Shares of Campbell Soup Company (NYSE: CPB) were up on Tuesday. The stock has gained 22% over the past 12 months. Last week, the company delivered second quarter 2023 earnings results that surpassed market expectations. It also hiked its guidance for the full year. Here are three factors that work in favor of this soup maker:

Sales and earnings growth

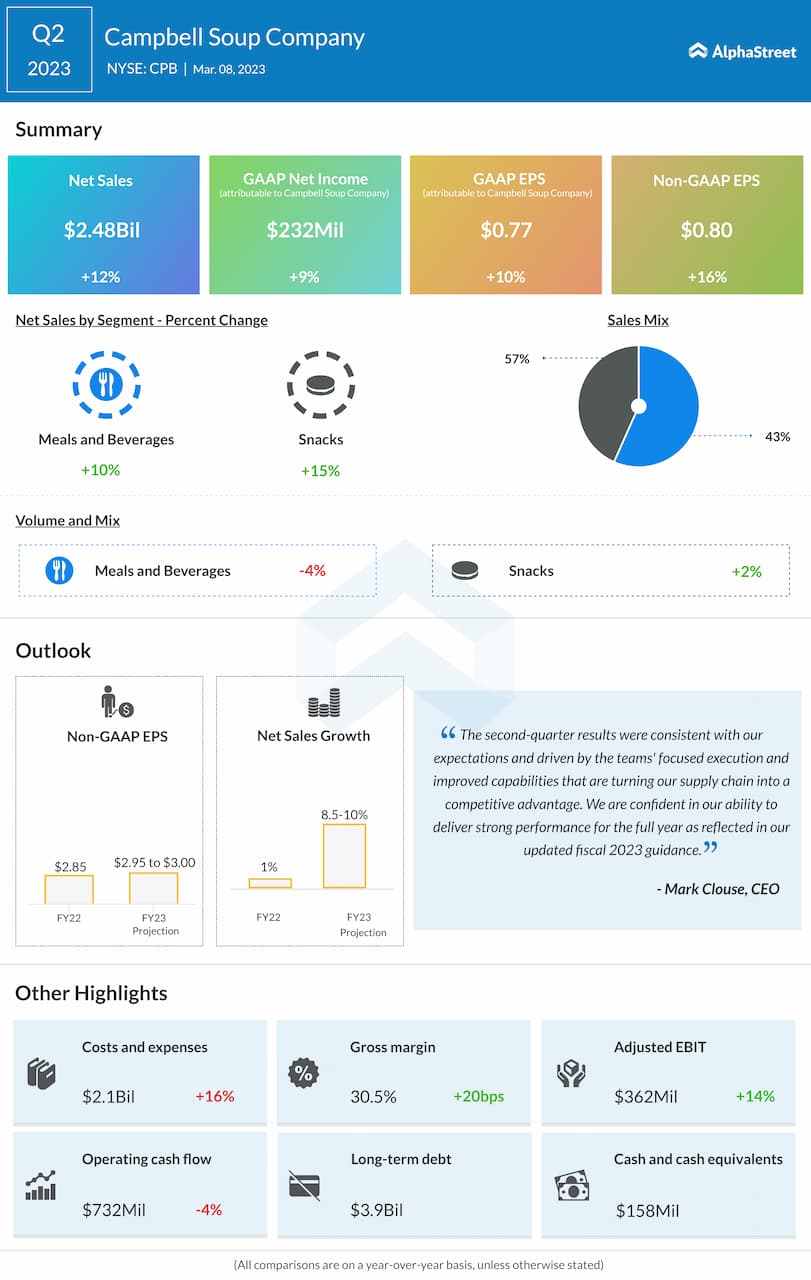

In Q2 2023, Campbell’s net sales increased 12% year-over-year to $2.5 billion. Organic sales grew 13% in the quarter, helped by inflation-driven price hikes and strong consumer demand for its brands. Reported EPS increased 10% to $0.77 while adjusted EPS rose 16% to $0.80 in Q2 compared to the year-ago quarter.

Category strength

Campbell saw double-digit sales growth in both its segments during the second quarter. Meals & Beverages recorded sales growth of 10% on a reported basis and 11% on an organic basis, helped by increases in US retail products and gains in foodservice. The Snacks segment posted sales growth of 15% on both a reported and organic basis, driven by a 20% growth in power brands sales.

Within Meals & Beverages, sales of US soup increased 7%, driven by gains in condensed and ready-to-serve soups. The US soup business grew dollar consumption by 4% in Q2. The segment also benefited from gains in Prego and Pace sauces. In Q2, Italian sauces witnessed an 8% growth in dollar consumption while in Mexican sauces, dollar consumption was up 12%.

The Snacks segment benefited from gains in cookies, crackers and salty snacks with strong performances from brands like Goldfish, Pepperidge Farm, Snack Factory and Kettle. The Goldfish brand, which continues to be a key growth driver, recorded a 21% rise in consumption in Q2.

Updated guidance

Campbell raised its guidance for the full year of 2023. The company now expects net sales growth of 8.5-10% compared to the previous range of 7-9%. The updated sales outlook reflects brand strength with price elasticities remaining favorable to historical norms as well as stronger supply chain execution. The company also updated its adjusted EPS outlook and now expects it to grow 3.5-5% versus the previous range of 2-5%. Adjusted EPS is expected to be $2.95-3.00.

Click here to read the full transcript of Campbell Soup’s Q2 2023 earnings conference call