Shares of Campbell Soup Company (NYSE: CPB) stayed green on Friday. The stock has gained 13% year-to-date. The company delivered better-than-expected sales and in-line adjusted EPS for its fourth quarter of 2022 a day ago. The processed foods maker expects to see strong demand for its products as well as high levels of inflation during the upcoming year.

Higher sales, lower profits

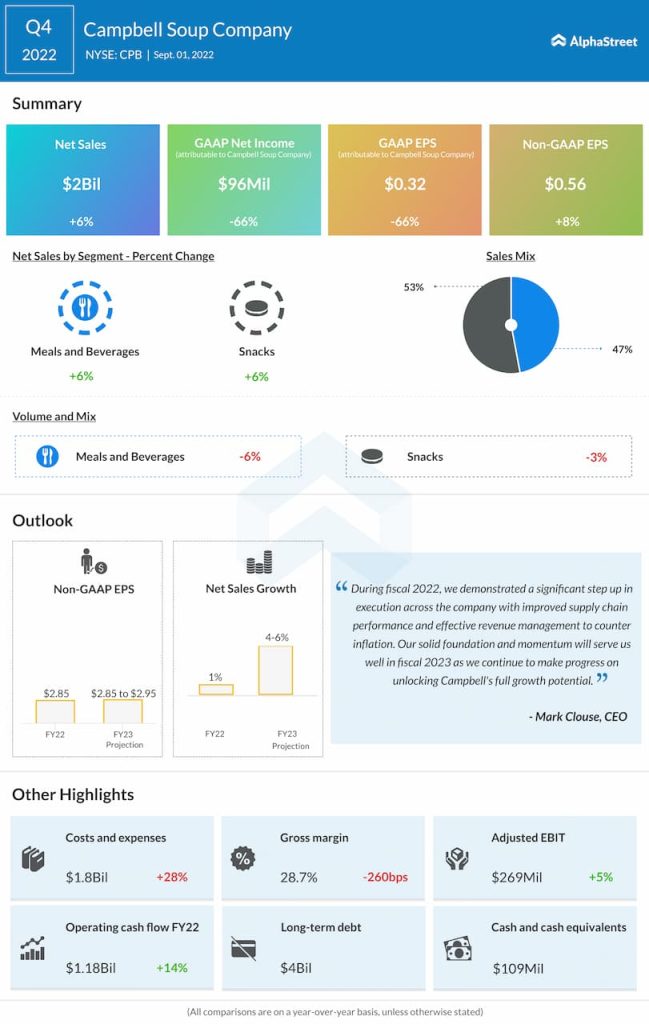

Campbell’s net sales for Q4 2022 increased 6% year-over-year to $2 billion, both on a reported and organic basis. Sales growth was driven by high consumer demand, pricing actions and improved supply. On a GAAP basis, net income fell 66% YoY to $96 million, or $0.32 per share. Gross margin dropped to 28.7% from 31.3% last year.

However, on an adjusted basis, EPS rose 8% to $0.56, and gross margin increased 40 basis points to 31.3% as pricing, supply chain productivity improvements and cost savings helped reduce the impact of inflation.

Strong portfolio and favorable trends

During the fourth quarter, Campbell recorded sales growth in both its divisions, helped by gains across its brand portfolio. Net sales increased 6% on a reported basis in both the Meals & Beverages and Snacks segments. The growth was driven by gains in soups, pasta sauces, salty snacks, cookies and crackers. In both divisions, pricing and sales allowances were offset by volume declines.

Amid inflationary pressures, people have started to cook and eat more at home to save money and there is a preference for shelf-stable, simple meals like ready-to-serve soup. Sales of US soup rose 6% in Q4, driven by strength in ready-to-serve and condensed soups.

The rise in quick scratch cooking has also led people to look for more ways to increase the flavors of their meals, which in turn fueled demand for sauces. The company’s Prego and Pace brands saw double-digit consumption growth in Q4. Through the launch of Campbell’sFlavorup concentrated sauces and the relaunch of Campbell’s cooking sauces, the company aims to drive further growth in its sauces portfolio.

Snacks remained resilient with a 9% sales increase in power brands. Campbell witnessed share gains in Kettle Brand, Cape Cod, Snack Factory pretzel crisps and Pepperidge Farm cookies.

Outlook

Looking ahead into fiscal year 2023, Campbell expects to see strong demand for its brand portfolio. The company expects to generate positive top line growth in both segments helped by brand investments and an improved supply chain. Net sales for FY2023, both reported and organic, are expected to be up 4-6% compared to FY2022.

Campbell expects inflation to be in the low-teens range for the year. The company plans to tackle inflationary pressures through productivity improvements and cost savings. FY2023 adjusted EPS is projected to be flat to up 4% compared to last year.

Click here to access the full transcripts of the latest earnings conference calls