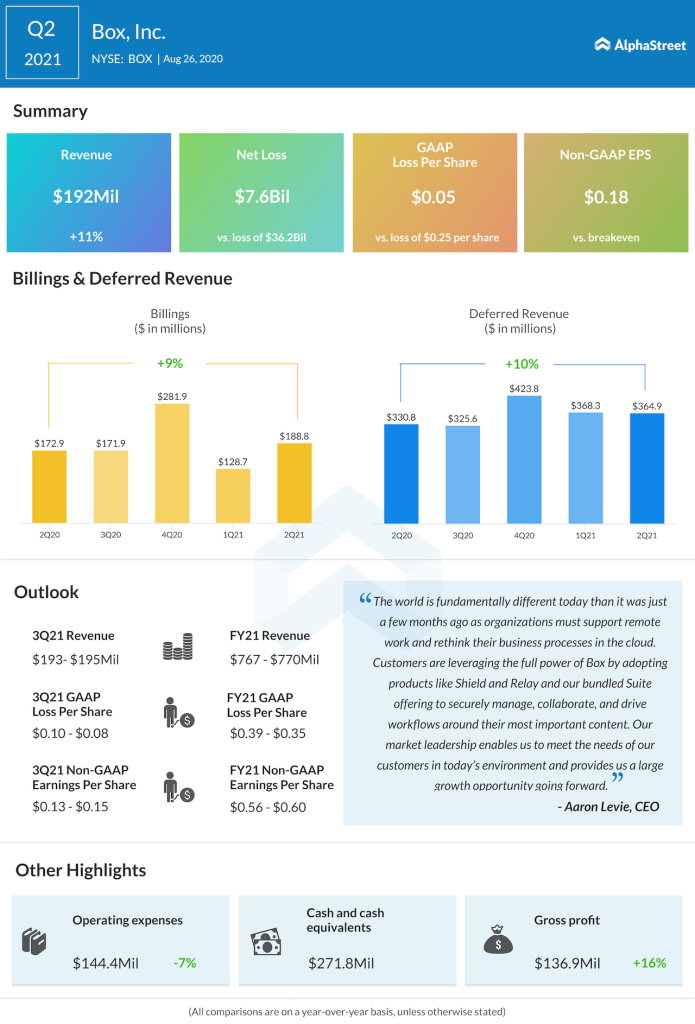

Revenue increased 11% year-over-year to $192 million while adjusted EPS rose to $0.18 from breakeven last year. 28% of revenue came from outside the US, up from 25% a year ago, with strong performance from Japan. Box saw expansion in its existing customer base and witnessed increasing demand for its products which led to higher adoption of Suite during the quarter.

At quarter-end, remaining performance obligations (RPO) were up 13% year-over-year to $726.7 million, of which approx. 65% is expected to be recognized over the next 12 months. RPO represents non-cancellable contracts that are expected to be recognized as revenue in future periods.

As the need for digital business processes increase due to remote work, Box is working on automating and digitizing content-centric processes. The ability to integrate seamlessly with applications such as Microsoft Teams, Zoom, G Suite etc. is critical to the company’s remote work strategy.

Billings

Billings increased 9% to $188.8 million during the second quarter. Billings performance is driven by factors such as payment durations and the timing of large renewals. Customer contract durations remained stable during the period.

In the second quarter, Box closed 64 deals worth more than $100,000 and three deals over $500,000. The company is seeing strong demand for six-figure enterprise deals and expects to see solid year-over-year growth in its large deal counts in the third quarter. Box ended Q2 with an annualized net retention rate of 106% versus 105% a year ago.

Box expects billings growth to lag revenue growth by a bit for the remainder of fiscal year 2021. Due to challenges caused by the COVID-19 pandemic, the company expects its professional services bookings and small business segments to remain weak this year.

Outlook

For the third quarter of 2021, Box expects revenue to grow around 10% year-over-year at the midpoint to $193-195 million. The company expects to see continued strength from enterprise customers while the professional services business is anticipated to see softness. Adjusted EPS is expected to be $0.13-0.15.

For fiscal year 2021, Box expects revenue to range between $767-770 million, representing around 10% year-over-year growth at the midpoint. Adjusted EPS is expected to be $0.56-0.60.

Click here to read the full transcript of Box Inc Q2 2021 earnings call