The disruption caused by coronavirus has affected almost all sectors except business service providers like Cintas Corporation (NASDAQ: CTAS), which is busy helping clients maintain hygiene and safety during the crisis. But the workwear maker is not fully immune to the COVID-related slowdown, though the impact on its operations has not been as bad as expected.

Shares of the Ohio-based firm hit a new high at the start of the month but changed course in the following days and slipped to the pre-peak levels after it announced first-quarter results. At the current price, the stock is considered overvalued and market watchers predict a modest downside in the coming weeks. Though the recent withdrawal is a buying opportunity, CTAS might disappoint those looking for immediate gains. From a long-term perspective, the strong fundamentals and impressive past performance make it an attractive bet.

New Opportunity

Before the business world was hit by the pandemic, Cintas had benefited from the booming employment market and economic growth. Interestingly, the company managed to stay resilient to the virus crisis to a great extent supported by an uptick in the non-core areas of its business such as laundry services, personal protection, and sanitization. Going forward, that could set a new sales trend as the lingering safety concerns would likely lift the demand for the related products and services. The trend is poised to continue even after normalcy returns to the business world.

Also see: Sysco Corp Q4 2020 Earnings Call Transcript

Since its client base consists of relatively large corporates, the widespread closure of small businesses does not affect the company. Those clients are looking to scale up operations as the markets gradually open up, which would create the backdrop for the company to regain the growth momentum seen before the crisis. There has been a bigger demand for safety and sanitation products compared to the pre-COVID days, especially from sectors like healthcare.

Cautious View

With a clientele that spreads across markets, the company expects to take advantage of its extensive service network and supply chain to maintain stable operations. But it will be difficult to sustain the momentum in the long term if the macroeconomic conditions do not improve and businesses remain in the grip of the pandemic. It needs to be noted that hotels and airlines, which are among the worst affected businesses, represent a large chunk of Cintas’ client base.

“Our value proposition of getting businesses ready for the workday, by providing essential unparalleled image, safety, cleanliness and compliance, has never resonated more, than it does today. A new trend of greater focus on health, readiness and outsourcing of non-core activities is underway. We are well positioned for this new normal,” said Scott Farmer, chairman and chief executive officer of Cintas.

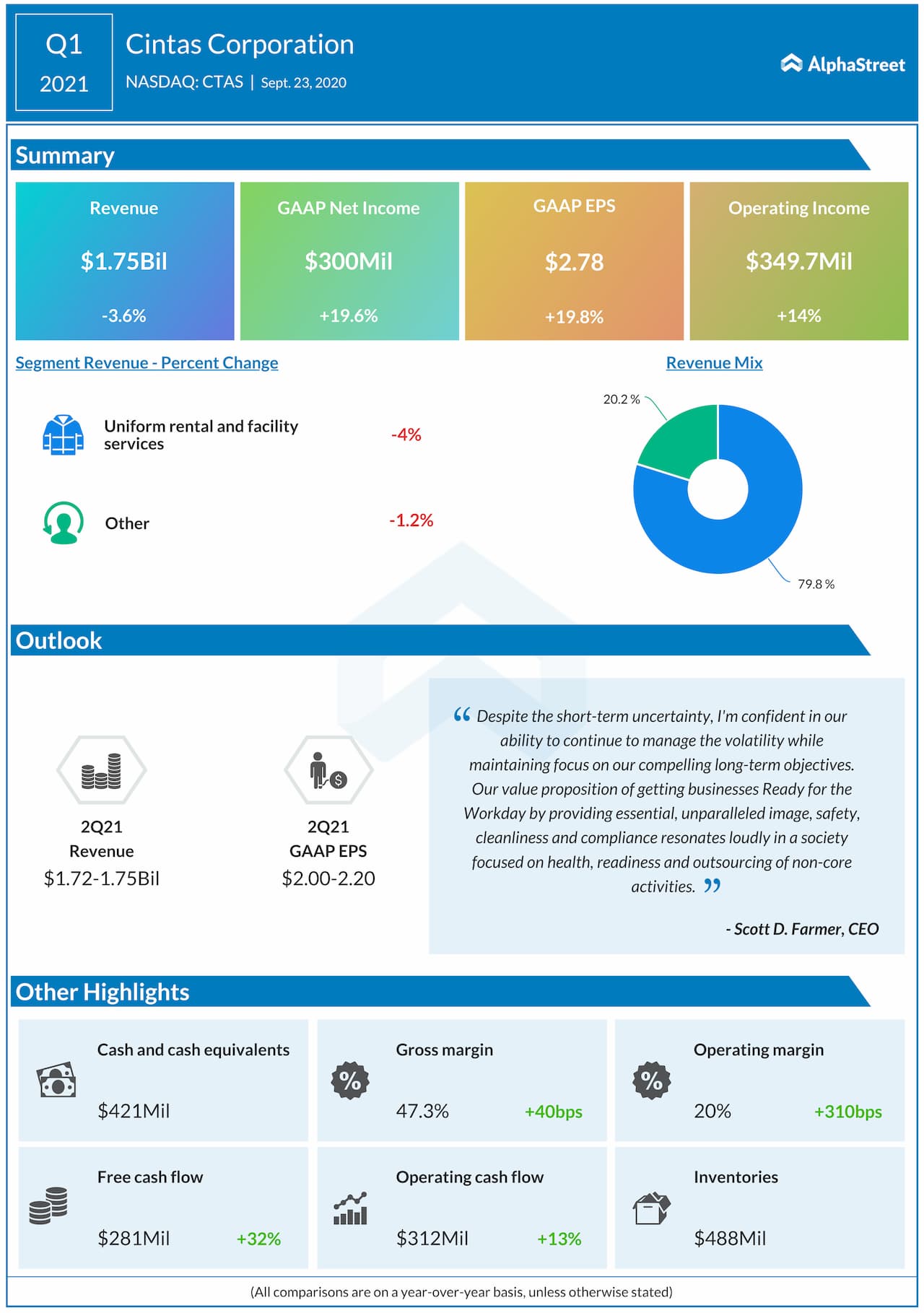

While withholding its long-term outlook, citing the continuing uncertainty, the management is optimistic about the company’s financial performance in the current quarter.

Q1 Numbers Beat

The demand for uniform rental services softened in the early months of the fiscal year as the shelter-in-place orders kept people away from their workplaces. However, its impact on Cintas’ top-line was not as severe as estimated and the recovery seen towards the end of the first quarter restricted the year-over-year decline to 4%. Earnings moved up 20% to $2.78 per share as margins benefited from a decrease in operating expenses.

Read managements/analysts’ comments on Cintas’ Q1 2021 results

Cintas’ stock consistently outperformed the S&P500 Index and the business services industry in the recent past. The stock traded slightly higher during Thursday’s session, after closing the previous session at $316.71. It has been losing momentum since hitting a record high earlier this month, and the downtrend intensified after the first-quarter earnings report.